April 1, 202612 min read

Traditional vs Alternative Investments: What You Need to Know Before Going Public

By Aman Singh

Investopedia

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Most founders approaching capital markets for the first time have a vague sense of what they need: "someone who understands finance and can get this done." That vagueness is expensive.

The confusion typically starts with terminology. Asset management and investment banking sound interchangeable to someone outside the financial system. They are not. They serve different clients, execute different mandates, operate on different sides of the market, and require entirely different standards of execution.

For a promoter running a ₹200 Cr enterprise and evaluating a Main Board or SME Exchange listing, this distinction is not academic. It determines who you hire, what you pay, what you get, and whether your IPO prep collapses in month four because the wrong firm was brought in for the wrong job.

The difference between investment banking and investment management becomes especially sharp in the Indian capital markets context, where regulatory precision, SEBI compliance, and execution timelines leave little room for misaligned advisory.

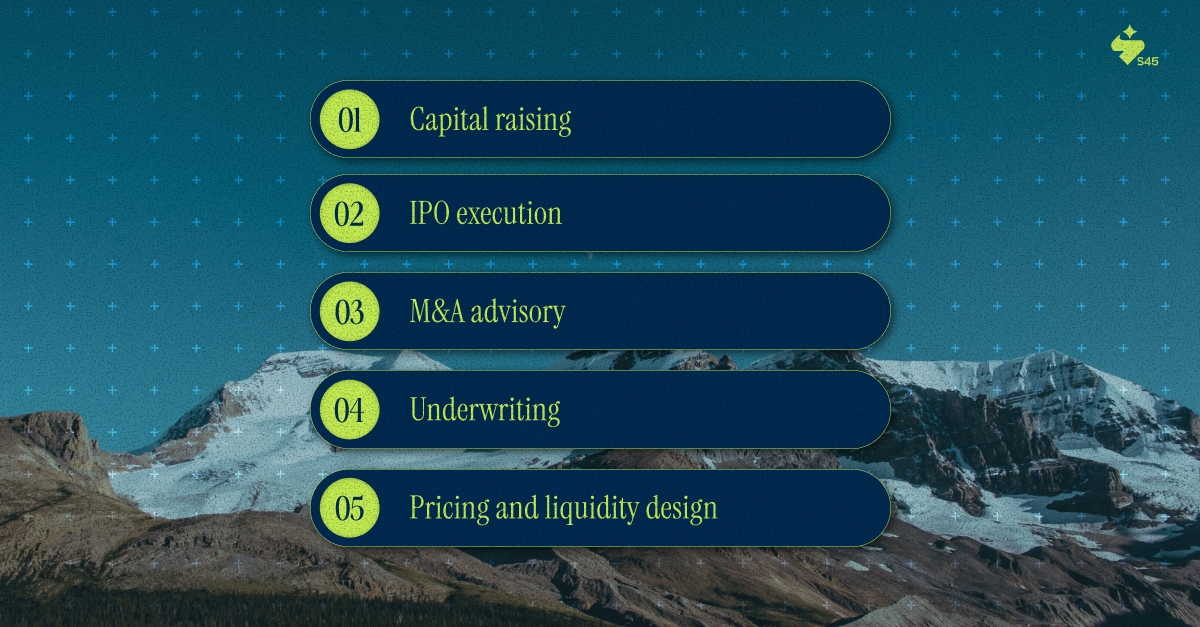

Investment banking sits on the sell side of capital markets. The mandate is transactional: help clients raise capital, structure and execute deals, and navigate the mechanisms through which money moves between companies and the market.

In the Indian context, this means deep familiarity with SEBI's ICDR (Issue of Capital and Disclosure Requirements) regulations, LODR (Listing Obligations and Disclosure Requirements), and the specific documentation standards that govern both Main Board and SME Exchange listings.

Investment banking is not advisory in the abstract. It is execution. Every deliverable has a regulatory deadline, a pricing implication, or a SEBI comment attached.

Asset management, also known as investment management, is on the buy side. The mandate is ongoing: to grow and protect clients' wealth over time by making informed investment decisions across asset classes.

Asset management clients are typically institutional investors (pension funds, endowments, and sovereign wealth funds), high-net-worth individuals, or retail investors accessing pooled vehicles such as mutual funds. The relationship is long-term, ongoing, and performance-benchmarked.

Asset managers do not file DRHPs. They do not sit across SEBI in a comments discussion. They do not design IPO pricing bands or manage book-building timelines.

Understanding the difference between investment banking and investment management comes down to a few structural realities:

Dimension | Investment Banking | Asset Management |

Market Side | Sell-side | Buy-side |

Core Activity | Transactions and capital raising | Portfolio management and wealth growth |

Client Type | Corporations, governments, promoters | Institutional investors, HNIs, retail |

Revenue Model | Deal fees, underwriting fees | Management fees, performance fees |

Time Horizon | Transaction-specific | Long-term, ongoing |

India Regulatory Frame | SEBI ICDR, LODR, Stock Exchange rules | SEBI (Mutual Funds), AMFI, PMS regulations |

IPO Relevance | Direct and central | Indirect (as a potential investor, not advisor) |

The confusion persists because large financial conglomerates often house both divisions under one brand. A bank like HDFC or Kotak may operate an investment banking division and an asset management arm. But inside those institutions, the teams, mandates, processes, and regulatory frameworks are entirely separate.

For an Indian promoter in IPO prep, conflating the two means you may be consulting a portfolio manager when you need a capital markets banker. The consequences show up in your DRHP quality, your pricing rationale, and your SEBI response timeline.

Platforms like S45 are increasingly helping founders and CFOs navigate this distinction early by aligning them with the right advisory workflows and capital-market readiness benchmarks before formal engagement with bankers.

India's IPO market has been running at a significant volume. The distinction between investment banking and investment management becomes operationally critical in this context for three specific reasons.

SEBI's ICDR regulations impose strict documentation, disclosure, and timeline requirements on IPO filings. This is investment banking territory, not asset management. Every number in your DRHP must be traceable. Every disclosure must link to a verifiable source. Every risk factor must be drafted with regulatory defensibility in mind.

An asset manager can analyze whether your company is a good investment. An investment banker is responsible for proving it to the regulator and to the market simultaneously, with legal accountability attached.

IPO pricing in India involves setting a price band, managing the book-building process, and calibrating the offer price against signals from institutional and retail demand. This is a transaction-specific, execution-intensive activity. Asset managers consume IPO pricing decisions; investment bankers design them.

For SME Exchange listings in particular, where liquidity design post-listing is a genuine concern, pricing strategy requires investment banking expertise that understands both the market microstructure and the SEBI framework for SME listings.

One of the most common reasons Indian IPOs stall is not a bad business or a weak market. It is a workflow breakdown. The wrong advisors, unclear accountability, and fragmented processes create documentation delays that compound into regulatory setbacks.

Firms like S45 are built specifically to address this. The model pairs sector-experienced investment bankers with proprietary AI systems to compress the mandate-to-DRHP timeline from the traditional four to six months down to 30 to 45 days. That compression is only possible when the function is correctly identified from the start: this is investment banking work, not financial advisory in the general sense.

There is one area where the functions genuinely overlap in relevance for Indian promoters: the post-listing phase.

Once your company is listed, it becomes an investable asset. Asset managers, mutual funds, and institutional investors begin evaluating it as a portfolio holding. Your investor relations strategy, disclosure quality, and financial reporting cadence all affect whether institutional money flows into your stock.

This is where compliance craftsmanship during the IPO phase pays dividends. A DRHP built with the rigor of an investment banking operation, with evidence-linked disclosures and clean financial documentation, reduces the friction between your listing event and institutional adoption.

The quality of investment banking execution upstream directly influences the quality of asset management interest downstream. They are sequential, not interchangeable.

If you are a promoter or CFO of an enterprise in the ₹80 to ₹800 Cr revenue range, evaluating a listing, here is the operational framing:

You need investment banking if:

You need asset management if:

These are not competing choices. They address different problems. For capital markets readiness, investment banking is the function. Knowing this before you spend six months with the wrong advisor is the difference between institutional clarity and expensive confusion.

The difference between investment banking and investment management is not a technicality. It is a structural distinction that determines execution quality, regulatory outcome, and the credibility of your listing.

Investment banking is about transactions, access to capital, and market-facing execution. Asset management is about portfolio construction, wealth protection, and long-term performance. In Indian capital markets, where SEBI's framework is rigorous and the margin for advisory misalignment is narrow, understanding this distinction is the starting point for serious IPO preparation.

Founders who walk into the IPO process with institutional clarity about who does what, and why, do not spend months rebuilding from avoidable errors. They execute.

Connect with S45 to evaluate your IPO readiness and understand whether your enterprise is truly positioned for a successful listing.

Discover more insights on similar topics