March 30, 202610 min read

Debt Capital Markets in India: Why Enterprises Should Care

By Aman Singh

Debt & Equity Financing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

If you have been running a high-growth enterprise in India for more than five years, you already know the problem. Banks want collateral you have not pledged. Venture capital wants equity you do not want to give. Private equity wants control you did not build your company to hand over.

And somewhere in the middle, between the capital you need now and the capital structure you want to defend in a DRHP two years from now, lies a gap that most advisors fill with vague recommendations and generic term sheets.

Revenue-based financing in India has emerged as one serious attempt to fill that gap. It is fast. It is non-dilutive. It is structurally flexible. But it is also widely misunderstood, especially at the mid-market level where the stakes of a wrong financing decision extend well beyond the current quarter.

This guide is written for founders, CFOs, and board members of Indian enterprises with revenue between Rs. 80 crore and Rs. 800 crore who are evaluating RBF not just as a working capital tool, but as a decision point in a larger capital markets journey. The mechanics matter. But so does the sequencing.

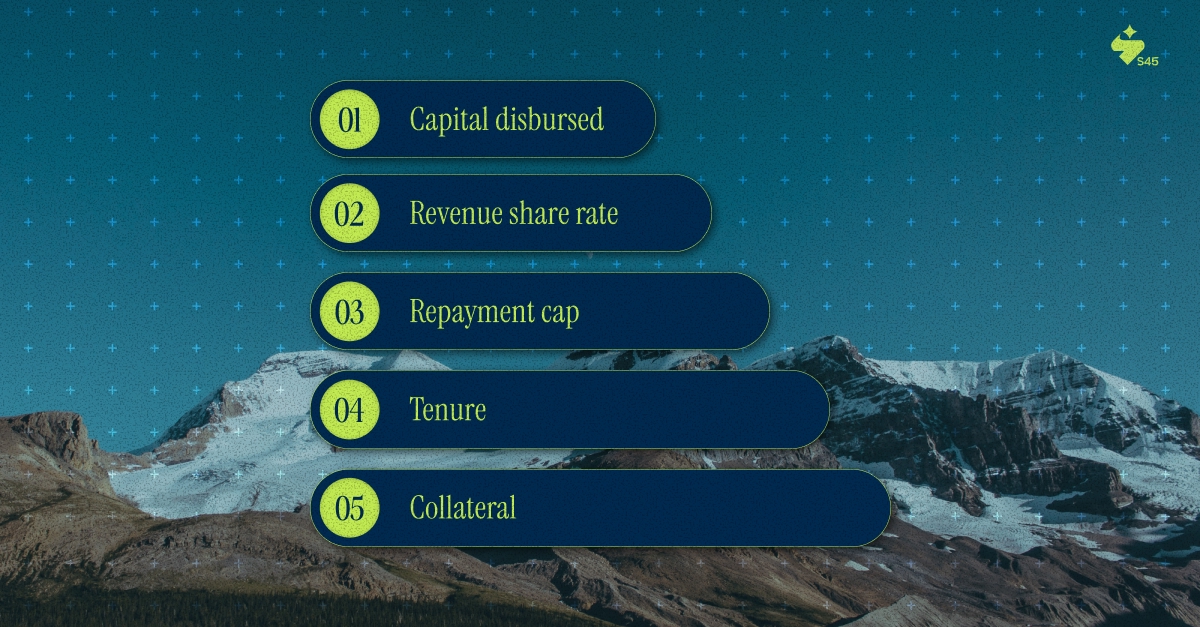

Revenue-based financing (RBF) is a capital instrument where an investor or lender provides a lump sum to a business in exchange for a defined percentage of future monthly revenues. The arrangement continues until the total repayment reaches a pre-agreed cap, typically expressed as a multiple of the disbursed principal.

Unlike a term loan, there is no fixed EMI. Unlike equity, there is no ownership transfer. The repayment adjusts to business performance, which is the instrument's core design principle.

Here is how a standard RBF structure works:

The practical result: in a strong revenue month, you repay more. In a lean month, you repay less. The lender's return is tied directly to your business performance.

Feature | Bank Loan | Venture Capital | Revenue-Based Financing |

Equity dilution | None | Significant | None |

Collateral required | Usually yes | No | Usually no |

Repayment structure | Fixed EMI | Exit event | % of monthly revenue |

Board interference | Minimal | Often present | None |

Approval speed | Weeks to months | Months | Days to weeks |

Best suited for | Asset-heavy businesses | High-growth, exit-focused | Revenue-generating, asset-light businesses |

This comparison matters because RBF is not universally superior, it is situationally superior. The decision to use it should be grounded in an honest assessment of your capital structure, not simply the speed of disbursement.

Must Read: Revenue-Based Financing for Startups: A Comprehensive Guide

India's credit architecture has historically been designed around two extremes: the collateral-backed loan, which favors asset-heavy businesses and legacy industries, and venture capital, which favors high-growth startups willing to trade equity for scale capital.

For the large segment of Indian mid-market enterprises, profitable, growing, asset-light, and founder-led, neither extreme fits cleanly.

The structural mismatch is not a failure of ambition. It is a failure of instrument design.

Revenue-based financing in India directly addresses this gap. It operates outside the collateral-driven banking framework and the equity-dilution framework of venture capital. For businesses with documented, recurring revenue, SaaS ARR, subscription cohorts, trade receivables, or repeat D2C sales, it provides a financing pathway calibrated to actual cash flow.

Not every business belongs in an RBF structure. The instrument is most effective when the following conditions are met:

Businesses that meet this profile include SaaS companies with stable ARR, D2C brands with established repeat purchase rates, subscription-first platforms, agencies with retainer-based revenue, and mid-market manufacturers with strong order books.

Speed is the primary marketing claim of most RBF providers in India. Founders are often told they can access capital in 48 to 72 hours. That is sometimes true. But speed without structural clarity is simply expensive capital with good branding.

Before executing an RBF agreement, a CFO or founder should run the following analysis.

RBF is priced not by an interest rate but by a revenue-share multiple. A capital advance of Rs. 2 crore with a repayment cap of Rs. 3 crore (1.5x) and a 6% monthly revenue share on a business generating Rs. 50 lakh per month will produce a repayment tenure of approximately 10 months.

The annualized cost of that capital depends entirely on how fast the business repays. A fast-growing business repays quickly, thereby compressing tenure and inflating annualized cost. Slower business stretches repayment periods, making the effective rate appear more moderate.

The practical implication: RBF is most cost-effective for businesses deploying capital in campaigns or initiatives with a defined, measurable return cycle. It is the least cost-effective as a substitute for long-term working capital or as a bridge instrument when the business has no clear path to revenue acceleration.

Before accepting an RBF term sheet, the following questions should be answered in writing:

These are not adversarial questions. They are institutional clarity questions, the kind that separate a well-structured capital decision from a working capital emergency resolved too quickly.

Also read: Is Your Business Facing a Funding Gap? Here’s What Every SME Should Know

Most conversations about RBF in India treat the instrument as entirely outside the regulatory perimeter. That is largely accurate for the capital deployment phase. But the picture becomes more complex for companies that are building toward a public market event.

This is where firms like S45 bring a dimension to the conversation that most RBF providers cannot. The question is not simply whether the instrument is legally permissible; it is whether the financing history you are building today will be defensible when SEBI, exchange due diligence teams, and institutional investors examine your books two or three years from now.

When a company files a DRHP, its complete financing history is disclosed and scrutinized. This includes:

RBF instruments, if structured as debt, appear in the borrowings schedule. If structured as revenue-sharing agreements with investors who receive revenue before it flows to equity holders, the instrument may raise classification questions depending on its specific terms.

This does not mean RBF is incompatible with an IPO pathway. It means the instrument must be structured with downstream disclosure requirements in mind. An RBF agreement executed without that lens can generate SEBI queries that delay a filing by three to six months, not because the instrument was illegal, but because the documentation was ambiguous.

Beyond disclosure, RBF usage signals something about business governance to institutional investors. A company that has relied on multiple rounds of RBF financing without building a long-term capital strategy raises a question: Is this a business being managed toward a milestone, or toward institutional credibility?

The answer to that question lies in the capital structure architecture, not in the choice of individual instruments.

Revenue-based financing in India makes the most sense as an early- to mid-stage instrument, a bridge between bootstrapped growth and the first formal institutional equity event. For founders eyeing a Main Board or SME Exchange listing, the financing decisions made in the Rs. 80–200 crore revenue window have disproportionate consequences for IPO readiness.

A typical high-growth Indian enterprise on the path to listing moves through broadly three capital stages:

Stage 1 (Rs. 20–80 crore revenue)

This is where RBF fits most naturally. The business has demonstrable revenue, the cap table is clean, and the founders need working capital or growth capital without diluting equity or taking on hard collateral debt. RBF addresses this cleanly.

Stage 2 (Rs. 80–300 crore revenue)

This is where capital structure decisions begin to have consequences for IPOs. Debt-to-equity ratios, related party exposures, and the governance infrastructure around financial reporting start to matter. RBF can still play a role here, but it should be used selectively and with full awareness of how it will be classified in financial statements and disclosed in due diligence.

Stage 3 (Rs. 300 crore+ revenue, 12–24 months pre-IPO)

This is where the capital structure needs to be stabilized, cleaned up, and made defensible. New RBF obligations introduced at this stage, particularly if they create revenue share arrangements that appear as off-balance-sheet commitments, are a risk, not a feature.

Before committing to any material financing decision in Stage 2 or Stage 3, an IPO Readiness Scan is the correct first step. This is not a vague audit process. It is a structured diagnostic that assesses capital structure defensibility, governance gaps, financial disclosure quality, and SEBI compliance posture, generating a clear picture of what is listing-ready and what needs to be addressed before mandate.

The scan is the instrument that tells you not just whether to use RBF, but whether your existing capital decisions, including any RBF agreements already in place, require restructuring before a DRHP can be filed without generating adverse commentary.

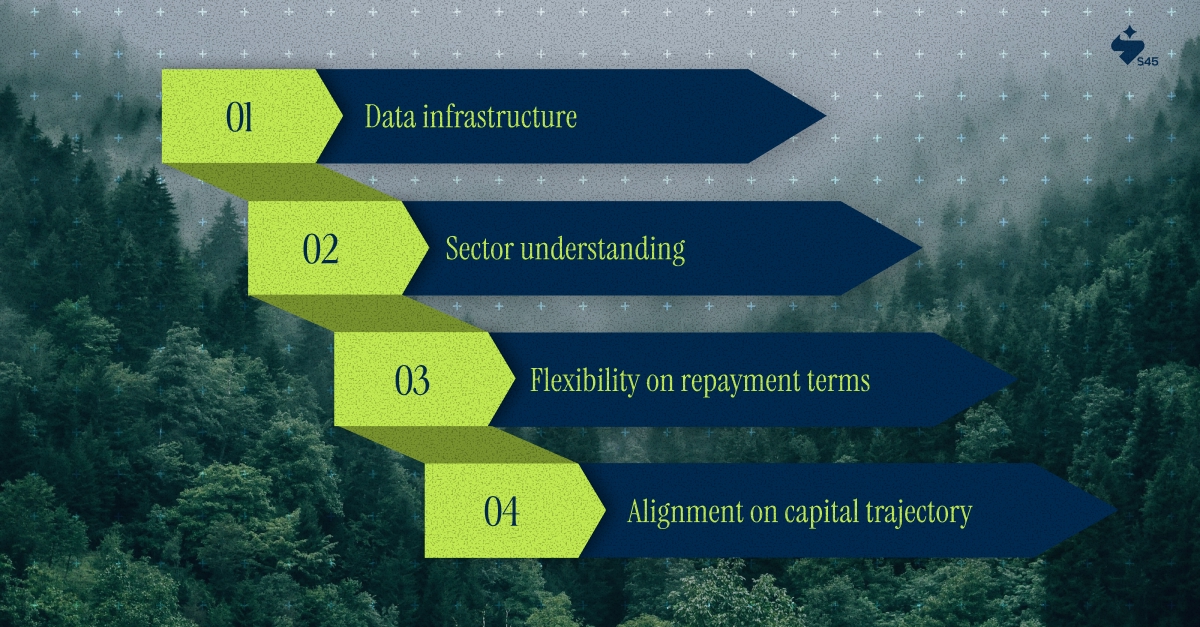

The revenue-based financing market in India has grown substantially since 2020, with platforms ranging from marketplace-based lenders to NBFC-backed providers. For a founder evaluating options, the choice of provider matters as much as the choice of instrument.

Revenue-based financing in India has earned its place as a legitimate capital instrument for growth-stage enterprises. It solves a real problem: fast, non-dilutive capital for businesses with documented revenue and specific deployment needs. When used at the right stage and structured correctly, it adds genuine operational leverage without compromising the cap table.

But the founders and CFOs reading this guide are not simply managing a working capital cycle. They are building enterprises with specific capital markets destinations, a Main Board listing, a strategic acquisition, and an institutional anchor round. For those enterprises, every financing decision is a building block in a structure that will be examined by SEBI, rated by credit agencies, and assessed by institutional investors with no tolerance for structural ambiguity.

Use RBF where it fits. But use it with full awareness of where it sits in your longer-term capital architecture.

If you are at a stage where those questions do not yet have clear answers, the right next step is a structured conversation, not a term sheet. Connect with S45 for an IPO Readiness Scan or a capital structure consultation before committing to your next financing round.

Discover more insights on similar topics