February 13, 202612 min read

Understanding Derivatives in Investment Banking: Overview, Types, and Benefits

By Aman Singh

Angel Investing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Most founders who ask about crowdfunding versus angel investing are actually asking a different question. They want to know which path gives them capital fastest, with the least dilution, and the least interference. That framing is understandable. It is also how companies end up with a capital structure that looks reasonable in year two and becomes a serious problem in year five, precisely when they are trying to go public.

But conflating these two instruments is a mistake that founders pay for years down the line, sometimes at the exact moment it matters most, which is when they are preparing for a public listing.

The difference between crowdfunding and angel investors is not just about ticket size or investor type. It is about governance structure, regulatory compliance, cap table hygiene, and the story your balance sheet tells when institutional investors and SEBI start asking hard questions. Getting clarity on this distinction is not a preliminary exercise. It is a capital strategy decision with compounding consequences.

Before a founder can make an intelligent choice, they need to understand what each of these instruments actually is, not in generic terms, but in the context of how Indian capital markets and regulators treat them.

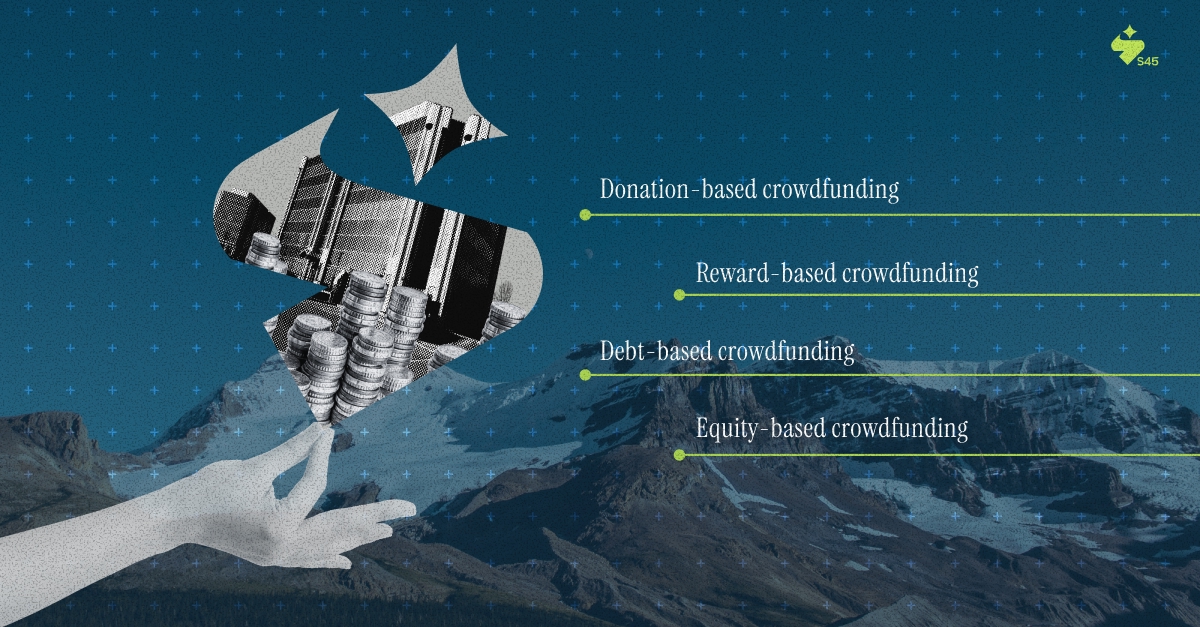

Crowdfunding, at its broadest, is the practice of pooling small contributions from a large number of individuals to fund a project or business venture. Globally, it operates in four broad models:

The critical point for Indian founders: SEBI has classified equity-based crowdfunding as "unauthorized, unregulated, and illegal" in India, citing the Securities Contracts Regulation Act, 1956. Only reward-based and donation-based models operate legally without specific SEBI oversight. This is not a gray area. It is a hard regulatory wall that eliminates crowdfunding as an equity financing option for most Indian growth-stage enterprises.

Angel investors are high-net-worth individuals who deploy their own capital into early-stage companies in exchange for equity. In India, the regulatory framework governing angel investing is shaped by SEBI's Alternative Investment Fund (AIF) regulations, the Companies Act, and tax provisions that have recently become more founder-friendly following the abolition of the angel tax in the 2024 Union Budget.

Angel funds registered as Category I AIFs under SEBI regulations pool capital from multiple investors and deploy it into startups. SEBI has also proposed raising the maximum investment limit per angel fund to Rs 25 crore and reducing the minimum ticket size to Rs 10 lakh, changes designed to deepen domestic capital participation in the Indian startup ecosystem.

Unlike crowdfunding, which is structurally distributed, angel investing is a direct relationship, with negotiated terms, defined rights, and governance expectations baked into the shareholder agreement.

The difference between crowdfunding and angel investors becomes most apparent when you map each instrument against the parameters that actually govern capital decisions in India.

Parameter | Crowdfunding | Angel Investors |

Ticket size | Small, fragmented | Rs 10 lakh to Rs 25 crore per fund |

Total capital raised | Capped; limited for equity routes | Uncapped; scalable via syndication |

India regulatory ceiling | Equity route blocked by SEBI | Governed by AIF regulations; structured |

Crowdfunding can work for early validation or reward-based pre-sales. It cannot substitute for structured equity financing in a growth-stage Indian enterprise.

This is where founders often underestimate the implications.

Crowdfunding:

Angel investing:

For a founder concerned about control and narrative ownership, neither instrument is neutral. But angel investing carries explicit governance weight that must be negotiated, documented, and managed.

One of the most significant differentiators between crowdfunding and angel investors is the non-financial value each provides.

Angel investors, particularly those with domain expertise and institutional networks, can provide:

Crowdfunding backers, by contrast, rarely contribute strategic value beyond transaction funding and, in the case of reward-based campaigns, early customer feedback.

For companies heading toward capital markets, credibility conferred by respected angel investors can strengthen the institutional narrative. The quality of early investors matters when investment bankers construct the IPO story.

Crowdfunding in India:

Angel investing in India:

Founders who shortcut documentation at the angel stage create legal and diligence risk that surfaces during IPO preparation. SEBI's review process is evidence-based. Every prior investor relationship will be examined.

The difference between crowdfunding and angel investors is not just a present-moment funding question. It is a decision that will shape the company's capital architecture over the next five to seven years.

Institutional investors and IPO regulators expect a clean, well-documented shareholder register. Fragmented ownership structures, informal investment arrangements, or undocumented angel deals create exactly the kind of noise that delays DRHP filing and increases SEBI comment rounds.

A cap table built on clear, structured angel relationships, with proper shareholder agreements and documented rights, is significantly easier to clean up and present to public market investors than one built on informal or legally ambiguous arrangements.

When investment bankers construct the IPO story, the quality and provenance of early-stage investors form part of the institutional credibility signal. A company backed by reputable angel investors from relevant sectors carries a different market perception than one without traceable institutional backing.

Every disclosure in the DRHP must be evidence-linked and traceable. Founders who treat early-stage capital arrangements casually, without proper documentation, compliance filings, or shareholder agreements, create gaps that SEBI's review process will surface. The cost of resolving documentation gaps during IPO preparation is always higher than the cost of getting the original arrangement right.

Given the regulatory constraints in India and the long-term capital market implications, here is a practical framework for evaluating which path makes sense at which stage:

For founders who are already thinking about what comes after angel funding, the path from early-stage capital to a public listing requires deliberate structural decisions at every stage.

The difference between crowdfunding and angel investors matters most not at the point of the initial capital raise but when institutional investors and regulators begin stress-testing the company's history. That is when the discipline with which early-stage capital was structured either accelerates or complicates the listing process.

India's IPO market is increasingly demanding institutional-grade readiness, not just revenue scale, but governance maturity, documentation integrity, and a capital structure that can withstand regulatory scrutiny. This applies equally to Main Board candidates and SME Exchange listings.

Firms like S45 operate at this intersection, bringing together sector bankers and proprietary AI systems to compress IPO timelines while maintaining the evidence-linked execution standards that SEBI demands. The work begins long before the DRHP. It begins with the foundational capital decisions founders make in the company's early stages.

The difference between crowdfunding and angel investors in India is not a question of preference; it is a question of legal structure, governance implications, and long-term capital market readiness. Equity crowdfunding is not a viable path in India's current regulatory framework. Reward-based crowdfunding serves a specific, limited purpose. Angel investing, when structured correctly, builds the investor base and governance foundation that institutional capital markets expect.

For founders operating in a varied revenue range and oriented toward a public listing, every early capital decision is a data point that will appear in the DRHP. The quality of those data points, how well documented, how compliant, how institutionally structured, determines how smoothly the public markets journey unfolds.

If you are at the stage where these decisions are imminent, getting clarity before committing is worth the time. Connect with S45 for a founder-level discussion on capital structure and listing viability, before the decisions are made, not after.

Discover more insights on similar topics