April 9, 202611 min read

Valuation of Alternative Investments: What an IPO-Bound Founder Must Know

By Aman Singh

IPO

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

For many growth-stage Indian founders, the "Series B/C crunch" and restrictive debt covenants can stifle long-term vision. Constant fundraising cycles drain management focus, making the transition to public markets an attractive path to permanent capital and "acquisition currency."

However, moving from private boardrooms to public scrutiny requires a level of discipline often underestimated until the DRHP stage.

This guide dismantles the complexities of IPO funding, from SEBI eligibility and valuation to the nuances of Fresh Issues vs. OFS, helping you determine if your company is truly ready to ring the bell.

In the context of corporate finance, IPO funding refers to the process by which a private company raises capital from the general public and institutional investors by listing on a stock exchange (BSE or NSE).

Unlike debt, this capital is interest-free and does not require repayment, but it involves trading equity for cash. It is the definitive shift from a "private limited" structure to a "public limited" entity, subjecting the firm to market-driven valuation and SEBI's rigorous disclosure norms.

Note: While "IPO funding" can sometimes refer to investors borrowing money to bid for shares, this guide focuses exclusively on the company's perspective of raising funds.

Understanding the definition is simple, but the mechanics of how this capital actually moves from public pockets to your balance sheet involves a highly regulated workflow.

Also Read: How To Raise Funds For Your Startup In India

The flow of IPO funding in India is a structured transfer of risk and ownership, overseen by SEBI to ensure investor protection. It is not an overnight transaction but a 4–9 month systematic process.

This is how it works:

Once you understand the mechanism, the strategic question becomes: why choose this route over private equity or debt?

Navigating this complex process requires a partner, not just a checklist. For a data-driven assessment of your specific IPO timeline and readiness, talk to an S45 banker today to bring clarity and precision to your path to listing.

Also Read: Different Types Of Startup Funding In India

Going public is a strategic pivot that solves specific problems related to scale, liquidity, and perception. Below are some reasons:

Private capital often comes with short investment horizons. IPO funding provides "patient capital" suitable for long-term projects like setting up new manufacturing units, entering international markets, or funding heavy R&D cycles that don't yield immediate returns.

High leverage ratios can cripple a company's valuation. Proceeds from a Fresh Issue are frequently used to retire expensive debt, immediately boosting the bottom line by eliminating interest costs and improving the debt-to-equity ratio.

Early backers (Angels, VCs, PE firms) eventually need liquidity. An IPO allows them to sell their stake (via OFS) on a liquid market without forcing the company to buy them out, ensuring the founder doesn't lose cash reserves to facilitate an investor's exit.

A listed stock with a market-determined price is a powerful currency. Public companies can acquire competitors by swapping shares rather than spending cash, a strategy that is difficult to value and execute in the private market.

While the reasons are compelling, the method you choose to structure this funding dictates who gets the money, the company or the shareholders.

Also Read: 7 Top Venture Capital Firms in India in 2025

There are two distinct components to an IPO issue size. Understanding the difference is vital for founders to align their capital goals with investor expectations.

Type | Mechanism | Who Gets the Money? | Impact on Equity |

Fresh Issue | The company creates and sells new shares. | The Company. Funds go to the balance sheet for growth/debt repayment. | Dilutive. Total number of shares increases; promoter % decreases. |

Offer for Sale (OFS) | Existing shareholders sell their shares. | The Selling Shareholder. Funds go to VCs, PEs, or Promoters. | Non-Dilutive. Total share count remains the same; only ownership hands change. |

Type | Mechanism | Usage |

Book Building Issue | A price band is set (e.g., ₹100–₹105). Investors bid at different prices. | Standard for Main Board IPOs to discover true market demand. |

Fixed Price Issue | A single fixed price is set (e.g., ₹102). Investors bid only at this price. | Common in smaller SME IPOs, where demand discovery is simpler. |

Structuring the deal is irrelevant, however, if the company does not meet the baseline criteria to enter the market.

Before engaging with investment bankers, an honest internal assessment is crucial. SEBI and the exchanges have clear eligibility norms, but true "readiness" extends beyond checkboxes to market preparedness.

Once you have confirmed that your company meets the baseline regulatory hurdles, the focus shifts from eligibility to execution.

Also Read: Private Equity vs. Venture Capital: Key Differences

The journey from the first board meeting to the listing bell typically spans 6 to 9 months. This timeline is dictated by the speed of data preparation and the extent of regulatory queries.

The Merchant Banker conducts rigorous due diligence, and the legal team drafts the DRHP.

The DRHP is filed. SEBI (for Main Board) or the Exchange (for SME) reviews it and asks questions.

The RHP is filed, the price band is fixed, and the issue opens for the public.

Navigating the process is execution; determining the amount to raise is strategy.

Also Read: Best Crowdfunding Platforms in India 2025

Raising too little leaves you cash-strapped too soon; raising too much dilutes you unnecessarily and drags down your Return on Equity (ROE).

Follow these steps to estimate how much IPO funding you actually need:

SEBI requires specific details on how every rupee will be spent. You cannot raise "blind pool" capital for undefined future plans.

Pro tip: Map costs for specific machinery, defined debt repayment amounts, and working capital gaps for the next 18–24 months.

IPO costs (fees, marketing, printing) are deducted from the raised amount.

Pro tip: If you need ₹100 Cr net for the business, you may need to raise ₹105–₹110 Cr to cover the 5–10% issue expenses.

SEBI caps the amount you can raise for vague "General Corporate Purposes" at 25% of the total issue size.

Pro tip: Ensure 75% of your fresh issues are tied to specific, verifiable use cases like capex, debt reduction, or acquisitions.

Determining the funding amount leads directly to the most sensitive topic for founders: ownership dilution.

IPO funding is mathematically dilutive, but it should be value-accretive. When you issue Fresh Shares, the total pie gets larger, so your slice (percentage) gets smaller, even though the value of your slice hopefully increases.

For example, if you own 100% of a company valued at ₹400 Cr and raise ₹100 Cr in fresh capital, the post-money valuation becomes ₹500 Cr. You now own 80% (₹400/₹500), not 100%.

However, control is distinct from ownership. As long as the promoter group retains a controlling stake, day-to-day management remains with the founders.

The real change is in accountability: you now answer to thousands of minority shareholders and a stronger independent board.

A key factor in minimising dilution is achieving the right valuation.

A healthy IPO book is a balanced mix of different investor classes, each playing a specific role in stability and liquidity.

These are Mutual Funds, Banks, and Foreign Portfolio Investors. They are the "smart money."

High Net-worth Individuals and corporates bidding more than ₹2 Lakhs.

Small investors bidding up to ₹2 Lakhs.

Bringing these investors on board is expensive. Let's look at the hard costs.

IPO funding is cheaper than debt in the long run (no interest), but the upfront cost of entry is significant. Here are the costs involved:

Despite the costs, many companies fail to maximize the event due to avoidable errors.

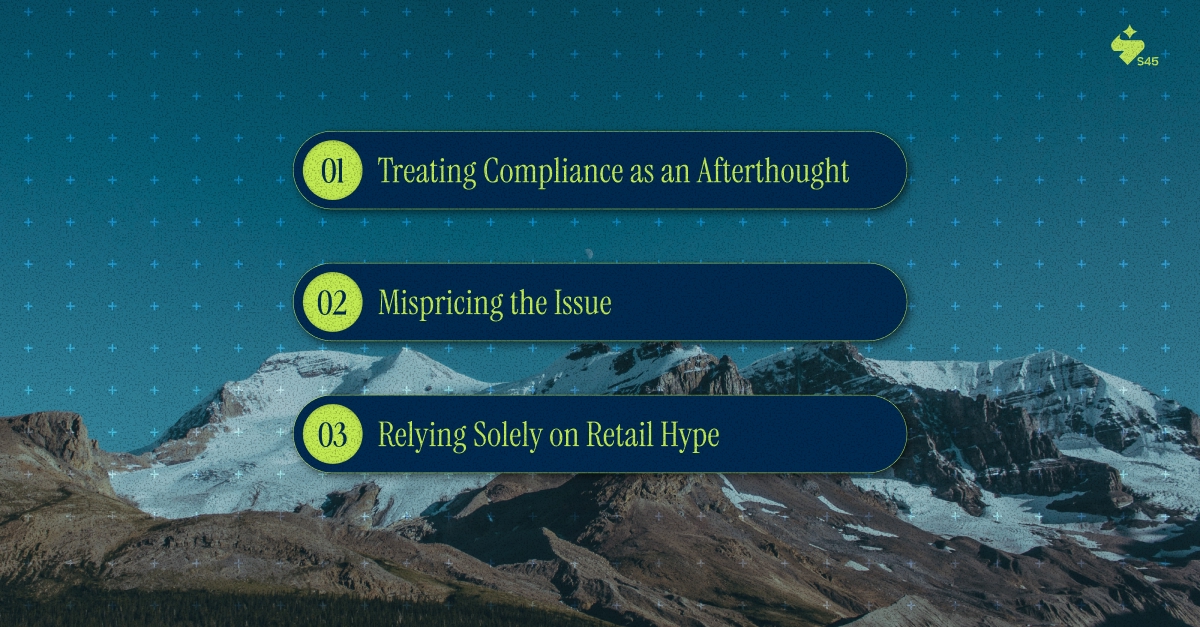

The path to an IPO is littered with companies that filed a DRHP but never listed, or listed and crashed. Below are some common mistakes companies make when planning IPO funding and how to avoid them:

Many founders rush the DRHP filing with weak internal controls or "skeleton" litigations.

Trying to squeeze every rupee of valuation often leads to a weak subscription and a discounted listing.

Ignoring institutional (QIB) outreach in favor of retail marketing creates a volatile shareholder base.

Also Read: What Is Equity Fund: Meaning and Types

Avoid the 'skeleton in the closet' that halts a DRHP. Consult our bankers to identify and resolve litigation or disclosure risks before they become public.

Avoiding mistakes is good; executing best practices is better.

To ensure not just a successful listing but a strong aftermarket performance, follow these disciplines:

Maintain a centralized, digital repository of all contracts, IP, and financial data.

For SME IPOs, a market maker is mandatory, but choosing a good one is vital.

Your DRHP is a legal document, but your roadshow presentation is a sales pitch.

The bell rings, the stock lists, what happens next?

The listing day is not the finish line; it's the start of a new chapter as a public company. How you deploy the capital and communicate with your new owners will determine your long-term market reputation and valuation.

You must now report results every quarter (or half-yearly for SMEs).

You must report to the exchange exactly how the IPO money is being spent.

You need a dedicated channel to communicate with shareholders.

Successfully managing the transition to a public company requires balancing growth with the relentless transparency mandated by the markets.

The journey to IPO funding is often portrayed as a paperwork hurdle, but in reality, it is a test of readiness, demand visibility, and execution speed. Founders frequently struggle with the opacity of the process: Are we actually eligible? What valuation is realistic? Is there real demand for our sector?

S45 operates as an AI-native investment bank designed to solve these exact uncertainties for Indian growth-stage companies. We replace the traditional "black box" of investment banking with a transparent, data-driven platform.

Our features:

We don't just execute the deal; we prepare you for the market. From the first readiness check to the 30/90-day post-listing investor relations plan, S45 ensures your transition to public markets is disciplined, compliant, and successful.

Moving from a private enterprise to a public entity is a transformative leap that provides the capital and credibility needed to scale across India’s landscape. By mastering the nuances of IPO funding, from SEBI eligibility to strategic price discovery, founders can secure the permanent capital and acquisition currency required for long-term expansion.

S45 bridges the gap between private ambition and public execution. Our AI-native platform simplifies the journey with instant readiness scans, demand mapping, and 0% upfront fees, ensuring your path to the BSE or NSE is data-driven and cost-effective.

We combine banking expertise with proprietary analytics to manage everything from DRHP filing to post-IPO investor relations, letting you focus on growth while we handle the listing.

Ready to translate your ambition into a successful public offering? Begin with clarity. Talk to a banker today and receive a data-driven assessment of your path to the public markets.

Discover more insights on similar topics