April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You have built a business generating INR 100–500 crore in revenue. Your balance sheet is clean. Your bankers are satisfied. And yet, the moment you start planning a public listing or a structured capital raise, you discover that your capital architecture has gaps nobody warned you about.

The most common gap is this: most Indian promoters and CFOs understand equity capital markets intuitively, IPOs, valuations, and dilution. But debt capital markets? That is where the conversation usually stalls. Not because the subject is complicated in theory, but because nobody maps out how the machine actually operates at the enterprise level in India.

This is the problem this blog addresses, not a primer for first-year analysts, but a clear operational map of how debt capital markets function in India, what instruments exist, who regulates them, and what a credible capital markets strategy looks like when debt and equity work in tandem.

Debt capital markets (DCM) are the markets through which governments, financial institutions, and corporations raise capital by issuing fixed-income instruments, such as bonds, debentures, commercial paper, and related securities. Investors lend capital and receive periodic interest payments, with principal returned at maturity. Unlike equity, the issuer does not dilute ownership.

In India, the DCM ecosystem comprises two broad segments:

Operated and regulated by the Reserve Bank of India (RBI), this segment includes G-Secs (central government bonds), State Development Loans (SDLs), and Treasury Bills. It forms the largest portion of India's total bond market. The RBI functions simultaneously as a monetary authority, debt manager, and market regulator for government securities.

Regulated by the Securities and Exchange Board of India (SEBI), this segment covers non-convertible debentures (NCDs), commercial paper, and other fixed-income instruments issued by corporates. The governing framework is the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021.

Together, India's bond market stood at approximately INR 226.3 trillion as of December 2024, a substantial increase from INR 140.8 trillion a decade earlier. Of that, corporate bonds account for roughly INR 51.58 trillion. The scale is significant. The depth, however, remains a work in progress.

Understanding how DCM operates is not optional for any enterprise planning a structured capital raise. Here is how the system works in practice.

The primary market is where new debt securities are issued. Corporate issuers in India typically access this market through one of two routes:

The trade-off is real: private placement conserves time and compliance burden, but produces securities that are lightly traded in the secondary market.

After issuance, bonds are traded on the debt segment of recognized exchanges (NSE, BSE). SEBI's Request for Quote (RFQ) platform has improved price discovery by enabling electronic, screen-based trading. However, trading volumes have remained largely stagnant even as the outstanding stock of corporate bonds has grown, suggesting a structural buy-and-hold culture among institutional investors that constrains genuine secondary-market liquidity.

Moving an enterprise toward these debt instruments requires a capital structure that can withstand institutional due diligence. S45 provides the execution framework to ensure these debt layers are structured correctly long before they reach the primary market.

Not every instrument suits every issuer. The choice depends on tenure requirements, cost of capital, investor appetite, and regulatory eligibility.

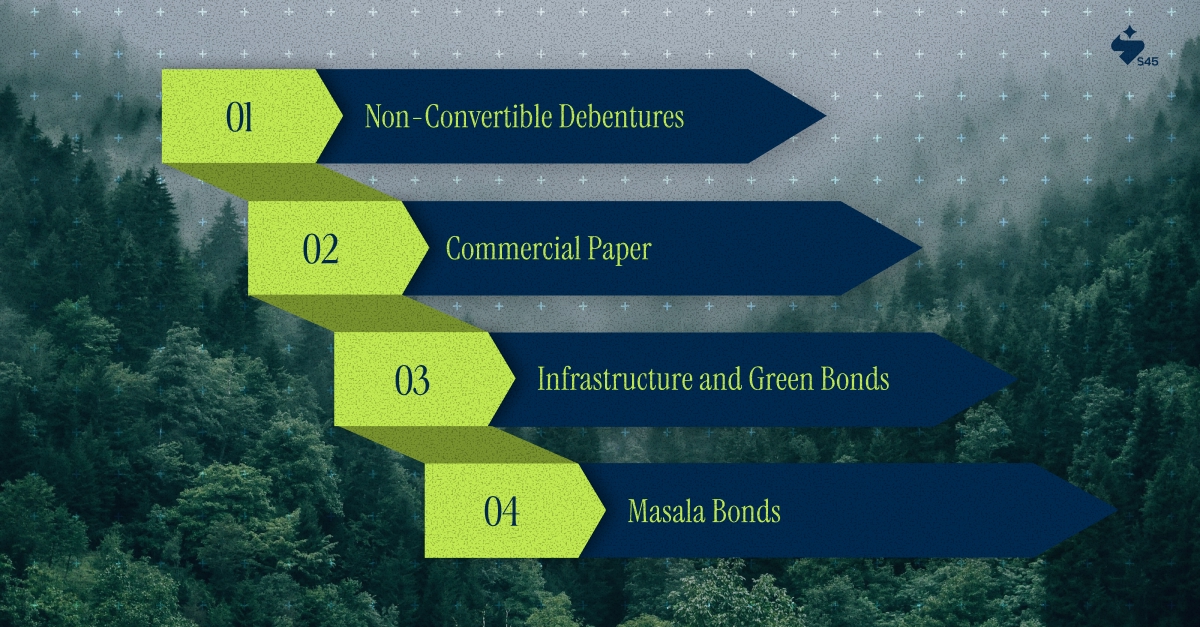

The most common corporate debt instrument in India. NCDs are fixed-tenure, fixed-income securities that cannot be converted into equity. They are used for capital expenditure financing, refinancing of existing debt, and working capital management. Listed NCDs must comply with SEBI NCS Regulations and maintain ongoing LODR obligations.

Short-term unsecured instruments with maturities between 7 days and 1 year. Primarily used by large, creditworthy corporates and NBFCs for working capital needs. CPs are issued at a discount and governed by RBI guidelines for issuance, with SEBI overseeing listing requirements.

Purpose-linked instruments structured for infrastructure financing or ESG-mandated projects. These carry potential advantages in investor appetite given the participation of development finance institutions (DFIs) and FPIs with ESG mandates.

INR-denominated bonds issued in overseas markets are governed by the RBI's External Commercial Borrowing (ECB) framework. They allow Indian issuers to access global capital while keeping the currency risk with foreign investors.

Indian debt capital markets operate under a dual regulatory structure. Getting this wrong at the planning stage is expensive.

The RBI operates India's government bond market as both monetary authority and debt manager. It conducts weekly debt auctions, sets monetary policy (which directly drives bond yields), and regulates primary dealers. Its Retail Direct Gilt (RDG) platform, launched in 2021, opened direct retail access to government securities. The RBI's rate cycle has direct downstream consequences for corporate bond pricing. When the RBI cuts rates, bond yields fall, reducing the cost of fresh corporate debt issuances.

SEBI is the primary regulator for the corporate bond market. Its interventions over the past decade have systematically expanded market access, reduced issuance costs, and improved transparency. Key SEBI reforms include reducing the minimum face value for privately placed corporate bonds from INR 10 lakh to INR 1 lakh (January 2023) and further to INR 10,000 (May 2024). These changes are documented under SEBI NCS Regulations, 2021, and subsequent circulars.

Any publicly issued corporate bond must be rated by a SEBI-registered Credit Rating Agency (CRA). India's rating profile is dominated by AAA and AA-rated issuances, which creates a structural challenge for mid-market companies. Without investment-grade ratings, access to the public corporate bond market is limited, and the private placement route becomes the primary option.

The honest assessment: Indian debt capital markets punch below their weight relative to the size of the economy. Understanding why matters for any enterprise that intends to use them strategically.

The tailwinds are real. Corporate bond mutual funds recorded net inflows of INR 11,983 crore in May 2025, more than three times the prior month's figure. RBI rate cuts have lowered the cost of fresh corporate debt. India's inclusion in the J.P. Morgan GBI-EM global government bond index has attracted fresh FPI interest into the broader fixed-income ecosystem.

SEBI's push on digital platforms, unified KYC, electronic bidding, and retail access through OBPPs is systematically broadening the investor base. For mid-market enterprises, this matters: the window for structured corporate debt issuances at favorable terms is genuinely widening.

This is the section most investment bankers skip, and it is the one that matters most for enterprise promoters planning a capital markets strategy.

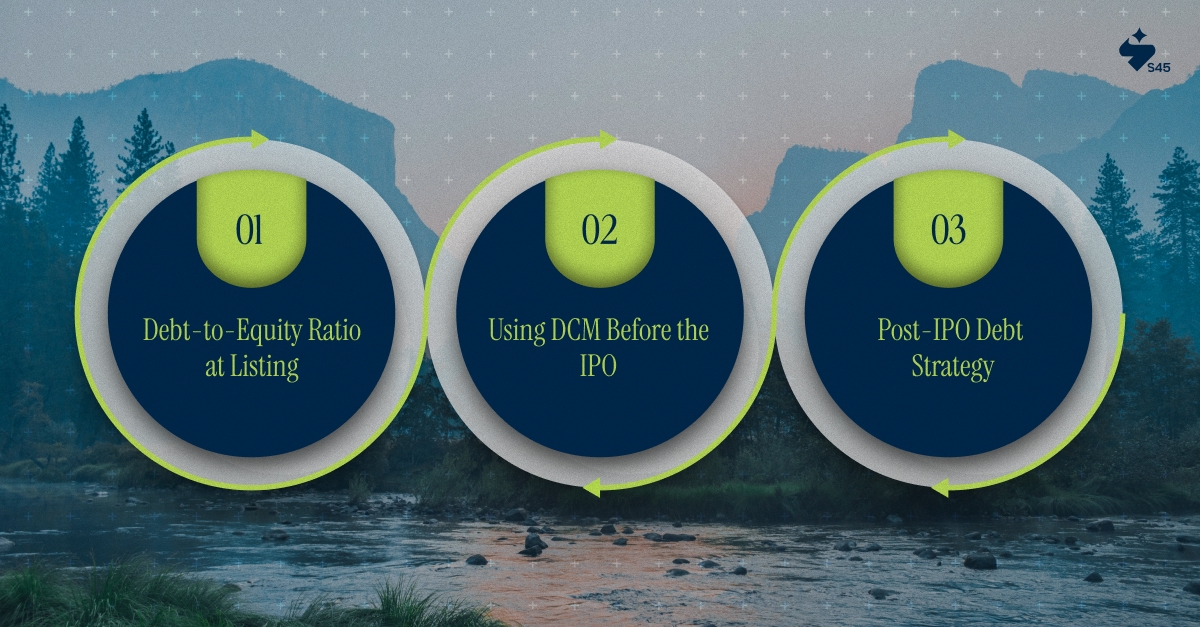

For a company targeting an IPO on the Main Board or SME Exchange, the capital structure entering the listing process directly shapes pricing, valuation, and post-listing obligations.

SEBI ICDR disclosures require a detailed presentation of capital structure, outstanding borrowings, and debt service obligations. Institutional investors, QIBs, and anchor investors scrutinise debt serviceability as part of the pricing logic. A company entering the IPO process with poorly structured corporate debt faces a valuation discount.

Some enterprises strategically access debt capital markets in the 12–24 months before an IPO to accomplish two things: (1) refinance high-cost bank debt with rated NCD issuances at lower coupon rates, improving the P&L presentation entering the listing; and (2) establish a credit rating track record that signals institutional creditworthiness to public market investors.

Listed companies are subject to SEBI's Listing Obligations and Disclosure Requirements (LODR) Regulations. Ongoing debt issuances after listing require continuous disclosures and credit agency reporting. Designing a post-IPO debt strategy is capital markets craftsmanship; it is not an afterthought. S45 works with enterprise promoters precisely at this intersection: building institutional clarity around the capital structure before the DRHP is filed, so that nothing in the debt schedule becomes a SEBI comment.

One of the consistent failure modes in Indian capital markets is the gap between what a promoter believes about their debt position and what an institutional investor or SEBI reviewer needs to see documented.

When a company issues NCDs publicly, the offer document must contain:

This is not a checklist exercise. It is an evidence architecture. Every disclosure must be traceable to a source document. Every number must show its math. This is what separates institutional-grade capital markets execution from the fragmented, advisor-led process that stalls at SEBI review.

Debt capital markets in India are no longer a secondary consideration for high-growth enterprises. They are an active tool for managing capital structure, reducing borrowing costs, establishing creditworthiness, and preparing the balance sheet for a public listing.

The regulatory architecture is more functional than ever. SEBI and RBI have made consistent structural improvements. The investor base is broadening. The rate environment has turned favorable. What remains in short supply is institutional clarity at the enterprise level — the ability to read the debt market, structure an issuance correctly, and embed that work into a coherent capital markets strategy rather than treating it as a compliance exercise.

For promoters and CFOs building toward a public listing, the starting point is not the bond market; it is the balance sheet. Get the capital structure right before the DRHP. Know what your debt profile signals to institutional investors. Ensure every number in your offer documents can be defended.

If you are assessing your capital markets readiness, whether for a structured debt issuance, an IPO, or both, connect with S45 for a focused IPO Readiness Scan. Before you commit months and reputation, get institutional clarity.

Discover more insights on similar topics