April 10, 202611 min read

Angel vs. Seed Funding: What Every Indian Founder Must Know Before Raising Capital

By Abhishek Bhanushali

Startup Funding

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

In 2022, you closed a complex funding round fast. Lawyers called it structured debt with equity participation. Auditors signed off. Tax advisors approved the treatment. The round closed, growth continued, and the paperwork went into a drawer.

Now you’re 90 days from your DRHP filing. SEBI’s first comment questions the conversion pricing and whether it triggers preferential allotment disclosure. Suddenly, what felt like smart structuring becomes compliance archaeology. The rationale lives in scattered emails. The valuation support was never formalized. Board minutes don’t tell the full story.

This is a common pattern in mid-market Indian companies heading toward IPO. Private credit and hybrid instruments address growth capital constraints, but they rarely fit into clear regulatory categories. What creates flexibility in fundraising can create friction at listing.

Solve the documentation 18 months before the mandate, and timelines stay tight. Solve it 90 days before filing, and your 45-day plan becomes a six-month delay.

The difference between private credit and bank lending barely matters when you’re raising capital. It matters a lot when you’re drafting your DRHP. Fundraising rewards flexibility. IPO prep demands defensibility. That’s why capital structure surprises surface 24–36 months later.

Banks follow RBI exposure and end-use norms. AIF-structured private credit funds operate under a different framework and can finance acquisitions, land, or shareholder refinancings. Helpful with fundraising. Messy at disclosure.

PE buys equity and exits on appreciation. Private credit uses debt or hybrid securities with coupon and maturity features. Control remains unchanged, but the capital stack becomes more complex.

In India's market context, private equity credit funds function as non-bank lenders providing:

The investor base differs from banks. These funds deploy capital from pension funds, insurance companies, family offices, and high-net-worth individuals seeking 12-24% IRRs rather than 8-10% bank lending spreads.

The structure creates flexibility for borrowers but documentation complexity for pre-IPO disclosure. AI-native investment banks like S45 address this by treating capital structure mapping as the first step in IPO readiness, not an afterthought during DRHP drafting.

Market shifts in lending don’t happen by accident. India’s private credit expansion is driven more by regulatory pressure on traditional lenders than by innovation. That’s why many capital stacks today look very different from five years ago.

India’s private credit market has grown from roughly USD 500–600 million annually in 2012 to nearly USD 10 billion in 2024. This is a structural shift, not a trend cycle.

Why banks pulled back

After the 2018 NBFC crisis and COVID disruptions:

For mid-market companies doing M&A or pre-IPO restructuring, this created funding gaps. Private credit funds stepped in.

What this means for pre-IPO companies

If you raised capital in 2023–2024, part of it likely came from private credit, especially in:

At the PO stage, the source doesn’t matter. The disclosure standard does.

You’ll need:

Whether funds came from a bank or an alternative credit fund, SEBI expects the same institutional-grade documentation.

Beyond understanding the market context, founders need precision about which instruments create specific disclosure challenges. Not all private equity lending structures are equally complex during DRHP preparation.

The term private equity lending encompasses multiple instrument types, each with different disclosure implications:

Backed by company assets with priority in repayment hierarchy. Appears straightforward until SEBI comments ask for collateral valuation methodology, charge registration timelines, and inter-creditor agreement disclosures. If collateral includes intellectual property, brand value, or future receivables, valuation becomes subjective, which invites extended comment cycles.

Sits between senior debt and equity in the capital structure. Often includes equity warrants, conversion rights, or PIK (payment-in-kind) features, in which interest accrues rather than being paid in cash. During DRHP drafting, this requires explaining why the instrument is classified as debt or equity, how conversion pricing works, and the dilution scenarios that may arise post-listing.

Debt instruments with attached equity warrants, profit participation rights, or conversion features. These hybrids require dual disclosure: debt service obligations and potential equity dilution. If conversion pricing was set using 2022 pre-money valuations and your IPO values the company at 3x that level, the delta becomes material.

CCDs (Compulsorily Convertible Debentures), CCPs (Compulsorily Convertible Preference Shares), and OCDs (Optionally Convertible Debentures) each have different accounting treatment, tax implications, and disclosure requirements. The key question: can you reconstruct the conversion logic that made sense at issuance and defend it during institutional scrutiny?

The timeline compression that separates 45-day DRHP execution from 6-month remediation cycles comes down to one factor: whether compliance discipline existed during fundraising or gets built retrospectively during IPO prep.

Firms like S45, which pair AI-driven DRHP systems with sector-specific banking experience, can accelerate disclosure assembly, but only if source documentation is available. Technology compresses workflow around evidence. It cannot manufacture evidence that was never created.

What SEBI ICDR and LODR Require from Day 1: Every debt instrument, every equity round, every related party transaction needs:

This is not "best practice." This is a baseline institutional expectation. Companies that maintain this discipline during fundraising treat SEBI comments as routine verification. Companies that reconstruct compliance post-facto spend 90-120 days in remediation cycles.

The Role of Private Equity Credit Funds in Pre-IPO Restructuring: Some companies use private equity credit funds strategically before IPO:

This works only if restructuring occurs 18-24 months before listing: enough time for the new capital structure to establish a track record and for financial statements to reflect the updated arrangements across full fiscal years.

For companies targeting SME Exchange listings, capital structure carries additional implications:

SME listings require market makers for liquidity. Market makers analyze debt service obligations, promoter pledge status, and capital structure complexity to assess risk. Heavy debt loads or complex hybrid instruments reduce market makers' appetite, thereby affecting listing liquidity and price discovery.

Many private equity credit funds include financial covenants, such as minimum EBITDA coverage ratios, maximum leverage limits, and restrictions on additional borrowing. Post-listing, these covenants continue. If your listed entity violates debt covenants due to market volatility impacting earnings, it creates disclosure obligations and potential technical defaults that damage institutional credibility.

If existing debt facilities are secured by promoter equity pledges, listing creates complexity:

These elements require advance planning, not crisis management during book-building.

Capital structure decisions made during the growth phase determine more than ownership percentages. They establish the disclosure complexity, covenant constraints, and refinancing obligations that either accelerate or delay your path to public markets.

The strategic question facing mid-market Indian promoters preparing for public markets:

Using private equity lending to fund growth preserves equity ownership but creates:

Bringing in private equity creates:

Mezzanine debt, convertible instruments, and structured credit occupy the middle ground:

For companies in the ₹80-800 Cr revenue range preparing for Main Board listing, the answer is rarely binary. It's about sequencing. What capital structure positions you best for institutional scrutiny while preserving the flexibility to execute your growth plan?

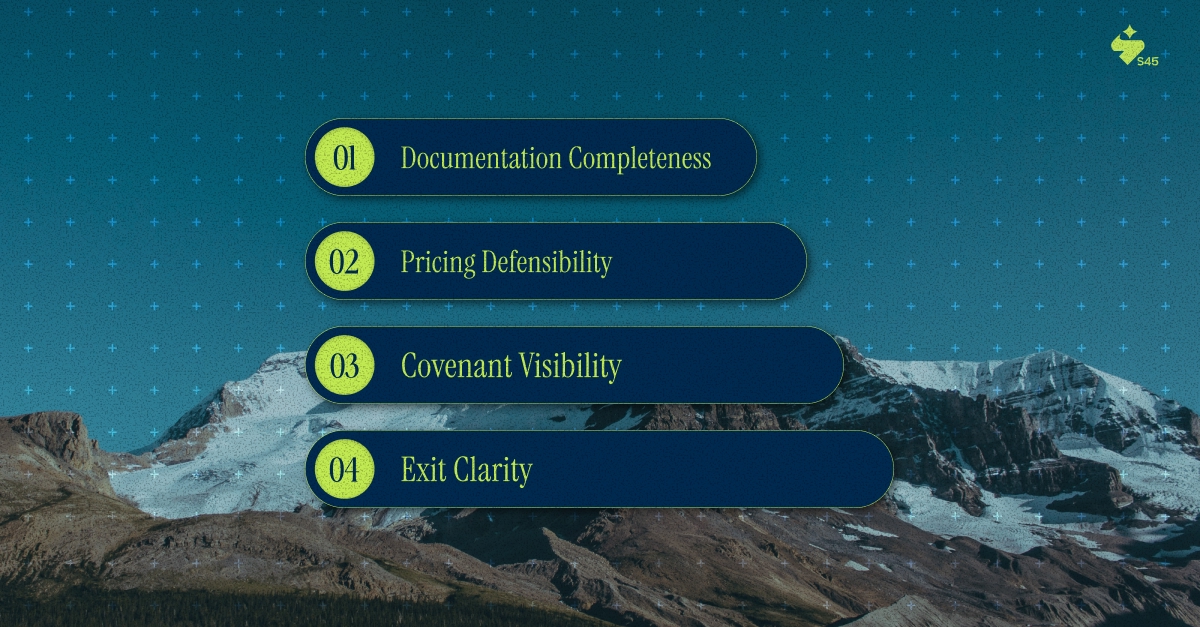

Abstract discussions about optimal capital structure matter less than concrete evaluation of documentation completeness and disclosure defensibility. The readiness assessment framework used by institutional bankers focuses on four elements:

Can you produce every subscription agreement, board resolution, valuation report, and compliance certificate for every equity and debt issuance in the last 5 years? If the answer is no, you're not ready to draft the DRHP. You're ready for compliance archaeology that adds 60-90 days to the timeline.

Can you explain why equity was priced at ₹100/share in 2022, ₹150/share in 2023, and you're now targeting an IPO valuation of ₹400/share? The delta needs an evidence-based narrative. Revenue growth, margin expansion, market position change, comparable transactions. Opinion without evidence fails SEBI scrutiny.

Do you have real-time tracking of all debt covenants across all facilities? Not just current compliance status, but forward-looking triggers and cross-default linkages. If SEBI asks, "What happens to your debt covenants if IPO pricing comes at the bottom of the price band," can you answer with precision?

For every debt facility and structured instrument, what's the exit plan?

Ambiguity on any of these creates disclosure gaps that surface during SEBI review.

The companies that successfully navigate private equity credit funds before IPOs share a common approach. They treat every capital raise as IPO preparation, not just growth funding.

This Means:

The discipline required here isn't about perfection. It's about institutional preparation. Companies that maintain clean documentation trails during fundraising compress IPO timelines by responding to SEBI comments with evidence, not narrative reconstruction.

Macro trends in private credit deployment reveal more about banking constraints than market opportunity. The growth numbers matter less than understanding what created the gap.

The 53% surge in private credit deployment in H1 2025 is not about market euphoria. It's about banks retreating from mid-market complexity while capital needs remain.

For companies in the ₹80-800 Cr revenue range, this creates:

If you're accessing the capital, you're not taking shortcuts: you're choosing instruments appropriate for a mid-market scale. The question is whether you're documenting these decisions with the precision required for eventual public market transition.

Private equity credit isn’t complex because of its structure. It’s complex because every capital decision at each growth stage eventually surfaces in your DRHP.

Hybrid instruments, convertibles, and covenant triggers are none of these issues on their own. The issue is whether the documentation and rationale are of institutional quality. When they are, scrutiny moves faster. When they aren’t, IPO timelines stretch.

Companies that compress timelines treat SEBI ICDR and LODR as standards, not obstacles. Evidence over explanations. Documentation over memory.

If public markets are 18–24 months away, the readiness checkpoint is now. S45 begins with an evidence-based capital structure assessment because IPO speed is earned years before filing.

To understand where your structure stands, evaluate it the way S45 would. Clarity first. Mandate later.

Discover more insights on similar topics