April 1, 202610 min read

Third-Party Funding in Indian Arbitration: What You Need to Know

By Abhishek Bhanushali

Finance Advice

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

The breakdown doesn't announce itself dramatically. There's no single moment when an IPO derails. Instead, delays accumulate quietly across fragmented workflows.

A DRHP section awaits legal review for three weeks. Evidence documentation is incomplete because no one has defined what "complete" means. Pricing discussions stall because comparable analysis lacks institutional rigour. Board presentations slide into the next quarter because SEBI observations triggered another documentation cycle.

By the time promoters recognise the pattern, six months have been lost to coordination overhead. The market window that justified listing urgency has shifted. What began as a strategic capital-markets entry has become an operational endurance test.

This isn't about banker incompetence or founder unpreparedness. It's a structural mismatch between legacy advisory models and the current pace of capital markets. India witnessed 80 mainboard IPOs in FY25, raising ₹1,630 billion, whilst SEBI compressed approval timelines to three months from six. The regulatory infrastructure accelerated. Most investment banking workflows did not.

The investment banking future addresses this gap through rebuilt execution models in which AI handles mechanical precision and seasoned bankers' strategic judgement. Where evidence architecture precedes DRHP drafting. Where compliance becomes structural discipline embedded in preparation, nota defensive scramble during regulatory review.

The gap between "we're ready to list" and "SEBI has approved our DRHP" is revealed by operational details most promoters don't anticipate.

Material contracts exist but aren't catalogued systematically. Financial performance is strong, but comparable company analysis lacks institutional depth. Governance structures function effectively, but don't align with LODR disclosure requirements. Growth narratives are compelling, but evidence linkages remain undocumented.

That disconnect is most evident in the timeline itself. What should be a controlled preparation phase turns into a reactive, month-by-month scramble:

The investment banking future compresses this timeline not through corner-cutting but through structural redesign. Firms like S45 pair AI-driven documentation systems with seasoned sector bankers to collapse mechanical work whilst preserving strategic judgement. When evidence architecture precedes drafting, and SEBI frameworks inform preparation from day one, the mandate-to-DRHP timeline compresses from 4-6 months to 30-45 days.

Understanding where the future of investment banking diverges from traditional models requires examining specific operational transformations already reshaping India's capital markets.

SEBI's ICDR and LODR frameworks don't accept narrative assertions. They require documented proof. When a DRHP cites market share, it must reference independent research. When it claims technological differentiation, it must reference patents or contracts. When it projects the addressable market size, the methodology must be traceable.

Traditional investment banking approaches this through manual aggregation of research. AI-native systems scan source documents, extract relevant data, verify claim-evidence linkages, and flag documentation gaps before drafting begins. Every disclosure becomes an evidence node with traceable provenance, not an editorial choice requiring post-facto validation.

For promoters, board presentations asserting "leading position in our segment" require supporting data before they can become DRHP language. Growth narratives built on management conviction need independent validation before regulatory filing.

SEBI's regulatory framework isn't constrained. Its structure. SEBI undertook a comprehensive regulatory overhaul in 2025, introducing amendments across ICDR and LODR regulations, issue size norms, anchor investor participation, and promoter holding requirements.

Compliance-late founders pay predictable premiums: timeline delays, documentation rework, and pricing pressure all accumulate when regulatory requirements are engaged reactively during SEBI review rather than proactively during preparation.

The investment banking future treats SEBI frameworks as design parameters from day one. ICDR disclosure requirements inform DRHP structure. LODR continuing obligations shape post-listing readiness. Lock-in norms influence promoter holding optimisation. This isn't about gaming regulatory review; it's about institutional alignment.

AI doesn't make listing decisions. It doesn't assess promoter quality. It doesn't evaluate sector timing. These remain banker functions requiring pattern recognition across market cycles.

AI compresses mechanical work that traditionally consumes 60-70% of IPO preparation timelines: DRHP drafting, disclosure tracking, evidence linking, and pricing analysis. According to industry analysis, AI-based systems now process up to 100 times more data per second than conventional platforms.

But the critical insight isn't velocity. It's judgement preservation. When AI handles mechanical precision, bankers spend their time on what machines cannot do: assessing whether the enterprise should list now or later, whether the Main Board or the SME makes strategic sense, and whether pricing ambitions align with market reality.

Traditional investment banking operates under a diffused responsibility model. Legal counsel handles documentation. Merchant bankers manage the regulatory interface. Financial advisors develop valuation models. When SEBI raises observations, when pricing misses expectations, when post-listing liquidity disappoints, responsibility fragments.

The future of investment banking consolidates accountability vertically. Institutions own IPO outcomes end-to-end from readiness assessment through DRHP filing, SEBI navigation, pricing strategy, and post-listing liquidity design. This isn't expanded scope; it's rebuilt accountability where the deliverable isn't advice but a listed company with institutional-grade documentation, defensible pricing, and sustainable liquidity.

The structural shifts described above aren't responding to theoretical scenarios. They're operational requirements driven by the evolution of India's capital markets.

India led global capital markets in 2024 with 327 IPOs raising $19.9 billion. The NSE topped global exchanges for funds raised, surpassing NASDAQ. Median P/E ratios stood at 21.5x versus 14x in the US, reflecting strong investor appetite.

SEBI now approves the majority of IPOs within three months of filing, down from six months previously. Approximately $18.7 billion worth of IPOs await regulatory approval.

This acceleration creates both opportunity and exposure. Enterprises with institutional-grade readiness access markets during favourable windows. Those prepared operationally but not documentationally miss cycles whilst competitors advance. The gap between traditional advisory and outcome-owned execution has widened to decision-critical levels. Choosing incorrectly costs quarters, not weeks.

Understanding the future of investment banking requires examining specific operational transformations. The DRHP creation process illustrates this precisely.

Merchant banker outlines structure. The company provides data. Drafting teams write sections sequentially over weeks. Legal counsel reviews. Multiple revision cycles address gaps. Output quality varies based on coordination effectiveness.

Documentation gaps emerge during SEBI review because the evidence architecture was never systematically built. The timeline stretches because mechanical work occurs sequentially rather than systematically.

The compression isn't about speed alone. When evidence architecture precedes drafting, every disclosure has traceable provenance. When AI handles mechanical consistency, bankers focus on strategic judgement. When regulatory frameworks inform structure from day one, SEBI observation cycles decrease substantially.

For CFOs managing IPO preparation alongside business operations, less time coordinating document workflows means more time running the enterprise. Faster DRHP development means board decisions on listing timing can respond to market windows rather than preparation constraints.

One of the most consequential decisions enterprises face is listing venue selection. The investment banking future approaches this not as capability assessment ("do we qualify?") but as strategic optionality ("which pathway serves our capital objectives?").

Suited for:

Key considerations:

Suited for:

Key regulatory parameters: SEBI introduced ₹1 crore EBITDA requirements for two of the last three years and limited OFS to 20% of the issue size. These frameworks calibrate market access for emerging enterprises whilst maintaining investor protection standards.

Here's where pathway selection intersects directly with the investment banking future and outcome ownership models.

SME listings face structural liquidity challenges that Main Board issuances do not: narrower institutional participation, less analyst coverage, and shallower market-making infrastructure. Without deliberate liquidity design, many SME IPOs succeed on listing day but fail to sustain trading volumes three months later.

Institutions like S45 treat post-listing liquidity as a core deliverable for SME pathways, not a peripheral concern. This means pre-listing market-maker commitments secured during preparation, systematic investor relations programmes, and strategic corporate action calendars designed to maintain market engagement. For Main Board candidates, the focus shifts to institutional investor engagement, QIB allocation strategy, and pricing discipline.

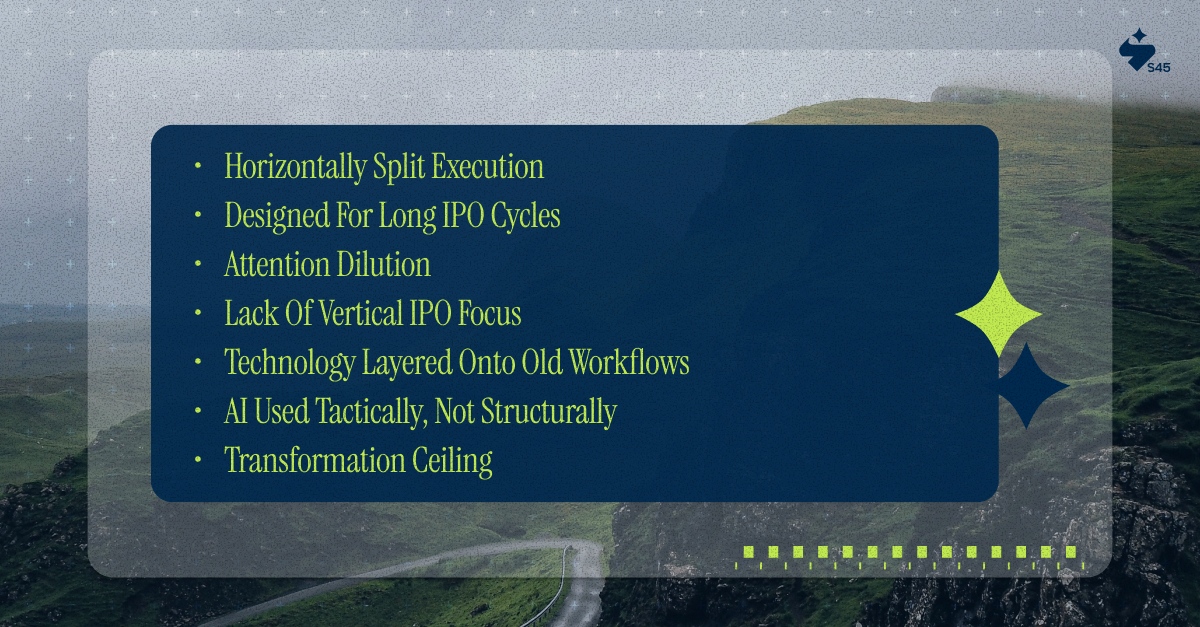

What slows traditional investment banking today isn’t mindset or talent. It’s structural design built for a slower market era.

If you're operating an enterprise with ₹80-800+ crore in revenue and contemplating capital markets entry, the investment banking landscape offers options that prior cohorts didn't face.

The bar moved from "good enough for eventual listing" to "SEBI-ready before mandate engagement." Enterprises succeeding in current IPO cycles built their evidence architecture before engaging investment banks: board packs with audited financials readily accessible, material contracts in systematic repositories, regulatory licences tracked contemporaneously, and corporate governance documented as decisions happen.

SEBI's three-month approval cycle creates stark division: Institutionally prepared enterprises move from board decision to listing in 5-7 months. Enterprises that identify gaps during preparation face delays of 12-18 months, despite identical regulatory approval times. The difference is the readiness state when engaging the capital markets infrastructure.

Traditional investment banks offer process familiarity and relationship networks. AI-native institutions offer outcome ownership and timeline compression. Choose traditional advisory if you need guidance navigating known processes, and timeline pressure is minimal. Choose outcome-owned execution if documentation velocity determines market window capture and you prefer single-point accountability over specialist coordination.

Being listed solves for capital access and brand credibility. It doesn't automatically solve for liquidity, analyst coverage, or sustained market attention. This is particularly critical for SME Exchange candidates, where liquidity infrastructure requires deliberate design rather than market-driven emergence.

The future of investment banking in India isn't a distant prospect. It's operationally present in today's capital markets, enabling enterprise access.

Current institutional expectations didn't exist five years ago: evidence-linked disclosures traceable to source documentation, AI-compressed preparation timelines measured in weeks rather than quarters, SEBI's heightened scrutiny requiring structural compliance, and post-listing liquidity requirements extending beyond listing day.

Choosing incorrectly costs quarters of market opportunity. The difference between fragmented specialist inputs and full-cycle institutional accountability determines whether enterprises access capital markets during optimal windows or miss them whilst competitors advance.

The capital markets don't accommodate operational unpreparedness. They allocate opportunity to enterprises demonstrating institutional readiness measured by documentation quality, regulatory alignment, and execution velocity.

If you've built an enterprise worth taking public, the strategic question isn't whether to engage capital markets infrastructure. It's whether the infrastructure you engage owns the outcome you need and delivers it at the velocity markets demand.

For institutional-grade IPO readiness assessments before committing board time to public markets timelines, S45 works with enterprises with ₹80-800+ crore in revenue, evaluating listing pathways.

Discover more insights on similar topics