April 1, 202610 min read

Third-Party Funding in Indian Arbitration: What You Need to Know

By Abhishek Bhanushali

Finance Advice

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Three bidders make it to the final round. Months of diligence are complete. The board is aligned. Then the preferred bidder pulls out, not over valuation, but because debt financing doesn't come through on time.

What follows is familiar. Competitive pressure vanishes, timelines slip, and the seller accepts a lower offer, often ₹50–150 crore below fair value, simply because committed capital feels safer than a higher bid dependent on uncertain financing. The business hasn’t changed. The market hasn’t turned. The value erosion is purely structural.

Investment banks working on Indian mid-market M&A, including capital-markets-focused firms like S45, repeatedly see this pattern. Buyer financing is treated as a bidder problem until it becomes a seller crisis. Staple financing can help close that execution gap.

Staple financing refers to a pre-arranged debt package organized by the seller's investment bank and made available to all potential bidders in an M&A auction. The term derives from stapling the financing commitment letter to the back of the acquisition memorandum. The package specifies principal, interest rates, fees, covenants, and repayment terms before bidding begins.

Staple financing serves as a strategic catalyst in M&A, transforming a conditional auction into a high-velocity race to close. By removing the "subject to financing" contingency, it provides a standardized capital foundation that shifts the focus from debt discovery to valuation.

By addressing financing upfront, staple financing prevents late-stage bidder dropouts. Sellers maintain competitive tension through exclusivity, and buyers submit offers backed by realistic, fundable capital structures, not assumptions that unravel post-selection.

With debt terms visible early, buyers can move faster and commit with confidence, while sellers avoid prolonged processes and exposure to shifting credit conditions that can derail transactions after months of diligence.

Staple financing allows a broader pool of bidders, particularly strategic buyers without dedicated leveraged finance desks, to compete effectively against large private equity funds. This increased competition typically drives higher multiples and better terms for the promoter.

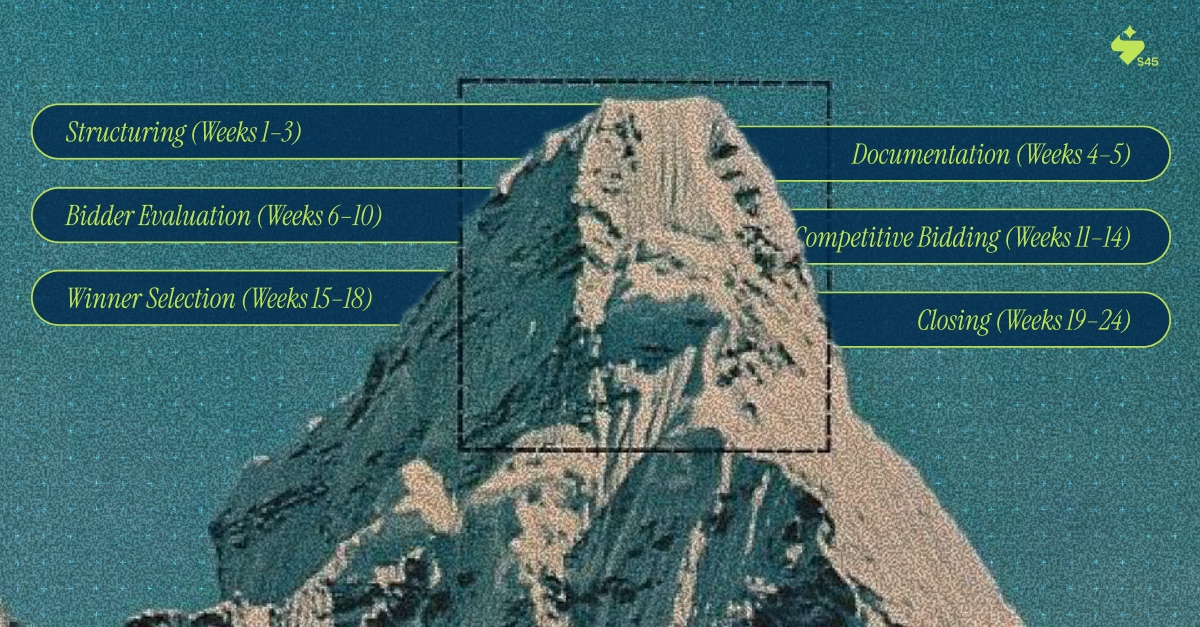

Understanding the mechanism requires walking through the operational sequence from seller engagement to transaction close. Each phase has specific deliverables and timeline implications:

The seller and the advisory bank assess whether staple financing makes strategic sense, considering the bidder's profile, timeline pressures, and debt capacity. If affirmative, the bank engages lenders to structure a preliminary package, typically 4x–6x EBITDA in Indian markets.

Commitment letters and term sheets detail principal, interest rates (MCLR plus spread), tenure, security, and covenants. This documentation accompanies the Confidential Information Memorandum in the virtual data room.

Bidders receive the CIM and staple package simultaneously, eliminating parallel lender negotiations. This compresses timelines by 60–90 days compared with conditional bids that require post-selection financing.

Equal access to debt makes the auction purely about equity value. The staple amount signals valuation expectations; if offering ₹400 crore at 5.5x EBITDA, bidders infer an enterprise value range of ₹550–650 crore.

The preferred bidder can accept or decline the staple financing. Many sophisticated buyers decline it, but the option ensured credible bidding without financing risk.

If accepted, debt funding flows simultaneously with equity consideration. Transaction execution risk drops dramatically.

Also Read: The Essential Credit Funding Guide for Indian SMEs: Scores, Risks & Smarter Decisions

The practical application becomes clearer through examining actual transactions where staple financing played a decisive role in execution:

Michael Foods Transaction (US, 2010): Thomas H. Lee Partners sold Michael Foods to GS Capital Partners for USD 1.7 billion. Bank of America Merrill Lynch served as advisor and arranged staple financing. The transaction was completed in under six months, materially faster than comparable carve-outs.

Hillman Group Acquisition (US, 2010): Oak Hill Capital Partners acquired Hillman Group for USD 815 million. Barclays Capital advised the seller while providing debt financing to bidders, ensuring multiple private equity firms could compete on an equal footing despite varying lender relationships.

These transactions share common characteristics: competitive auctions, a focus on financial buyers, significant leverage requirements, and time pressure that favors execution certainty.

Despite its proven value in Western markets, staple financing hasn't achieved widespread adoption in Indian mid-market M&A. Several structural factors explain this gap:

As Indian mid-market M&A matures, expect increased adoption of PE-to-PE secondaries, family office acquisitions, and time-sensitive sales where execution certainty justifies more complex structuring. Advisors focused on capital markets execution, such as S45, which operates at the intersection of IPO readiness and strategic M&A, increasingly assess staple financing as a workflow tool for specific transaction scenarios rather than a universal practice.

The most substantive criticism of staple financing centers on a structural issue that cannot be eliminated but can only be managed: the investment bank advising the seller simultaneously provides financing to the buyer.

Conflict 1: Pricing Incentives: The bank must maximize the sale price for the seller while also earning fees from the buyer's debt. It might structure aggressive leverage, favoring buyer economics over seller value.

Conflict 2: Buyer Recommendation Bias: If only one bidder commits to the staple financing, the bank might favor that bidder to earn arrangement fees, even if another offer is economically superior.

These conflicts are manageable:

For Indian mid-market companies, the conflict demands board-level discussion. The company secretary, independent directors, and audit committee should review the structure and ensure that documented safeguards are in place.

Must Read: Investment Banking in India: Roles, Growth Opportunities & How to Get Started

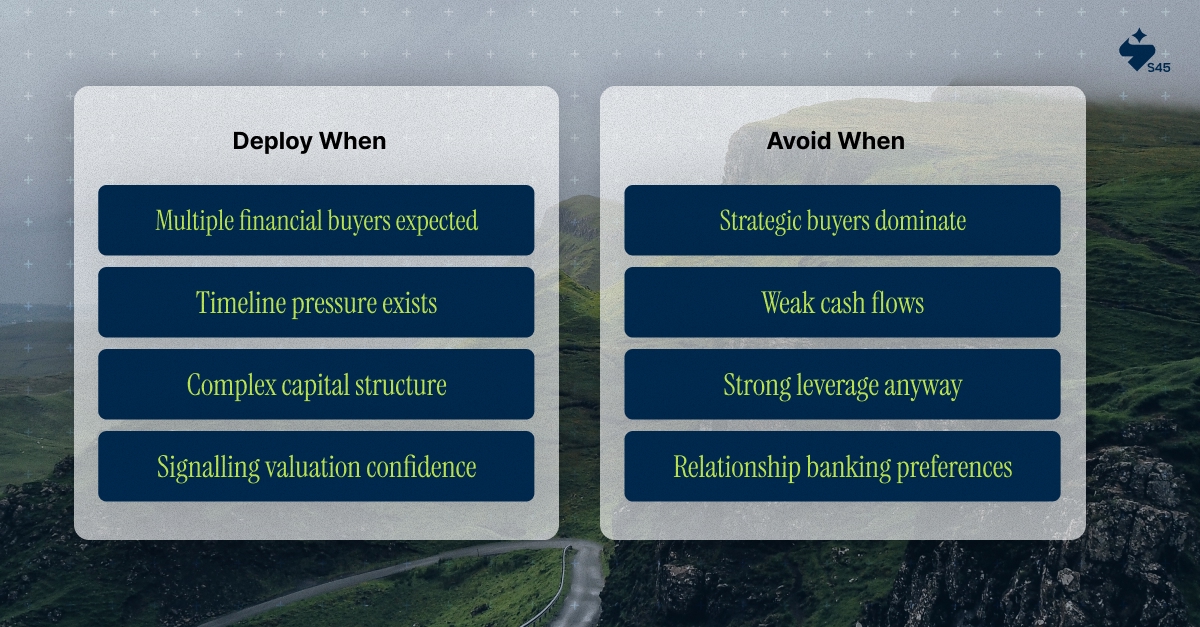

The decision to employ staple financing should be driven by specific transaction characteristics, not by imitation of Western practices or perceived sophistication:

Deploy When:

Avoid When:

The deployment decision should be evidence-based: quantifying the value of timeline compression, mapping actual bidder financing needs, and assessing the board's tolerance for disclosed conflicts. Execution-focused advisors evaluate staple financing through three lenses: bidder profile analysis, timeline value quantification, and conflict management capability, before recommending deployment.

Staple financing eliminates one specific execution risk: financing uncertainty that kills competitive tension in M&A auctions. For Indian mid-market companies, this matters because the mechanism separates institutional execution from improvised process.

The structure works by providing all qualified bidders with pre-negotiated debt access with clearly specified terms. This removes the execution risk that causes capable buyers to withdraw mid-process, compresses timelines by 60–90 days, and signals credible valuation expectations. The trade-off is managing conflicts through information barriers, third-party lenders, and rigorous board-level disclosure.

As financial buyers expand their presence in Indian mid-market M&A and private credit providers build India-focused platforms, companies that understand staple financing early will have execution optionality when market windows open.

S45 works with Indian mid-market enterprises on capital structure assessment and execution architecture for strategic sales, institutional capital raises, and IPO preparation. Connect with an S45 partner to build your execution roadmap today.

Discover more insights on similar topics