April 10, 20269 min read

Crowdfunding vs. Angel Investors: What Indian Founders Must Know Before Choosing a Capital Path

By Aman Singh

Angel Investing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making crucial business decisions.

Eight months into IPO preparation, a ₹300 crore manufacturer receives a SEBI query requesting explanations for derivative positions and a board-approved hedging policy. The trades exist. The policy does not. Retrofitting governance will take weeks. The IPO window narrows.

This is common across Indian mid-market enterprises. Not due to lack of sophistication, but because derivatives sit in an institutional blind spot, operational, technical, and ignored until SEBI makes them non-negotiable.

Risk does not pause for IPO readiness. FX, commodity, and interest-rate exposures continue while DRHPs are drafted and investors engaged. What was routine treasury management in a private company becomes a disclosure, audit, and valuation issue in public markets.

Most companies discover these gaps only after merchant bankers are appointed. By then, positions are fragmented, undocumented, and embedded in systems. Platforms like S45 address this by treating derivatives as listing-readiness infrastructure, not isolated trades, linking exposure, governance, and regulatory defensibility.

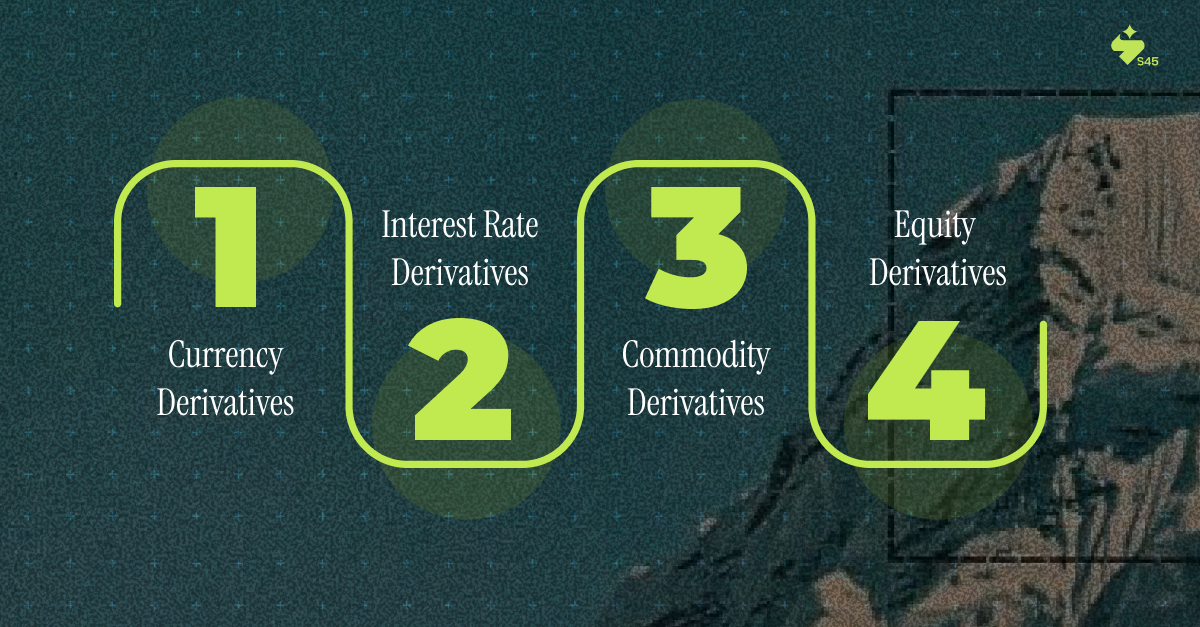

In institutional capital markets, derivatives in investment banking transfer risk from enterprises that cannot bear it to counterparties that can. Value derives from underlying assets: currency pairs, interest rate benchmarks, commodity indices, equity prices.

For Indian enterprises preparing for listing, four derivative categories matter:

The institutional test: Can you defend the derivative's economic purpose to SEBI, audit committees, and cornerstone investors? If the answer requires consultants, the position is wrong.

But definitions alone don't explain why derivatives cause such acute operational pain during IPO preparation. The issue isn't understanding what derivatives are but recognising what they represent to institutional investors evaluating your DRHP.

Traditional merchant bankers treat derivatives as a treasury footnote. Institutional investors treat them as evidence.

For SME Exchange listings, where retail participation is high, promoters often assume derivatives are unnecessary. This is wrong. The enterprises that graduate from SME to Main Board status treat SME listing as an institutional apprenticeship, not as capital-access theatre.

Platforms like S45 have observed this pattern across dozens of IPO mandates: companies that manage business risk brilliantly somehow enter IPO readiness with fragmented, undocumented, and indefensible derivative positions. The chaos manifests in disclosure failures, pricing failures, and strategy failures.

These observations point to a deeper question: if derivatives create such operational friction, why are they non-negotiable for IPO-bound enterprises? The answer lies in understanding their core institutional functions.

In institutional capital markets, derivatives are not tactical add-ons or treasury conveniences. They serve clearly defined functions that regulators, bankers, and investors evaluate during IPO preparation. Understanding these functions clarifies why the use of derivatives attracts SEBI scrutiny and how it influences disclosure quality, valuation narratives, and post-listing credibility.

The primary institutional function of derivatives in investment banking is converting uncertain cash flows into predictable outcomes. A Pune-based engineering firm exporting to Germany doesn't need to speculate on EUR/INR rates. It needs certainty on the rupee equivalent of its €2 million quarterly receivables for budgeting, capex, and earnings guidance.

This is hedging. Not trading. Not speculation.

SEBI regulations mandate that derivative positions must be backed by underlying exposure. Companies cannot take naked positions or leverage derivatives beyond actual business risk.

For CFOs preparing DRHP disclosures, the narrative must be explicit: "We entered forward contracts to hedge 75% of USD export receivables for FY24, reducing forex volatility from ₹14.2 crore to ₹3.1 crore." This is institutional language.

AI-native investment banks have begun automating this disclosure workflow, reducing the time required from 8-12 weeks of manual documentation to 2-3 weeks through evidence-linked systems that automatically map derivative positions to underlying exposures.

Derivatives manage risk without tying up working capital. Instead of maintaining dollar deposits for future import payments, a manufacturer uses forward contracts, freeing capital for inventory or growth.

This impacts IPO pricing stories. Enterprises demonstrating intelligent derivative use to optimise balance sheets command premium valuations. Those hoarding cash as volatility hedges signal operational weakness.

Derivative markets provide real-time signals about market expectations. Currency forwards embed interest rate differential expectations. Commodity futures reflect supply-demand dynamics. For IPO-bound enterprises, this intelligence informs hedging decisions: when, how much, whether to extend horizons.

But price discovery creates transparency. Mark-to-market movements appear in quarterly financials. Institutional investors scrutinise whether you're hedging intelligently or speculating poorly.

Post-listing, derivatives enable promoters, institutional investors, and employees to manage equity positions without destabilising share prices. Collar strategies, put-protected sales, and equity swaps allow orderly stake monetisation while maintaining market confidence.

For SME Exchange listings with 2-3 year promoter lock-ins, derivative strategies become essential for liquidity planning. Promoters who design exit pathways before listing retain pricing power.

These four functions explain the institutional value of derivatives. But execution requires understanding the specific instruments Indian corporates actually deploy and their operational implications during IPO preparation.

Indian corporate treasury teams use a limited set of derivative instruments, each with distinct regulatory and disclosure implications during IPO preparation. Understanding these differences is critical for building SEBI-defensible, disclosure-ready frameworks.

The simplest derivative in Indian enterprises. A forward locks in today's price for a future transaction. An exporter books a six-month forward to sell dollars at ₹84.50 when spot is ₹84.20. If the rupee strengthens to ₹83.80, the exporter still receives ₹84.50. If it weakens to ₹85.20, the exporter foregoes the gain but has certainty.

Forwards are over-the-counter instruments: customised bilateral bank agreements. This flexibility creates documentation complexity during IPO prep. Every forward requires proof of underlying exposure, board approval, and audit verification.

Exchange-traded instruments with standardised sizes, maturity dates, and settlement. The National Stock Exchange (NSE) offers currency and commodity futures, which are widely used by Indian corporates.

Futures advantage: regulatory transparency with daily mark-to-market, explicit margins, exchange-guaranteed settlement. Disadvantage: standardisation may not match actual exposure.

For IPO disclosures, futures are easier to audit and defend. Migrating from OTC forwards to exchange-traded futures during the readiness phase simplifies compliance workflows.

Options provide asymmetric payoffs: the right, not obligation, to execute a transaction. An importer worried about rupee depreciation buys a call option on USD/INR at ₹85, paying an upfront premium. If the rupee weakens to ₹87, the importer exercises at ₹85. If the rupee strengthens to ₹83, the option expires, and the importer buys at spot.

Options cost more than forwards or futures but provide flexibility. For enterprises with uncertain cash flows: seasonal businesses, project-based revenues, options prevent over-hedging.

SEBI scrutiny of options is higher because they can be speculative. CFOs must demonstrate clear linkage between option strategies and business volatility.

Interest rate and currency swaps exchange cash flows based on different benchmarks. A company with floating-rate debt at MCLR + 2.5% swaps into fixed at 9.8%, eliminating interest rate uncertainty for five years.

Swaps are powerful but complex, requiring sophisticated treasury teams, robust valuation models, and continuous monitoring. For mid-market enterprises, swaps often introduce more operational risk than they eliminate. S45's guidance: avoid swaps unless your treasury has dedicated derivatives expertise.

Understanding derivatives and their functions is necessary but insufficient. What separates enterprises that navigate IPO disclosure successfully from those that don't is having the right institutional framework in place before drafting the DRHP begins.

Institutional investors evaluate these elements when reviewing derivative disclosures:

This framework is mandatory for SEBI approval. Building it retroactively after engaging a merchant banker adds 12 to 16 weeks to the IPO timeline.

Leading investment banks now evaluate this framework within the first 30 days of engagement, deploying AI-driven documentation workflows alongside sector bankers who understand SEBI's evolving expectations. This compression from months to weeks enables enterprises to reach DRHP filing 40% faster than traditional timelines.

With the right framework in place, derivatives shift from compliance burden to strategic advantage. The benefits extend far beyond regulatory approval.

For pre-IPO enterprises, derivatives are not financial engineering tools. They are institutional risk-management mechanisms that directly influence valuation, credit perception, and market confidence. When executed correctly, their benefits extend well beyond treasury operations into core capital markets outcomes.

Institutional investors pay premium valuations for predictable businesses. A company with ₹200 crore in revenue and a 15% EBITDA margin is worth more than one with a 12-18% margin that swings with currency or commodity prices.

Effective use of derivatives in investment banking stabilises margins. That stability translates into valuation multiples. Companies with 20-30% valuation differentials based solely on earnings predictability through effective hedging are common.

For enterprises raising debt alongside equity: common in infrastructure, manufacturing, and real estate, derivative usage impacts credit ratings. Rating agencies evaluate risk management frameworks. Companies with documented hedging policies receive better ratings than those exposed to unmitigated risk.

Better ratings mean lower debt cost, improving return on equity and supporting higher listing valuations.

In thin-margin sectors: textiles, chemicals, manufacturing: locking in input costs or output prices creates a competitive advantage. A chemical manufacturer hedging crude oil derivatives can quote fixed prices while competitors expose themselves to volatile spot markets.

This operational superiority becomes a source of disclosure strength during IPO marketing.

Founders approaching public markets face psychological pressure: loss of control, quarterly scrutiny, and valuation debates. Effective derivative strategies reduce a major source of stress: P&L uncertainty from uncontrollable factors (currency rates, interest rates, commodity prices).

When promoters enter roadshows confident that quarterly results won't be destroyed by rupee volatility, that confidence translates into better investor conversations and stronger anchor commitments.

But no institutional tool is without risk. Derivatives introduce complexity that must be managed, not ignored.

Derivatives introduce complexity, creating operational, accounting, and reputational risk. For mid-market enterprises without dedicated treasury teams, risks can outweigh benefits.

Modern investment banking platforms treat these as workflow problems, not conceptual barriers. AI-driven DRHP drafting systems automatically generate hedge accounting disclosures, link derivative positions to risk factors, and create defensible narratives around mark-to-market movements.

Understanding risks is half the battle. The other half is understanding how SEBI's regulatory framework shapes what's permissible and what's required.

The Securities and Exchange Board of India maintains specific guidelines on corporate derivative usage. The regulatory framework requires underlying exposure (all positions must be backed by actual business exposure), board oversight (risk policies must be approved, reviewed annually, and disclosed), audit verification (auditors must verify positions comply with policies), and disclosure requirements (listed companies must disclose positions in financial statements).

For enterprises in IPO readiness, SEBI's requirements become your template. Build internal frameworks to match the listed company standards before DRHP filing. This eliminates regulatory queries and accelerates approvals.

Capital market execution platforms integrate SEBI compliance into every IPO preparation stage, flagging non-compliant positions, generating compliant disclosure language, and coordinating with auditors to ensure verification occurs in parallel with DRHP drafting.

The principles apply uniformly across the Main Board and SME Exchange contexts, though many mid-market enterprises mistakenly assume different standards.

For Indian enterprises preparing for public markets, derivatives in investment banking convert business uncertainty into capital market credibility.

The enterprises that reach listing fastest, price the highest, and trade most stably treat risk management as evidence of institutional readiness. Derivatives, used properly, documented rigorously, disclosed transparently, provide that evidence.

Those struggling attempt to retrofit derivative frameworks after engaging merchant bankers. By then, chaos is embedded. Timelines extend. Valuations suffer.

If your enterprise generates ₹80 to 800 crore in revenue, faces material currency or commodity exposure, and is considering Main Board or SME Exchange listing within 24 months, the derivative question isn't whether but how well. The answer determines whether your IPO takes 4 months or 10 months, whether your valuation reflects strategic sophistication or operational immaturity, and whether post-listing performance demonstrates stability or creates volatility that depresses trading multiples.

Before committing months of preparation and institutional reputation to the IPO process, get clarity on whether your derivative framework meets institutional thresholds. S45's IPO Readiness Scan provides a systematic evaluation of capital markets readiness in 30 days, identifying gaps that extend timelines and compress valuations before they become costly surprises.

Discover more insights on similar topics