March 26, 20269 min read

What Is Institutional Funding and Why Does It Decide Your IPO's Fate in India?

By Abhishek Bhanushali

IPO

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You have spent years building a business. You have crossed meaningful revenue milestones, built a leadership team, and begun thinking seriously about a public listing. Then someone puts a valuation figure on your company for the first time in a formal document, and the cracks appear.

The problem is rarely the business itself. The problem is the gap between how your company was valued as a private enterprise and how it will need to be valued in front of institutional investors, SEBI reviewers, and the public markets.

If your last private round was priced at a growth premium that does not hold up under public scrutiny, your DRHP will be questioned. If your pre-IPO alternative investment rounds were priced using methodologies inconsistent with ICDR norms, your pricing narrative will collapse before book-building even begins.

This is not a financial modeling problem. It is an execution and institutional readiness problem.

The valuation of alternative investments, private equity, structured debt, pre-IPO capital, and AIF-backed growth rounds sits at the centre of this challenge. Get it right, and your price band is defensible. Get it wrong, and you either reprice downward at listing or stall entirely.

Most founders treat their private funding rounds as internal milestones. The valuation assigned by a VC, family office, or AIF is understood to be a negotiated number tied to growth expectations and risk appetite, not a public declaration of intrinsic worth.

That assumption breaks the moment you file for an IPO.

SEBI's ICDR Regulations require that your DRHP disclose the basis of your IPO price band, including a comparison against your last private valuation. If your alternative investment rounds were priced using methods that do not align with publicly accepted valuation frameworks, you will face comments from SEBI asking you to justify the gap.

In June 2023, SEBI issued a circular mandating a standardized approach to the valuation of investment portfolios of Alternative Investment Funds. The circular endorsed the IPEV (International Private Equity and Venture Capital) Guidelines, adapted for the Indian context by IVCA as Country Partner. This was not a suggestion. It was a structural change in how private capital in India is expected to be valued and disclosed.

What this creates for IPO-bound companies is what can only be called a chaos gap. On one side, you have private rounds valued at levels below internal assumptions. On the other hand, you have SEBI reviewers and institutional investors demanding evidence-linked, methodology-consistent valuations. Between them sits a stack of spreadsheets, third-party reports of varying quality, and advisors who do not talk to each other.

This is the operational gap where Indian IPOs lose months and credibility. Founders do not fail because their businesses are weak. They fail because the evidence architecture around their valuation story is fragmented.

S45, India's AI-native investment bank, is built to close exactly this gap. The firm's IPO Readiness Scan identifies valuation inconsistencies before they surface in SEBI comments, mapping your private capital history against the disclosure requirements of a public listing, and building an evidence-linked valuation narrative that holds up under scrutiny.

Suggested Read: Characteristics of Alternative Investments: A Quick Guide

Understanding the valuation of alternative investments is not about knowing the formulas. Every institutional investor and SEBI reviewer already knows the formulas. What matters is knowing which method is appropriate for your business stage, your sector, and your IPO narrative, and why.

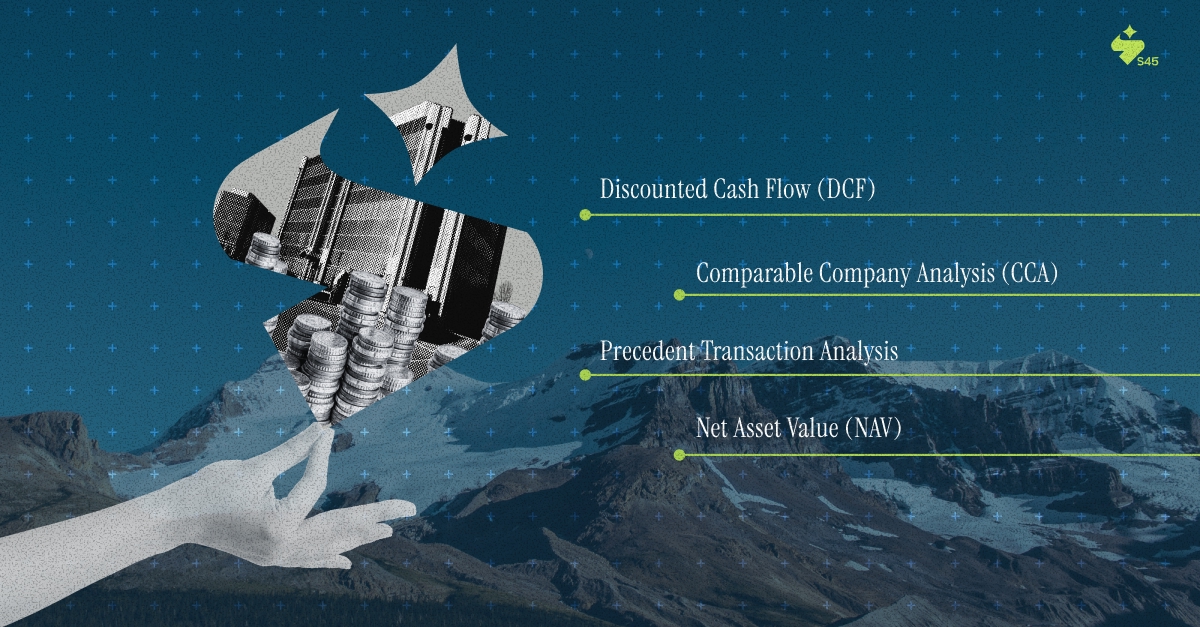

DCF values a company by projecting future free cash flows over a defined period and discounting them to present value using a risk-adjusted rate. It is theoretically the most rigorous method and is widely accepted under Indian Income Tax regulations for share transfers and ESOP valuations.

CCA values your business by applying valuation multiples derived from publicly listed peer companies. The most common multiples used in Indian capital markets are EV/EBITDA, EV/Revenue, and Price-to-Earnings.

This method derives valuation from historical M&A transactions and private investment rounds in similar businesses. It reflects what actual buyers paid, including any control premiums.

NAV values a company by subtracting total liabilities from total assets. It is most appropriate for asset-heavy businesses or investment holding structures.

The valuation of alternative investments in an IPO context is not about finding the highest number you can defend. It is about building a chain of evidence from your earliest private round to your proposed price band that no SEBI comment can break.

Every valuation claim in your DRHP must be traceable. This includes:

This is not bureaucratic compliance. It is the institutional architecture that allows QIB investors to underwrite your issue with conviction.

Sophisticated valuation practice for IPO-bound companies does not rely on a single method. The standard institutional approach triangulates across DCF, comparables, and precedent transactions to arrive at a defensible range. The goal is not a single number, it is a range with a clear centre of gravity that you can defend in front of bankers, investors, and regulators.

The SEBI ICDR Regulations require that your offer document explain in detail the basis for the issue price. Vague references to "market conditions" or "growth potential" will generate comments. Specific, method-referenced, evidence-linked explanations will not.

There is a pattern visible across Indian IPO timelines. Founders who treat valuation alignment as a pre-DRHP problem, something to sort out in the last 60 days before filing, consistently face one of three outcomes:

The cost of this is not just financial. It is reputational. Institutional investors track how a company navigates the IPO process. A messy DRHP history, visible in public SEBI records, signals weak governance and weak advisor quality.

Getting the valuation of alternative investments right before you begin IPO prep means:

This work cannot begin at the DRHP stage. It must begin at the readiness stage, ideally 12 to 18 months before you expect to file.

Traditional IPO preparation treats valuation analysis and DRHP drafting as sequential steps. The valuation work is done first, often by one advisor. The DRHP is written later, often by another. The result is a document where the pricing section does not fully align with the disclosure section, generating preventable SEBI comments.

The AI-driven approach compresses this timeline by running valuation analysis and disclosure drafting in parallel. Comparable company data is pulled and filtered systematically. DCF assumptions are stress-tested against sector benchmarks automatically. Disclosure language is drafted in line with SEBI ICDR requirements from day one, not retrofitted after the fact.

S45's AI-native DRHP drafting infrastructure reduces the mandate-to-DRHP timeline from a conventional four to six months to 30 to 45 days. This is not a claim about speed alone. It is a claim about precision, AI-assisted workflows reduce the number of internal review cycles, reduce the probability of methodology inconsistencies between sections, and allow banker judgment to be applied at the highest-value decision points rather than on data assembly.

Critically, AI does not replace the sector banker who has sat across SEBI comments, defended pricing logic under pressure, and cleaned up founder-led valuation narratives. It amplifies that judgment by removing the manual work that consumes the conventional IPO preparation timeline.

Must read: Best Alternative Investment Options in India 2025

The valuation of alternative investments does not end at the IPO price band. It continues into post-listing liquidity design, particularly for SME Exchange listings where trading volumes are structurally thin.

Founders preparing for SME listings often treat post-listing liquidity as someone else's problem. It is not. If your IPO price band is set too aggressively relative to secondary market absorption capacity, you will see immediate post-listing price deterioration that damages both your reputation and your ability to raise capital through the listed entity in the future.

Pricing discipline means calibrating your issue price not just to what the market will subscribe at, but to what the secondary market can sustain after listing. This requires sector knowledge, comparable trading data, and a pricing model built around your specific shareholder mix and lock-in structure.

This is the kind of liquidity and pricing design work that is embedded in execution-grade IPO preparation, not added as an afterthought on the day of book-building.

The valuation of alternative investments is not a number you arrive at before an IPO. It is a narrative you build over years of capital raising that must hold up under SEBI scrutiny, institutional investor analysis, and public-market pricing logic all at once.

Founders who treat this as a documentation exercise will face delays, repricing, or worse. Founders who treat it as an institutional discipline, building evidence-linked, methodology-consistent valuation records from their earliest private rounds through to their price band, arrive at their listing with capital market credibility intact.

The work required is operational, not theoretical. It demands banker judgment, regulatory precision, and the ability to compress timelines without compromising evidence quality.

If you are at the stage where IPO readiness is on the table, the right first step is not to begin drafting. It is to assess where your valuation history stands today, and what work is required to make it defensible tomorrow.

Connect with S45 for an IPO Readiness Scan that maps your private capital history against public market disclosure requirements before you commit months and reputation to a process that breaks on valuation.

Discover more insights on similar topics