April 10, 20269 min read

Crowdfunding vs. Angel Investors: What Indian Founders Must Know Before Choosing a Capital Path

By Aman Singh

Angel Investing

As a startup founder, creating effective contracts with angel investors is crucial to securing both capital and long-term business growth. The recent 50% drop in profits for Angel One highlights how quickly market and regulatory changes can disrupt a business.

For entrepreneurs, angel investor contracts must include provisions that protect both the investor’s capital and the business itself in case of significant market shifts or regulatory changes. This is especially true when diversifying into more stable revenue streams, like asset management and insurance, to mitigate financial risk.

This blog breaks down the real pain points and shows you how to create effective angel investor contracts that protect your interests and lay the foundation for healthy growth.

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Many founders approach angel deals reactively, focusing on valuation and ignoring the agreement's structure. But the structure, how equity is issued, when it converts, and the rights attached, are more important than the headline valuation.

The three core structures that you'll encounter are:

Choose the structure that aligns with your business reality. But real clauses are often buried under pages of your agreement. How would you know which one to check first?

Most founders skim through agreement sections, trusting their lawyer to flag any issues. That's a mistake. Your lawyer protects you legally; you need to protect your business strategically. Here are the critical clauses you should not miss:

Anti-dilution clauses protect investors if future rounds happen at lower valuations (a "down round"). However, this protection comes from your equity, not thin air.

Negotiation Tip: Push for weighted average (broad-based, not narrow). Better yet, negotiate a carve-out: anti-dilution only triggers if the down round exceeds a minimum threshold (e.g., ₹1 crore). This protects your cap table from small bridge rounds.

In an exit (acquisition or IPO), liquidation preferences decide the payout order.

These clauses can turn a modest exit into a disaster. For example, with 2x participating preference on a ₹6 crore exit, angels take ₹4 crore plus 20% of the remaining ₹2 crore. You’re left with ₹1.6 crore despite owning 80%.

Negotiation Tip: Always aim for 1x non-participating preferences. If angels insist on participating or multiple preferences, their risk perception is off. Walk away.

Drag-along rights are investor-friendly but reasonable if the approval threshold is high (75%+). Ensure founder shares have enhanced voting rights to maintain veto power over strategic decisions.

Angels often request board seats or observer rights, which isn't bad if balanced. A typical early-stage MSME structure:

"Reserved matters" should only include major decisions: raising debt, selling the company, changing the business scope, or issuing new equity. Founders should retain control over day-to-day operations, hiring, pricing, and product decisions.

Negotiation Tip: If investors can block operational decisions, you’re an employee, not a founder. Keep control where it counts.

Now that we’ve established the importance of favorable investment terms, let's see the key clauses that govern your exit strategy, ensuring you're in control of your future decisions.

Theory is useless without execution. Here's the exact process for structuring agreements that protect your interests while closing the deal.

Draft a term sheet, a non-binding summary of key terms. This single document prevents expensive legal back-and-forth later. Your term sheet should cover:

Negotiate here, not in 40-page legal documents. Once the term sheet is signed, lawyers execute; they don't renegotiate.

Your company secretary isn't enough. You need a lawyer who specializes in startup/MSME funding transactions. They should draft or review:

Expect to pay ₹1.5-3 lakh for quality legal work. This isn't an expense; it's insurance against ₹10 crore mistakes.

Angels will audit your business. Expect 2-4 weeks of document requests: financials, tax filings, customer contracts, IP ownership, litigation history, and cap table clarity. Be organized. Diligence delays signal operational chaos, and investors walk away.

Simultaneously, conduct reverse diligence. Who else has this angel invested in? Call those founders. Ask direct questions:

Bad angels are worse than no angels. A strategic partnership with S45 can help you close with an angel who has a reputation for hostile takeovers during distress. A single reference call saved his company.

Post-signing, you have filing obligations:

Miss these deadlines, and you're non-compliant, creating headaches for future fundraisers.

Your agreement is only as good as its execution. Set up:

Transparent communication builds trust. Trust makes future rounds and tough decisions easier.

Exit strategies are critical for ensuring you retain control, but no agreement is complete without considering the complex regulatory landscape that impacts angel investments, especially in India.

India’s regulatory framework for angel investments is clear if you know the rules, but complex if you don’t. Here’s what every MSME founder needs to understand:

All equity issuances must comply with the Companies Act. Key provisions include:

Angel Tax is a silent risk. Get a valuation report from a registered valuer (₹25,000-50,000) to justify pricing. This document can save you from tax notices and legal fees that could reach ₹20-30 lakh.

If your angel is an NRI or foreign investor, FEMA applies:

FEMA violations can block future foreign funding. Plan for an extra 4-6 weeks for compliance if targeting NRI angels.

SEBI regulations apply once you have 200+ shareholders or raise funds publicly. For angel rounds, you're generally safe. However, if an angel invests via an Alternative Investment Fund (AIF), be aware of the additional disclosure and governance requirements for portfolio companies.

The regulatory framework is there to protect investors, not block your growth. At S45, we help founders navigate these requirements to keep momentum going.

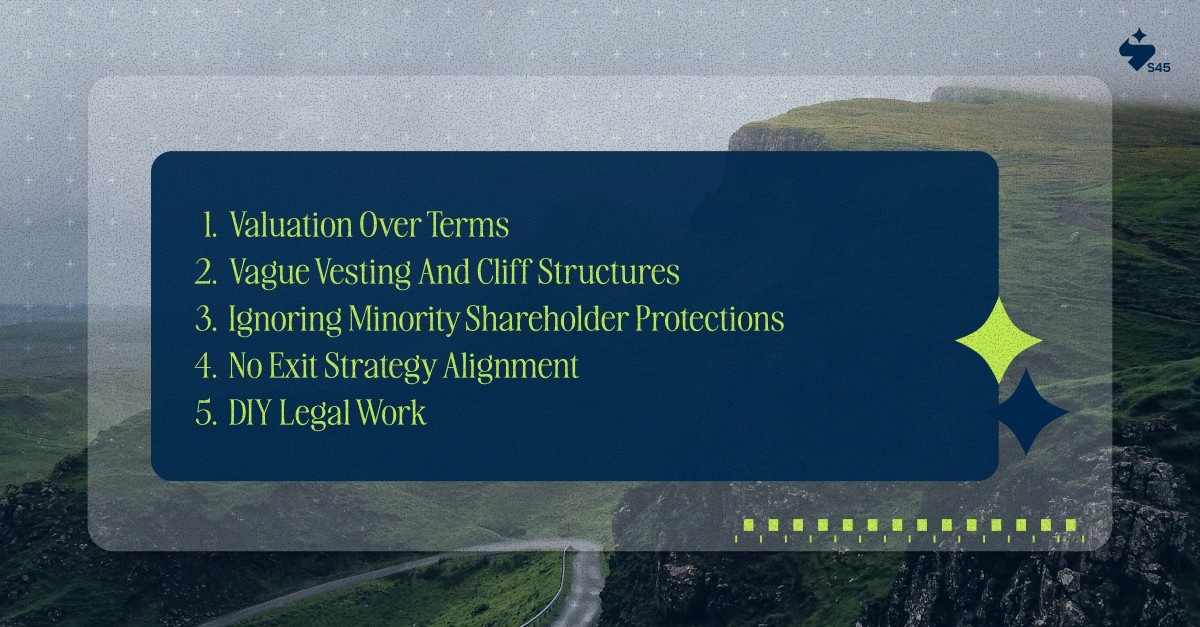

As you execute your investment strategy, being aware of common pitfalls can help you avoid mistakes that undermine your ownership and future growth potential.

Even seasoned founders make mistakes. Here are the traps we've seen most often—and how to avoid them.

Scaling an MSME requires not only the right capital but the right structure. Partnering with experienced investors who understand your challenges can make all the difference.

Scaling an MSME is about more than capital; it’s about building structures that support sustainable growth. Angel agreements are key to that foundation. Get them right, and you unlock resources, networks, and expertise. Get them wrong, and you’ll spend years fixing mistakes.

At S45, we partner with founders who are serious about scaling. We don’t just write checks; we help structure deals that align incentives, navigate regulatory complexities, and position businesses for institutional rounds. With hundreds of transactions closed, our network of operators, investors, and advisors brings invaluable experience to every partnership.

If you’re raising your first angel round or restructuring a cap table, let’s talk. We help founders protect what they've built while enabling future growth.

Ready to structure your next round? Connect with S45 and explore how we can support your journey.

Discover more insights on similar topics