April 1, 202612 min read

Traditional vs Alternative Investments: What You Need to Know Before Going Public

By Aman Singh

Investopedia

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Your cap table is under scrutiny long before SEBI reviews your DRHP.

As Indian companies move toward IPOs, pressure builds beneath the surface. PE funds approach expiry. Early investors seek exits. ESOP holders need liquidity. Boards want certainty. All of this converges when valuation discipline and shareholder alignment are most important.

Traditional exits assume cooperative timing. Markets don’t. IPO windows shift, diligence drags, and valuations compress, while private equity fund clocks keep ticking.

This is where private equity secondaries have become essential.

No longer niche or distress-driven, secondaries now offer liquidity without dilution, investor rotation without disruption, and pricing discovery without public exposure. For Indian promoters navigating fund expiries, regulatory scrutiny, and IPO readiness at once, understanding secondaries is no longer optional; it’s structural.

The secondary private equity market involves the transfer of existing investor commitments, LP interests in PE funds, or direct stakes in portfolio companies, from one investor to another. Unlike primary investments that inject fresh capital into companies, secondary transactions provide liquidity to existing shareholders without diluting the company's equity base.

Private equity secondaries involve buying and selling pre-existing investor commitments to private equity funds or underlying assets, conducted outside established trading exchanges through structured bilateral transactions.

Two primary transaction structures dominate the secondaries market in private equity:

For Indian promoters, the distinction matters. LP-led transactions happen without your involvement. GP-led transactions, particularly continuation vehicles, directly impact your company's shareholder structure and may require board engagement.

The global private equity secondary market has expanded from $8 billion in 2005 to approximately $150 billion in 2024. This growth reflects structural necessity; fund-life constraints increasingly misalign with portfolio company IPO readiness.

GP-led secondaries now dominate the market, accounting for more than 50% of transaction volume in the 2020s. They are no longer residual exits for underperformers, but strategic tools to extend ownership of high-quality assets while managing liquidity.

For promoters preparing for public markets, secondaries create both opportunity and obligation:

But they also reshape cap table narratives, valuation defensibility, and disclosure risk.

S45 approaches secondaries through the lens of IPO outcome ownership. In capital market assessments, cap table cleanliness is non-negotiable. A recurring pattern emerges: strong businesses undermined by fragmented shareholding, multiple PE investors, misaligned fund lives, and legacy decisions made under pressure.

When structured with institutional discipline, secondary transactions solve specific pre-IPO frictions:

Secondaries, when integrated into IPO readiness frameworks, strengthen disclosure defensibility rather than introduce execution risk.

India's private equity landscape has deployed over $4 billion across PE and VC funds in July 2025. Most of these funds are closed-ended, with 7- to 10-year lifespans. The maths is straightforward: funds raised in 2015-2017 are now approaching the end of life, creating liquidity urgency.

India's AIF regime, established in 2012, imposes stringent end-of-life protocols that don't exist in many offshore jurisdictions. Once a fund reaches end-of-life, it enters a one-year liquidation period where assets must be sold or distributed. Extensions require approval by three-quarters of the LP base and the submission of a cash bid equal to at least 25% of the remaining NAV.

If no bid materializes, the remaining NAV is marked at ₹1 for reporting purposes, a severe penalty designed to force efficient liquidation.

This regulatory architecture creates a predictable transaction flow. GPs facing fund closure need structured exits. LPs need distributions to support new fund commitments. Companies need liquidity solutions that don't compromise IPO timelines.

Secondary market transactions could reach up to $20 billion annually in India, driven by regulatory constraints on onshore Alternative Investment Funds. For promoters, this means secondaries aren't optional; they are a structural requirement for funds operating under India's AIF framework.

Primary Investments: Inject fresh capital, dilute existing shareholders, occur during growth phases, reflect forward-looking valuations, and require board and shareholder consent.

Secondary Investments: Transfer existing stakes without new capital, with no dilution; occur when investors need liquidity; reflect current market pricing (often at NAV discounts); may or may not require company involvement, depending on the structure.

For IPO-bound companies, secondary transactions enable shareholder rotation without affecting operations, establish market-validated pricing without diluting promoter control, and demonstrate liquidity to potential anchor investors.

But they create disclosure obligations. Every secondary transaction must be documented in the DRHP. Every valuation adjustment is explained. Every new investor is identified through source-of-funds verification. S45's IPO Readiness Scan assesses whether your cap table can withstand this scrutiny.

The mechanics of what secondaries in private equity vary by structure, but certain operational principles remain constant. Understanding these fundamentals helps promoters evaluate whether secondary transactions align with their IPO preparation timelines and compliance requirements.

Continuation vehicles are the fastest-growing segment of private equity secondaries. These structures allow GPs to extend ownership of high-performing assets by transferring them into new vehicles with longer investment horizons.

For Indian companies, continuation vehicles solve timing misalignment. If your business needs 24-36 months to reach IPO-readiness but your PE investor's fund expires in 12 months, a continuation vehicle extends that runway.

The structure: GP forms a new continuation vehicle; existing LPs choose liquidity or roll-in; secondary buyers provide capital for exiting LPs; the company benefits from patient capital and an aligned timeline.

Foundation Private Equity's recent continuation vehicle for HCAH demonstrates the model's viability, allowing Quadria Capital to exit its 2013-vintage fund while maintaining exposure through the new vehicle.

For promoters, continuation vehicles provide negotiating leverage that avoids accepting rushed exit terms or compressed valuations.

Indian enterprises preparing for public markets should view secondaries through a portfolio-management lens, not merely as exit mechanisms.

When S45 assesses IPO viability, we comprehensively evaluate the secondary transaction landscape. This includes cap table complexity, transaction documentation quality, pricing consistency between secondary transactions and prior primary rounds, investor alignment with exit timelines, and regulatory compliance, including AIF end-of-life status.

This assessment determines whether secondary transactions are necessary, advisable, or detrimental to IPO timelines, and if necessary, how to structure them to compress execution and maintain SEBI compliance from inception.

Every secondary transaction creates a paper trail feeding directly into IPO disclosure obligations. SEBI requires detailed disclosure of all shareholders holding more than 1% of equity, all transactions in the 12 months preceding the DRHP filing, any off-market transfers, the source of funds for all investors, and the valuation methodologies.

Secondary transactions require careful consideration of transfer restrictions, shareholder rights, competition law thresholds, foreign exchange pricing, and reporting for cross-border transfers, tax optimisation, and governance continuity.

Poorly documented secondaries create SEBI comment risks extending DRHP review timelines by weeks. S45's AI-driven DRHP drafting links every disclosure to source documentation. Every secondary transaction must have board resolutions, valuation certificates, shareholder consent (if required), FEMA reporting (for foreign investors), and tax clearances.

Without this evidence architecture, secondary transactions that seemed like solutions become compliance problems.

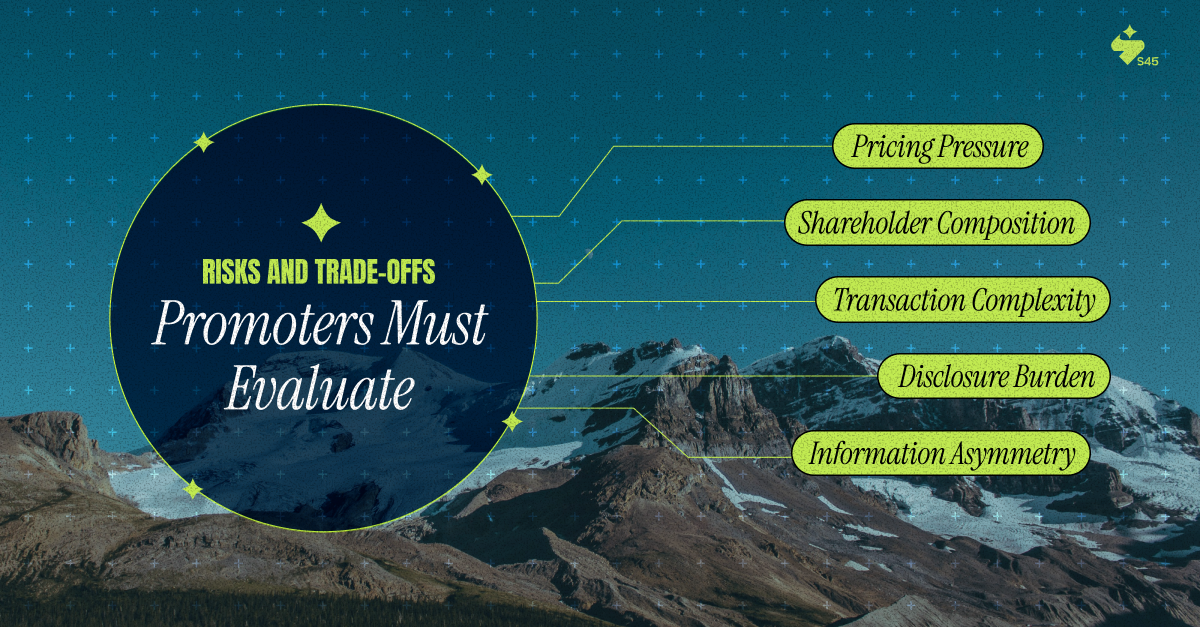

Secondaries address liquidity problems but create new complexities. Before engaging in secondary transactions, promoters must weigh specific risks that can affect both immediate execution and long-term IPO positioning.

The evaluation framework is straightforward: assess whether secondary transactions genuinely advance IPO readiness or merely solve short-term investor pressure.

Secondaries aren't just pre-IPO tools. They're increasingly relevant post-listing, particularly for SME Exchange listings, where anchor-investor lock-ins create liquidity constraints.

Indian SME Exchange regulations require a minimum 20% public holding at listing, anchor-investor lock-in periods, promoter lock-in on pre-IPO holdings, and market-making arrangements. These constraints create aftermarket illiquidity, particularly in the first 12-24 months.

Secondary market participants, particularly those focused on SME securities, provide liquidity bridges during lock-in periods. For companies listing on SME platforms, designing post-listing liquidity is as critical as achieving listing itself.

India's private equity secondaries market is following the maturation arc seen in developed markets, but compressed into a shorter timeframe by regulatory catalysts.

Several factors will drive continued growth: fund maturation cycle (large PE funds raised 2015-2019 entering end-of-life creates predictable transaction pipeline through 2027-2029); AIF regulatory framework (strict end-of-life protocols force structured exits); public market access (India's robust public markets provide ultimate exit pathway); institutional sophistication (emergence of India-focused secondary funds creates local execution capacity).

For promoters preparing for public markets, the question isn't whether secondaries will affect your journey; it's whether you'll structure them proactively or react under time pressure.

Private equity secondaries have evolved from distressed exit mechanisms into institutional infrastructure for portfolio management. In India, regulatory architecture and fund maturation cycles are accelerating this transition.

For promoters preparing enterprises for public markets, secondaries function as tactical tools for cap table optimisation, investor alignment, and pricing discovery. But they demand institutional discipline, evidence-based decision-making, regulatory compliance, and documentation rigour.

The chaos gap arises when companies treat secondaries as standalone transactions rather than as integrated components of their capital markets strategy. Institutional frameworks embed secondary evaluation into IPO readiness, ensuring each capital event advances public market objectives.

Before executing a secondary, assess its impact on SEBI disclosures, valuation narratives, and investor composition. Before dismissing them, test whether the cap table complexity will withstand DRHP scrutiny.

Evaluate how secondary transactions affect IPO readiness. S45’s IPO Readiness Scan analyses cap table complexity, investor alignment, and documentation integrity.

Discover more insights on similar topics