April 1, 202612 min read

Traditional vs Alternative Investments: What You Need to Know Before Going Public

By Aman Singh

Investopedia

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

If you've raised institutional capital, you already know the spreadsheet doesn't tell the full story.

Your company secretary maintains one set of books. Your CFO tracks another. Your PE investor demands quarterly reports that reconcile neither. By the time SEBI asks for evidence-linked disclosures on capital allocation, you're reconstructing transactions from three years ago whilst your merchant banker waits.

This isn't a documentation problem. It's an accounting architecture problem.

Most Indian promoters preparing for IPO discover, too late, that corporate accounting and fund accounting operate on fundamentally different principles. Corporate books track business performance: revenue, expenses, and assets. Fund accounting tracks capital: who owns what, how profits are split, what preferential rights exist, and how exits cascade.

According to KPMG India, 80 mainboard IPOs in FY25 raised ₹1,630 billion, with institutional participation driving valuations. Yet the majority of DRHP delays stem not from business fundamentals but from incomplete reconciliation between corporate financials and investor-level capital structures.

The chaos compounds when companies discover that fund accounting in investment banking isn't just a back-office function; it's the foundation of regulatory compliance, investor confidence, and pricing defensibility.

Fund accounting in investment banking governs how pooled investment capital is tracked, valued, and reported across stakeholders with different rights and return structures. Unlike corporate accounting, it manages capital allocation, valuation, and distribution waterfalls.

In India, it becomes critical when PE or VC investors hold preferential rights, multiple funding rounds create layered share classes, founder dilution must be tracked, and SEBI requires evidence of fund deployment, valuation, and allocation.

Fund accounting sits at the intersection of investment management and regulatory compliance. For IPO-bound companies, institutional investors, and SEBI, reconciliation across corporate financials, fund-level reporting, and cap table reality is required. This is not cosmetic; companies that listed during India’s 2024 IPO cycle had resolved fund accounting well in advance.

S45 bridges fund accounting and IPO readiness through execution ownership. For companies with institutional capital or complex cap tables, S45 surfaces risks early, allocation gaps, unreconciled preferential rights, missing deployment evidence, and NAV-to-book mismatches, before they become SEBI issues.

Sector bankers, supported by proprietary AI, cross-reference financials, agreements, and fund reports to embed evidence directly into DRHP disclosures. By integrating reconciliation into the core workflow, S45 compresses mandate-to-DRHP timelines to 30–45 days by removing friction, not work.

Indian capital markets operate at high velocity. According to data from IPO Platform, 243 SME IPOs were listed in 2024, up from 179 in 2023, a 35.8% year-on-year surge. Main Board IPOs raised over ₹1.63 lakh crore in FY25.

But velocity creates fragility.

Most mid-market Indian companies that raise PE/VC funding operate under fragmented accounting architectures:

The gap widens when:

By the time IPO preparation begins, the company faces dual obligations:

Companies that haven't maintained parallel fund accounting visibility spend months reconstructing transactions. This delays DRHP submission. Worse, it invites SEBI queries that could have been preempted with proper reconciliation.

Understanding fund accounting in investment banking means recognising that institutional investors think in terms of NAV, IRR, and MOIC (Multiple on Invested Capital). Promoters think in terms of revenue growth and EBITDA margins. SEBI demands that both perspectives be reconciled in the DRHP.

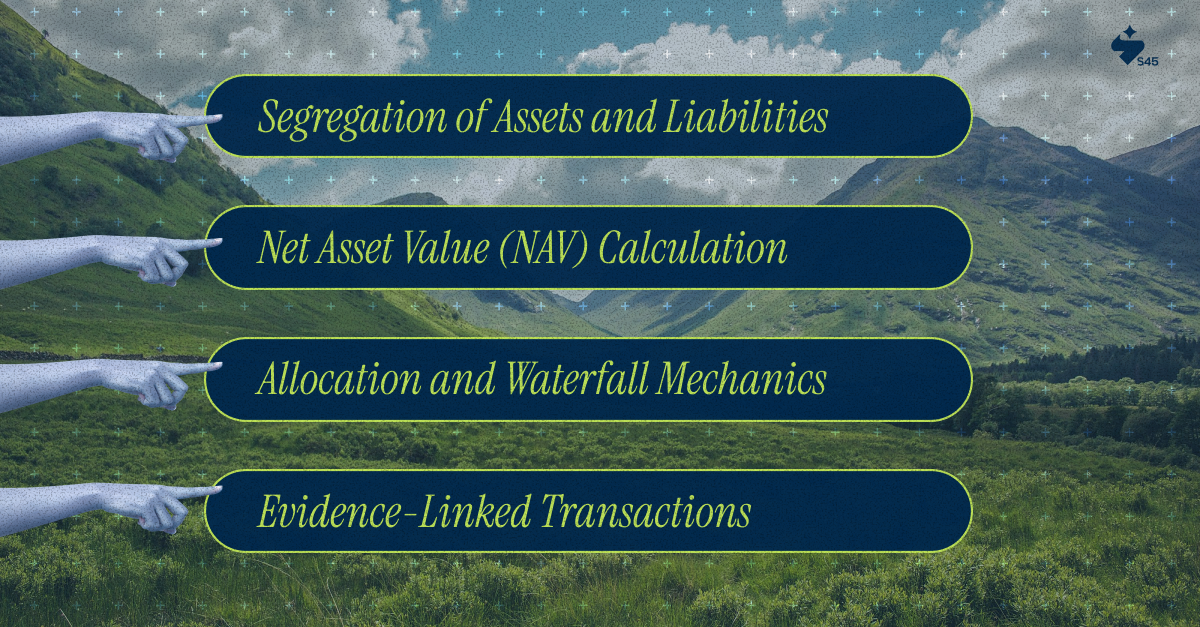

What is fund accounting in investment banking at the operational level? It's a methodology built on several core principles that directly affect IPO viability:

Investor capital must be tracked separately, including Series A, Series B, and promoter equity. Each must show subscription amount and date, entry valuation, attached rights (liquidation preference, anti-dilution, board seats), and current NAV.

For IPO-bound companies, this segregation determines:

Companies lacking investor-level segregation face costly reconstruction during due diligence.

NAV = (Total Assets − Total Liabilities) ÷ Outstanding Units.

NAV reconciliation matters because:

Profits are distributed per preferential rights:

For IPOs, waterfall mechanics affect promoter dilution, investor exit timing, and pricing anchors. Merchant bankers model these privately to ensure institutional return expectations are met.

Every transaction must trace to documentation: capital call notices, subscription agreements, board resolutions, and bank statements.

Rigorous fund accounting ensures a smooth drafting process for the DRHP. Treating it as a back-office function creates regulatory risk, investor skepticism, and IPO delays.

SEBI's ICDR (Issue of Capital and Disclosure Requirements) regulations govern every aspect of public market access. Fund accounting reconciliation affects multiple ICDR clauses:

Companies must disclose:

If fund accounting records are incomplete, these disclosures become guesswork. SEBI queries follow. Timelines extend.

Promoters must hold at least 20% of the post-issue shares for three years (lock-in). But determining who qualifies as "promoter" vs. "investor" depends on cap table analysis, a fund accounting exercise.

Companies that received PE funding often have ambiguous classifications: Is a founder-affiliated investment vehicle a promoter or investor? Fund accounting clarity resolves this before SEBI asks.

Pricing must be justified via:

If the last funding round was at ₹X per share but the IPO pricing targets ₹2X, SEBI expects a detailed justification. Fund accounting provides the evidence base: post-funding revenue growth, profitability inflection, sectoral re-rating.

S45's AI-Driven DRHP Drafting links every pricing assumption to verifiable evidence. When SEBI asks why valuation doubled in 18 months, the answer references specific financial performance milestones, audited results, and comparable market movements, not promotional language.

Promoters preparing for IPO face emotional cost beyond spreadsheets.

Institutional investors introduced discipline: board oversight, quarterly reviews, and performance metrics. But they also introduced complexity: term sheets with clauses that now constrain IPO pricing, liquidation preferences that dilute founder upside, and governance provisions that complicate decision-making.

Understanding what is fund accounting in investment banking is helps founders see the trade clearly:

S45's approach acknowledges this tension. We don't optimize for investor exit alone. We design capital structures that balance:

This requires operational empathy paired with institutional discipline. When a founder resists dilution, we model scenarios: at what IPO price can investors exit whilst promoters retain 51%? If preferential rights result in additional dilution, what alternative structures are available?

Fund accounting isn't just numbers. It's negotiating inherited constraints toward viable outcomes.

Every SEBI comment letter begins the same way: "Provide evidence supporting…"

Not projections. Not intent. Evidence. Companies that maintained rigorous fund accounting from the first PE round answer SEBI queries in days. Companies that didn't spend months reconstructing transaction trails.

S45's operational premise is simple: if a claim appears in your DRHP, the supporting evidence must exist in digital form, version-controlled, and cross-referenced to source documents.

When we draft: "The Company raised ₹50 crore in Series B at ₹200 per share from XYZ Fund on [date]," our AI systems verify:

If any document is missing, the disclosure doesn't appear. If the evidence conflicts, we resolve the conflict before drafting.

This evidence-first methodology isn't perfectionism. It's risk management. In 2024, 143 DRHPs were filed with SEBI, up from 84 in 2023. Not all reached the listing. Many stalled due to documentation gaps that fund accounting discipline would have prevented.

AI cannot replace a banker's judgement. But AI can compress workflows that traditionally consumed months.

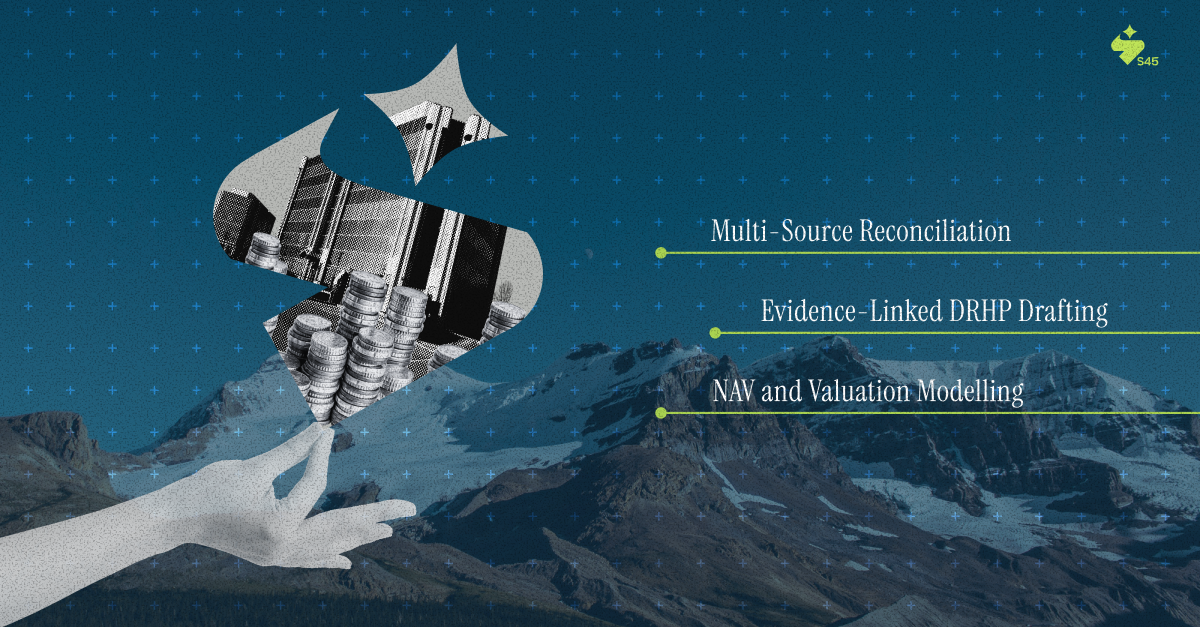

S45's proprietary AI systems address what is fund accounting in investment banking by:

This is why S45 compresses mandate-to-DRHP timelines. The work remains the same; the manual reconciliation is automated.

Before engaging an investment bank, promoters preparing for an IPO should audit their fund accounting readiness:

For every funding round:

If any document is missing, start reconstruction immediately. This work happens regardless, better to own it before SEBI mandates it.

Run parallel analysis:

If these three sources show different pictures, SEBI will notice. So will institutional QIBs during roadshows.

Some investor rights don't survive IPO:

Resolve these before the mandate. Investor negotiations during DRHP drafting delay timelines and weaken the bargaining position.

Institutional investors expect liquidity. For Main Board listings, this usually occurs naturally through market trading. For SME listings, liquidity design becomes critical.

Model scenarios:

This liquidity modelling is fund accounting extended forward, with an understanding of investor obligations post-listing.

Traditional merchant banks handle fund accounting as a compliance checkpoint in the late stages of IPO preparation. The workflow looks like:

This sequential approach creates delays because fund accounting reconciliation should happen before merchant banker engagement, not after.

S45 inverts this by offering IPO Readiness Scan as a pre-mandate service. We audit:

Promoters then know their starting position before committing to the IPO. If fund accounting requires three months of reconstruction, we identify that upfront, not during DRHP drafting when time pressure is acute.

This operational transparency reflects S45's institutional approach: we're not advisors who hand problems back to clients. We're execution partners who own workflow compression.

Most IPO delays aren’t market-driven. They’re workflow failures.

Fund accounting in investment banking makes one thing clear: institutional capital creates institutional obligations. Address them early, or manage them under SEBI scrutiny.

S45 treats fund accounting as execution infrastructure. Our capital structure mapping answers three questions: can the company reach IPO with current investors intact, does pricing balance founder and institutional returns, and will SEBI accept the disclosure evidence?

These questions must be resolved before the mandate, not during DRHP drafting. That’s why S45 offers capital structure consultation as a standalone service.

It’s not a free conversation, but it’s definitive. For companies with institutional capital considering Main Board or SME listing, it provides clarity before months, credibility, and board capital are at risk. Because in Indian markets, fund accounting determines whether an IPO takes six months or eighteen.

Fund accounting in investment banking is the core infrastructure for Indian enterprises preparing to access public markets, and it sits at the intersection of capital management, regulatory compliance, and investor relations.

For promoters with PE or VC capital, understanding fund accounting means recognising institutional disciplines, asset segregation, NAV calculation, allocation waterfalls, and evidence-linked transactions that directly affect IPO viability, pricing credibility, and regulatory timelines.

S45 treats fund accounting reconciliation as execution infrastructure, not clean-up. Our AI-native platform compresses reconciliation from months to weeks, ensuring SEBI disclosures align with verifiable evidence and institutional pricing.

India’s IPO momentum creates opportunity, but velocity demands discipline. Companies that maintain rigorous fund accounting transition smoothly to DRHP drafting; those that do not lose time to reconstruction and scrutiny.

Build IPO readiness with S45’s IPO Readiness Scan, where capital structure, investor obligations, and fund accounting meet institutional standards.

Discover more insights on similar topics