April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Most liquidity crises do not announce themselves. They build quietly, in the gap between how a bank funds itself today and how it needs to fund itself over the next twelve months. When that gap widens fast, especially during a period of market stress, the consequences move well beyond individual institutions.

That is the exact problem the net stable funding ratio was designed to address. Born out of the 2007-2008 global financial crisis, the NSFR is a structural liquidity standard under Basel III that forces banks to match the stability of their funding sources against the liquidity risk embedded in their asset portfolios.

For Indian promoters, CFOs, and board members of enterprises in the capital markets pipeline, this matters more than it appears at first glance. The banks financing your working capital, the institutions underwriting your listing, the NBFCs structuring your pre-IPO rounds: all are subject to NSFR. Understanding it means understanding how credit is priced, how counterparty capacity is calculated, and why institutional lenders behave the way they do under regulatory stress.

This blog explores how the net stable funding ratio shapes the broader capital environment around you. From how banks assess balance sheet risk to how institutions allocate lending capacity, the focus is on understanding the structural forces that influence credit availability, pricing, and deal execution, factors that directly impact any company preparing for a public listing.

The net stable funding ratio is a liquidity regulation that requires a bank's available stable funding to meet or exceed its required stable funding over a one-year stress horizon. In simple terms, it asks: if your primary funding sources dried up, could your balance sheet sustain itself for twelve months?

The NSFR became a minimum standard globally on January 1, 2018, under the Basel III framework published by the Bank for International Settlements (BIS). India's Reserve Bank of India implemented the standard via its circular, with the effective date ultimately set as October 1, 2021.

For companies operating in or approaching capital markets, these regulatory shifts are not abstract. They shape how financial institutions behave in real-world transactions, something firms like S45 factor into how they evaluate institutional readiness and capital strategy.

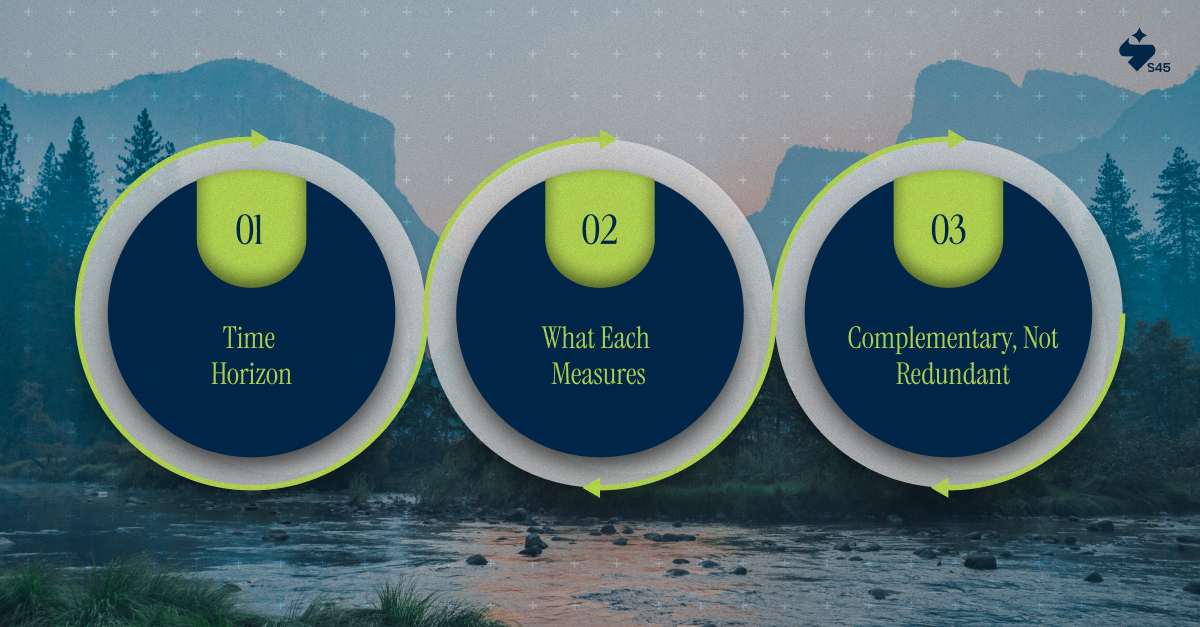

Basel III introduced two complementary liquidity standards that serve distinct purposes:

The two ratios are not substitutes. LCR is the emergency oxygen mask. NSFR is the structural integrity of the aircraft.

Understanding the NSFR starts with its formula. The calculation is straightforward in concept, but the weight assignments require precision.

NSFR = Available Stable Funding (ASF) / Required Stable Funding (RSF) >= 100%

Per the BIS standard and RBI guidelines, this ratio must be equal to or greater than 100% at all times. A ratio below 100% signals a structural funding shortfall.

ASF represents the portion of a bank's capital and liabilities expected to remain with the institution for more than one year. Each funding source is assigned an ASF factor based on its stability:

RSF represents the minimum amount of stable funding a bank must hold, based on the liquidity characteristics and residual maturities of its assets. RSF factors range from 0% to 100%:

RBI has prescribed specific RSF factor variations for Indian conditions, including higher RSF factors for agricultural crop loan NPAs and specific treatment of State Development Loans (SDLs).

India's implementation of the net stable funding ratio closely follows the BIS standard, while accommodating certain domestic-specificities. Here is what CFOs and board members of enterprises in the capital markets pipeline need to know.

Per the RBI circular (DOR.BP.BC.No.16/21.04.098/2020-21), the NSFR framework applies to:

As per PwC's regulatory analysis of RBI's NSFR guidelines, banks are required to:

The Basel Committee's RCAP assessment of India's NSFR identified two areas where India's implementation differs from the BIS standard:

Despite these deviations, India's NSFR regulations are assessed as compliant with the Basel NSFR standard, earning a higher overall grade.

If you are a promoter or CFO preparing your enterprise for a Main Board or SME Exchange listing, you may wonder why a banking regulation belongs in your IPO readiness checklist. The answer lies in how NSFR shapes the behavior of every institutional actor in your capital markets journey.

NSFR changes the cost structure of long-term lending. Banks subject to tighter stable funding requirements tend to price long-dated credit more carefully and shift capacity toward assets that require less stable funding. For mid-market enterprises in the pre-IPO phase relying on term loans or structured debt, this has direct implications for both pricing and tenor.

Lead managers, underwriters, and investment banks are themselves subject to NSFR if they are part of scheduled commercial banking groups. Their ability to provide firm commitments, bridge finance, or price-discovery support is a function of their balance-sheet capacity, shaped by NSFR compliance.

This is precisely where an AI-native capital markets firm like S45 operates differently. By pairing proprietary technology with sector banker judgment, S45 builds IPO execution models that account for institutional capacity constraints, rather than assuming unlimited underwriting bandwidth.

For SME Exchange listings, post-listing liquidity is one of the most structurally underprepared elements of an IPO. Market makers, designated liquidity providers, and institutional participation are all functions of balance-sheet capacity, governed in part by NSFR. An enterprise that enters its listing phase without understanding this dynamic will find itself with thin secondary market support precisely when it needs it most.

A common source of confusion is treating NSFR and LCR as interchangeable. They are not. Each addresses a different dimension of liquidity risk.

A bank can have a healthy LCR and still fail NSFR compliance if its funding structure relies excessively on short-term wholesale markets. The 2007-2008 crisis demonstrated that precisely: institutions appeared liquid in the short term but were structurally fragile. NSFR was designed to close that exact gap.

The net stable funding ratio is not a theoretical concept. Every scheduled commercial bank in India discloses its NSFR quarterly. Understanding what healthy NSFR compliance looks like in practice helps enterprises evaluate the institutional partners backing their capital markets transactions.

The most stable sources of funding, attracting the highest ASF factors, include:

Conversely, funding structures that reduce NSFR compliance typically include:

The adoption of NSFR does not operate in isolation. It reshapes how banks allocate capital, price risk, and structure their balance sheets. These shifts ripple through to every enterprise that relies on institutional banking for growth or capital markets access.

As analyzed in academic research on NSFR and Indian bank performance (MDPI, 2022), NSFR compliance incentivizes banks to rely more on stable retail deposits and long-term borrowings, reducing dependence on short-term wholesale funding. For enterprises, this means your banking partner's funding model becomes more stable over time, but may also mean reduced flexibility in short-term structured products.

NSFR forces banks to match the duration of their funding against the liquidity profile of their assets. This is institutional discipline at its most structural. Banks with poor asset-liability management face direct NSFR penalties in the form of higher RSF requirements on their asset books.

The transition to NSFR compliance is more challenging for smaller banks with limited access to a diverse range of funding sources. The RBI has historically acknowledged this and has built appropriate flexibility into the implementation framework. For enterprises banking with smaller institutions, this is a factor worth evaluating in your banking partner selection process.

The net stable funding ratio is one of the most consequential structural reforms to emerge from the post-2008 global regulatory overhaul. For Indian banks, RBI's implementation of NSFR effective October 2021 marked a decisive shift toward long-horizon funding discipline. For enterprises, it reshaped the institutional environment in which capital is priced, credit is extended, and market transactions are executed.

Understanding NSFR does not require a banking license. It requires recognizing that your capital markets journey does not happen in isolation from institutional liquidity frameworks. The banks structuring your pre-IPO debt, the underwriters pricing your listing, the market makers supporting post-listing liquidity: all operate under the structural constraints that NSFR defines.

If your enterprise is approaching a public listing and you want to ensure your capital structure is built to institutional standards, S45 supports promoters and leadership teams in preparing for public markets. Connect with S45 to begin the readiness conversation.

Discover more insights on similar topics