April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You commit ₹25 crore to a Category II AIF. The fund manager calls ₹6 crore with 12 business days' notice. Your working capital is locked in inventory. Your receivables cycle runs 45 days. Your board meets quarterly.

The capital call does not care.

This is where sophistication in evaluating fund performance means nothing if you lack the infrastructure to execute the commitment you signed. The Alternative Investment Funds framework operates on a capital-on-demand basis. Simple in theory. Operationally brutal when it collides with running a ₹300 crore enterprise with seasonal cash flows.

Every missed deadline triggers penalty interest. Every documentation gap creates tax scrutiny. The damage compounds until SEBI's due diligence exposes what your board never examined: whether your commitment architecture can withstand regulatory scrutiny.

Most private equity advisory in India is transactional: close the commitment, collect the fee, move on. Execution is ignored. Liquidity cycles aren’t mapped to drawdown schedules. Treasury reserves aren’t stress-tested against historical call patterns. Fund commitments remain disconnected from working capital, tax calendars, and capex plans.

The result is predictable. Promoters sophisticated enough to assess IRRs still scramble for bridge financing to meet capital calls they approved months earlier. Advisory support ends exactly where operational complexity begins.

What separates institutional-grade drawdown management from chaos is infrastructure, not sophistication. Systems that model probabilistic cash flows. Workflows that auto-generate evidence trails. Compliance is embedded into treasury operations, not applied retroactively. Platforms like S45 treat drawdowns as execution architecture integrated with operating rhythms, regulatory calendars, and governance from day one.

In Indian markets, PE outcomes hinge less on fund managers and more on whether promoter systems can sustain drawdown discipline across 3–5 year commitments.

The mechanics of drawdown private equity are deceptively straightforward. The operational implications for Indian promoters running enterprise-scale businesses are anything but. Understanding the structural difference between commitment and deployment is the first step toward building systems that can execute across multi-year capital call cycles without creating liquidity crises or compliance gaps.

The drawdown private equity model operates on a commitment-based structure. When you invest in a private equity fund registered as a Category II AIF under SEBI's Alternative Investment Fund Regulations, 2012, you are not transferring the full committed amount on Day One.

Instead, you sign a binding commitment (let's say ₹25 crore), and the fund manager (General Partner) draws down portions of this capital through formal capital calls as investment opportunities materialise or operational expenses arise.

A typical private equity fund operates over a 3–5-year investment period, during which capital is called in tranches. For instance:

Each capital call typically provides 10–15 business days' notice, specifying the required amount, the purpose (investment opportunity, management fees, or fund expenses), and the transfer deadline.

Here is what makes this operationally complex in India:

SEBI has proposed amendments requiring close-ended AIFs to execute drawdowns on a strictly pro-rata basis, meaning your capital is called in the same proportion as profits will eventually be distributed. Once disclosed in the Private Placement Memorandum, this methodology cannot be changed. For promoters, this means no flexibility to negotiate timing based on your cash position.

Failing to meet a capital call triggers penalties defined in the LPA (Limited Partnership Agreement). Standard provisions include:

Every rupee you deploy into a drawdown private equity fund must be documented with source verification, especially if you are using inter-company loans, dividend repatriations, or asset sale proceeds. Tax authorities scrutinise these trails, and any gap in documentation can trigger reassessment proceedings years later.

Indian promoters face a structural disadvantage in managing drawdowns versus institutional investors. This is not about capital or sophistication; it is about infrastructure built for continuous liability management rather than working capital cycles. That gap determines the success of execution under time pressure.

Institutional investors model liquidity, simulate drawdowns, and maintain segregated reserves through dedicated systems. Firms like S45 bring this institutional-grade drawdown infrastructure to Indian enterprises through AI-native workflows, replacing fragmented processes with integrated execution.

Indian promoters: even those running enterprises with ₹500+ crore in revenue rarely have this infrastructure.

Instead, they manage PE commitments through:

This creates what defines execution failure in Indian private equity allocation: the operational distance between what you committed and your institutional capacity to execute that commitment with precision, speed, and evidence.

The Chaos Gap expands when:

Traditional advisory firms do not solve this. They are not built for operational execution. They optimise for deal origination and mandate closure.

If you are a promoter with PE commitments and are contemplating an IPO within the next 24-36 months, drawdown management becomes exponentially more complex. The operational disciplines required for institutional-grade commitment execution overlap directly with the evidence standards SEBI demands during DRHP review. Capital markets execution platforms like S45 integrate PE commitment architecture with IPO readiness workflows precisely because these are not separate challenges but interconnected execution requirements that determine whether your path to public markets succeeds or stalls in regulatory review cycles.

Here is why the integration matters:

SEBI's ICDR Regulations require full disclosure of all related-party transactions. If you are funding your PE commitments through inter-company loans or dividend stripping from your operating companies, every transaction must be disclosed and justified.

Gaps in documentation create SEBI comment cycles that delay your DRHP filing by months.

PE investors in your company will have lock-in obligations after the IPO. If you simultaneously hold LP interests in funds that invest in your sector, you may face conflict-of-interest disclosures or trading restrictions that limit your flexibility.

Institutional investors in your IPO will scrutinise your working capital adequacy. If you have significant unfunded PE commitments that are not disclosed or adequately reserved for, it signals weak treasury discipline and affects your pricing.

Because in Indian capital markets, everything connects. Poor execution in one area destroys credibility across the entire structure.

The private equity industry obsesses over fund selection: which GP has the best track record, which vintage year offers optimal entry, which sector focus provides maximum upside. All of this matters. But none of it compensates for execution failure at the drawdown level, because operational friction in Indian capital markets compounds in ways that destroy returns before fund performance ever becomes relevant.

A poorly selected fund with disciplined drawdown execution will outperform a top-quartile fund where you miss capital calls, incur penalty interest, or create documentation gaps that trigger tax reassessments.

Why?

Because in India, operational friction compounds. A missed capital call does not just cost you penalty interest. It creates:

Each of these creates downstream costs that erode returns far more than a 2% difference in fund performance.

This is why S45 treats drawdown management as capital markets craftsmanship: not administrative overhead.

Precision in drawdown execution is not about adding bureaucracy. It is about building systems that make execution inevitable rather than aspirational. Here is the execution standard that separates institutional-grade commitment management from reactive crisis handling:

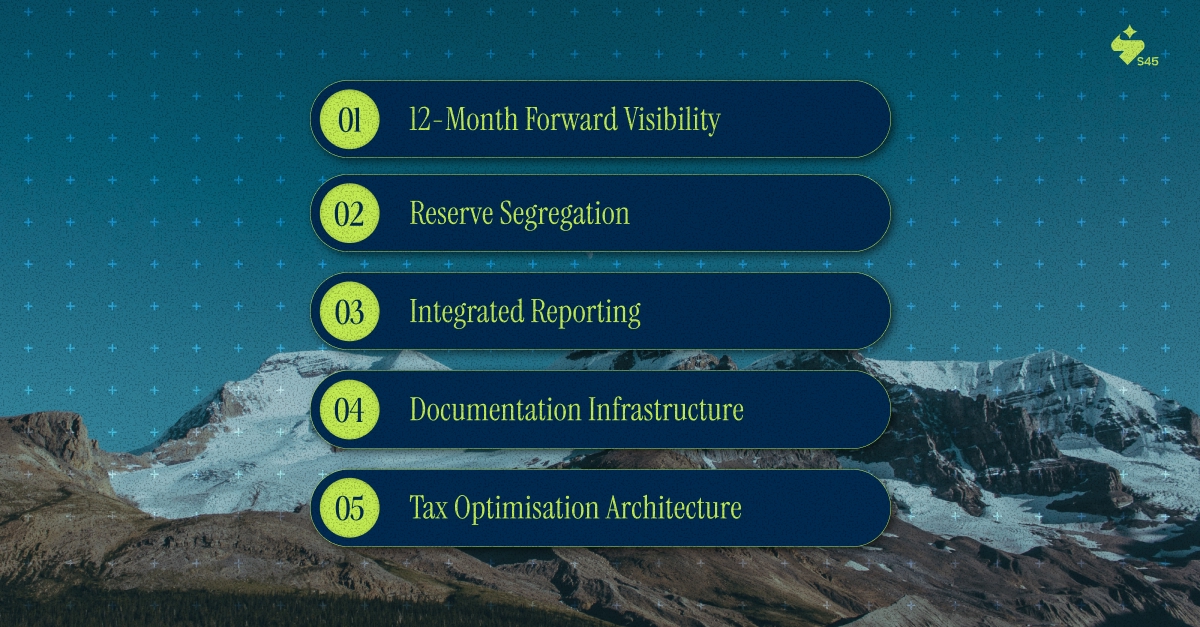

You should have probability-weighted projections of capital calls for the next four quarters, updated monthly based on fund deployment velocity and new commitment additions.

Liquidity reserves for unfunded commitments should be segregated in liquid, yield-bearing instruments (liquid mutual funds, Treasury bills, overnight repos) with automated redemption triggers tied to receipt of call notice.

Board papers should include a standing item on "Unfunded Commitment Status" showing:

Every capital deployment should auto-generate:

Capital deployments should be structured through holding entities with optimal tax positioning, considering:

This is not about adding bureaucracy. It is about building systems that make execution inevitable, not aspirational.

India’s approach to drawdown private equity has tightened sharply. SEBI’s push for standardisation now directly shapes how capital calls operate and limits fund manager flexibility. Promoters who understand this can build compliance into commitments early, rather than retrofitting it during the SEBI review.

SEBI’s consultation paper proposes strictly pro-rata drawdowns for close-ended Category II AIFs, aligned with profit distribution.

Key implications:

Fund managers cannot call capital from only certain investors while allowing others to defer. Every capital call must be proportional across all LPs.

Once disclosed in the Private Placement Memorandum, the drawdown methodology cannot be changed until scheme maturity. This eliminates mid-course flexibility.

AIFs using alternative drawdown mechanisms must align with SEBI's framework for all future calls, though existing drawdowns are grandfathered.

Importantly, shifting to the pro rata methodology is not classified as a "material change," so funds do not need to offer exit options to investors before implementation.

For promoters, this means:

The regulatory direction is clear: private equity drawdowns in India are moving toward standardisation, transparency, and reduced discretion.

Fund managers who previously offered flexible timing accommodations will lose that discretion. Promoters who relied on relationship capital to negotiate delays will find those conversations impossible.

This is execution infrastructure becoming a regulatory mandate.

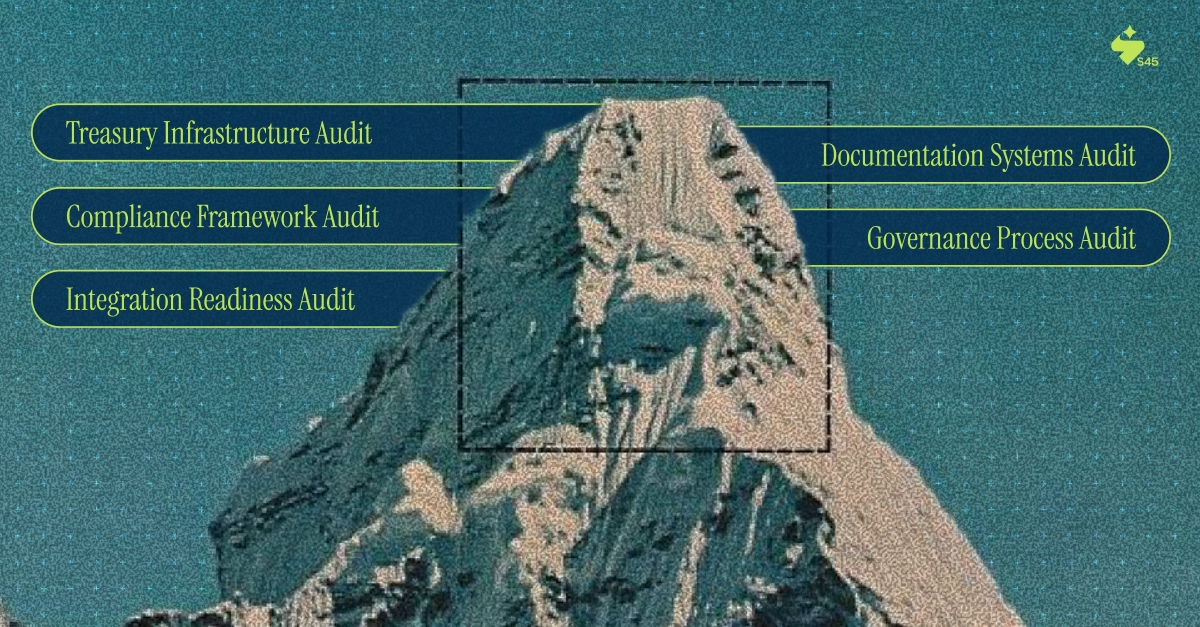

Before committing to any drawdown private equity fund, audit your institutional readiness against these operational dimensions. This is not about checking boxes. It is about an honest assessment of whether your current infrastructure can execute multi-year commitment obligations with the precision that Indian capital markets demand. Gaps identified here become implementation priorities before you sign, not crises after capital calls arrive.

If you cannot answer "yes" with confidence to most of these, you lack the institutional infrastructure for drawing down private equity at execution grade.

This is not about sophistication. It is about systems.

In Indian capital markets, systems determine whether your capital allocation creates value or chaos.

If you are a ₹200+ crore revenue enterprise considering public markets within 36 months, your approach to drawdown private equity determines more than just your fund returns. It determines execution capacity across the entire capital markets preparation journey.

It determines:

Poorly documented PE commitments prompt extensive SEBI queries regarding related-party transactions, sources of funds, and conflict management. Each query adds 15–30 days to your DRHP approval timeline.

Institutional investors conducting due diligence scrutinise treasury discipline. Evidence of missed capital calls or reactive liquidity-management signals indicates weak governance and can affect allocation decisions.

Unfunded commitments that are not transparently disclosed and reserved for affect how analysts model your working capital adequacy, influencing price targets and recommendations.

If your PE fund interests create conflict-of-interest scenarios with your own IPO, SEBI may impose additional lock-in requirements on your promoter holdings, reducing your post-listing liquidity.

Capital structure design and capital markets execution must be integrated from the outset, treating PE commitment architecture and IPO disclosure obligations as connected workflows rather than sequential problems.

Here is the execution standard that separates institutional-grade drawdown management from operational chaos. These are not aspirational best practices. They are minimum thresholds that determine whether your PE commitments create value or create compliance gaps that destroy credibility during SEBI review, tax audits, or institutional investor due diligence. Demand this from yourself and from any execution partner you engage.

Every rupee deployed into a drawdown private equity commitment is traceable to:

Unfunded commitments are managed through:

Board receives:

Every commitment structure is evaluated against:

This is not an aspiration. This is execution discipline that determines whether your capital allocation creates institutional credibility or regulatory risk.

Drawdown private equity is not a complex concept. It is a complex operation.

The mechanics are simple: commit capital, respond to calls, maintain reserves, and document sources. The execution is brutal: probabilistic liquidity planning across multi-year horizons, evidence trails that survive regulatory scrutiny years later, and governance frameworks that treat unfunded commitments as dynamic liabilities rather than static footnotes.

The difference between a commitment that creates value and one that creates chaos is never fund manager performance. It is the institutional capacity to execute capital calls with precision, speed, and evidence while running a ₹300 crore enterprise with seasonal cash flows and concurrent obligations.

Indian promoters who apply infrastructure discipline to PE allocation extract real value.They use systems that model cash flows probabilistically. They rely on workflows that auto-generate audit-defensible documentation. And they integrate governance that tracks commitments alongside working capital and disclosure obligations.

S45 enables this execution discipline through AI-native infrastructure built for drawdown precision and capital markets scrutiny. For enterprises preparing for institutional capital and eventual public markets, S45 turns commitments into controlled execution.

Discover more insights on similar topics