April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Key Takeaways

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

If you're an MSME founder exploring private equity funding, you've probably heard the term "carried interest" thrown around in investor meetings. It sounds technical, maybe even intimidating. And if you nodded along without fully grasping what it means for your business, you're not alone.

Many MSME founders sign term sheets without realising how this clause drives investor behaviour. When structured well, it pushes your PE partner to focus on long-term value instead of a quick flip. This guide breaks it down in simple terms, highlights what really impacts your outcome, and shows you the red flags that matter before you close the deal.

This blog breaks down carried interest in plain language, shows you what to negotiate, and helps you spot red flags before signing anything.

Carried interest is the profit share your PE partner earns when they generate real value, not a fixed fee. They usually receive 20 percent of profits only after beating the 8 to 12 percent hurdle rate.

Their salary comes from the annual 2 percent management fee, but carried interest is their true upside. This structure pushes them to focus on the long-term outcome

Here's the distinction that matters:

Your PE partner takes on risk by investing time, expertise, and capital into your business. They only earn substantial returns when they successfully navigate market challenges and help you grow.

Key numbers every founder should know:

Now that you understand what carried interest is, let's look at exactly how your PE partner earns it and what the money flow looks like when your business hits an exit.

Understanding the concept is one thing. Seeing the actual money flow is another. Let's walk through a realistic MSME scenario, so you know exactly where every rupee goes when your business exits.

Before we dive into the numbers, you need to know who sits on which side of the table.

These roles matter because the waterfall distribution follows a strict hierarchy based on who you are in this structure.

Imagine your manufacturing business raises ₹20 crores from a PE fund. The terms include a 12% hurdle rate and 20% carried interest. Five years later, you successfully exit by selling to a strategic buyer for ₹40 crores.

Here's how the ₹40 crores gets distributed:

This waterfall structure isn't arbitrary. Each step protects your downside while motivating your PE partner's upside. But the protection goes even deeper with specific contractual clauses.

These four provisions ensure the waterfall actually works the way it's supposed to, even when things get complicated:

These aren't just legal terms buried in contracts. They're built-in mechanisms that keep your PE partner accountable throughout the entire investment period. A well-structured carried interest agreement means your partner can't game the system or walk away after early wins.

At S45, we structure carry terms that align with sustainable growth timelines, not just exit pressures. Our partnerships include transparent waterfall provisions from day one, so founders know exactly how value gets distributed before signing.

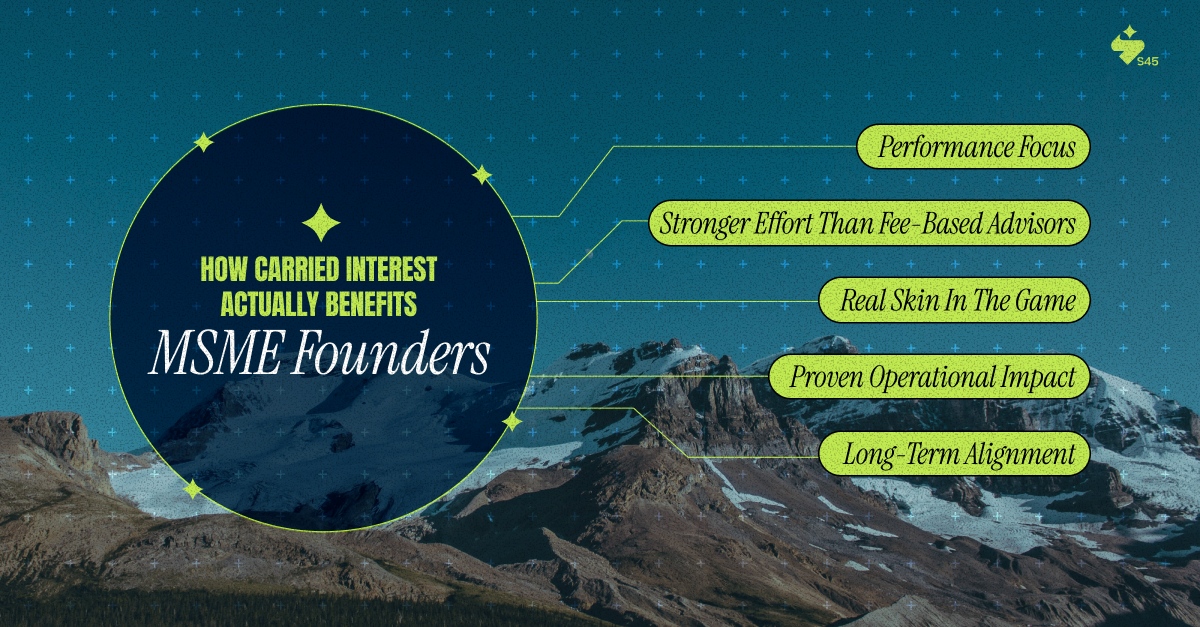

The waterfall distribution shows you the mechanics, but here's what really matters: how does this structure actually benefit you as a founder?

Most founders see carried interest as something their PE partner earns. That's technically true, but it misses the bigger picture. The real question is what you get in return for structuring compensation this way.

The carried interest model has worked for centuries because it solves a fundamental problem in partnerships: how do you ensure advisors care as much about your success as you do? The answer is simple. Tie their wealth to your outcomes, not their effort or time spent.

But understanding the benefits is only half the picture. India's regulatory environment has evolved significantly, especially with recent changes that directly impact how carried interest works for MSME founders.

If you've been researching PE funding over the past few years, you've probably encountered confusion around how carried interest gets taxed in India. The good news is that 2025 brought much-needed clarity.

The Finance Bill 2025 made a decisive call. Carried interest is now officially treated as capital gains, not business income. This wasn't just semantic clarification. It resolved years of debate between tax authorities and the PE industry about whether carry should be taxed like salary or investment returns.

What this means in practical terms:

Why does their tax rate matter to you? Simple. When quality PE firms find India tax-efficient, you get access to better partners with deeper expertise.

Here's where things got messy before 2024. Tax authorities argued that carried interest was essentially a service fee, which meant it should attract 18% GST on top of income tax. If that had stuck, the combined tax burden would have exceeded 40%, making India one of the least attractive PE markets globally.

The Supreme Court stepped in and upheld a Karnataka High Court ruling with a critical distinction. Since most AIFs operate as trusts, and trusts aren't considered separate taxable persons for service provision to themselves, GST doesn't apply to carried interest distributions.

The founder benefit here is direct:

This wasn't a minor technical fix. It fundamentally changed the economics of running PE funds in India, making the entire ecosystem more founder-friendly.

While tax clarity grabbed headlines, SEBI's ongoing regulatory framework deserves equal attention. These rules create transparency that protects you during negotiations:

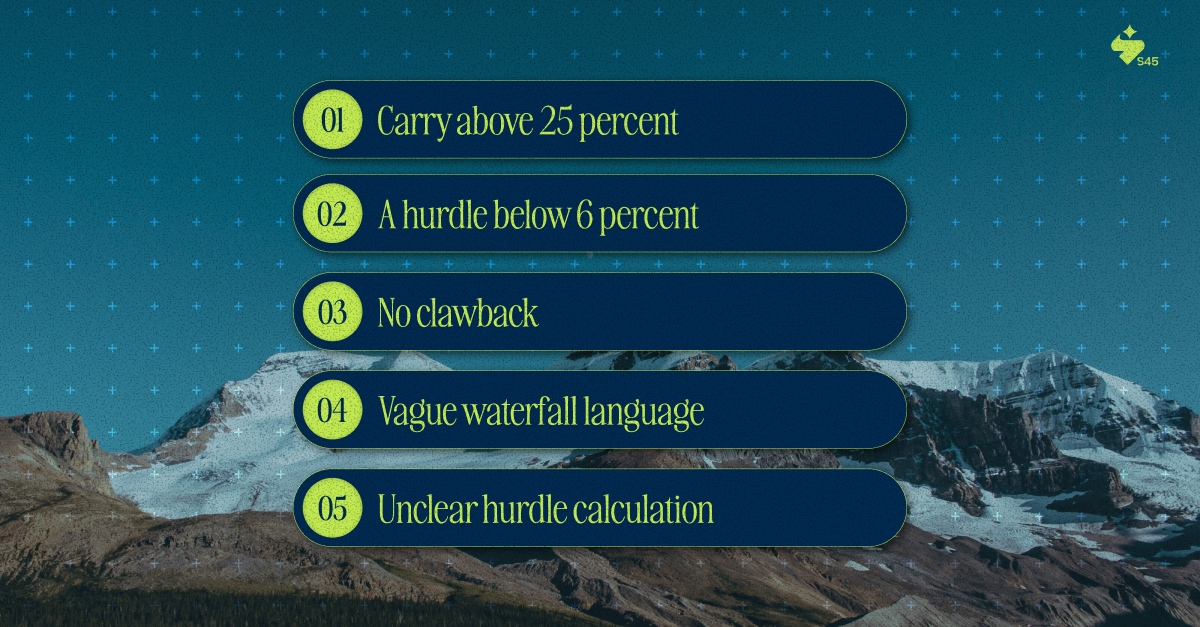

Before any meeting with a PE firm, request their standard PPM template. SEBI requires them to provide this. But even in this improved environment, not all PE deals are created equal. You still need to watch for warning signs in how carried interest gets structured.

Carried interest terms look simple, but small tweaks can shift millions. Watch for these issues during early discussions.

Understanding what to avoid is critical, but the real goal isn't just preventing bad deals. It's structuring partnerships where carried interest actually supports your vision for building a lasting business, not pressuring you into premature exits. At S45, we help founders catch these gaps early and negotiate terms that protect long-term value.

Carried interest isn't just a fee structure. It's the alignment mechanism that determines whether your PE partner wakes up thinking about your long-term success or their short-term exit.

The standard 20% carry with an 8-12% hurdle exists because it balances motivation with fairness. SEBI's regulations and 2025 tax clarity have made India's PE landscape more transparent than ever.

But transparency only helps if you know what you're looking at. Understanding waterfall distributions, clawback provisions, and red flags gives you the negotiation power to choose partners who genuinely walk beside you, not above you.

At S45, we help MSME founders navigate PE partnerships that align with their growth and legacy goals. Our approach goes beyond capital. We provide:

The right PE partner with clear carry terms can accelerate your path from MSME to market leader. Connect with our experts to evaluate your PE funding options with confidence and clarity.

Discover more insights on similar topics