April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

The gap between a signed shareholder agreement and a successful private equity exit is where Indian companies lose control, valuation, and time.

SEBI wants three years of clean, audited financials. Your related party transactions need restructuring. Strategic buyers are conducting forensic due diligence on customer contracts you've never properly documented. Your PE fund's investment committee is asking why DRHP drafting is taking six months, given that their fund lifecycle requires liquidity now.

Exit value in India reached $26 billion in 2024, with public markets driving the majority. But behind these numbers lie operational failures that go unacknowledged. Companies withdraw DRHPs after SEBI observations. PE investors sell stakes at deep discounts during market corrections. During exit execution, promoters discover that their evidence architecture cannot support their growth claims.

Private equity exits don't fail because of bad strategy. They fail due to fragmented workflows, delayed evidence gathering, and the assumption that "having an exit plan" equates to "being ready to execute an exit."

Most PE-backed companies believe they're exit-ready because they have relationships with merchant bankers and retain legal counsel. The institutional reality is different.

Private equity exits fail in India not because of market conditions but because of workflow fragmentation. The typical IPO exit path requires merchant bankers, legal counsel, registrars, financial audits, DRHP drafting, founder dilution management, lock-in negotiations, and hoping SEBI observations don't derail timelines by four months.

Each step is handled by different advisors using different systems. CFOs manage Excel cap tables. Lawyers redraft disclosures manually. Merchant bankers wait for "clean financials" before pricing discussions. PE investors ask when they can begin selling. Nobody owns the outcome.

This is the chaos gap, where strategy meets fragmented execution and private equity exits break. AI-native investment banks like S45 are addressing this by pairing proprietary AI systems with sector bankers to reduce DRHP drafting from 4-6 months to 30-45 days, but the fundamental issue remains: most companies identify evidence gaps during exit execution, not before.

The solution isn't hiring more advisors. It's continuously building evidence architecture, treating SEBI compliance as craftsmanship, and understanding that exit readiness begins at investment entry, not when PE funds need liquidity.

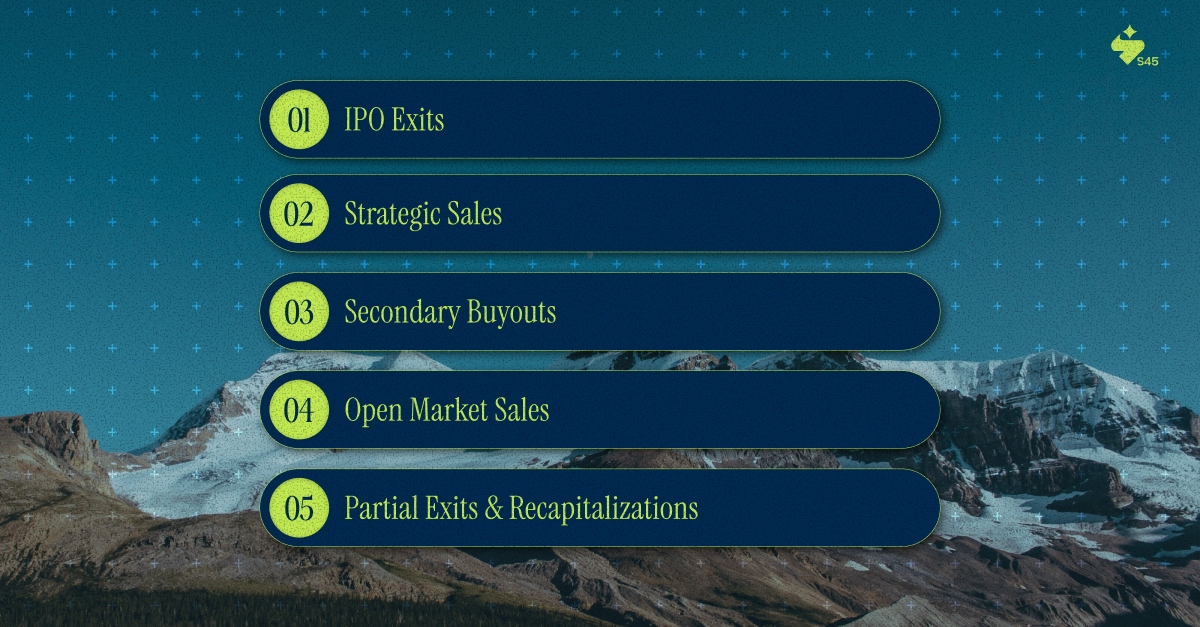

Understanding exit mechanics matters because each route demands different preparation timelines, evidence requirements, and regulatory workflows. Companies that grasp these distinctions early extract better multiples and preserve control during transitions.

IPO exits accounted for 46% of total exit value in November 2025, representing $1.5 billion across seven IPOs. Public markets offer valuation depth, liquidity access, and credibility that private transactions rarely match.

SEBI's ICDR regulations require exhaustive disclosures:

Each disclosure must be evidence-linked and defensible under regulatory scrutiny.

Traditional IPO timelines run 12-18 months from mandate to listing. DRHP drafting alone consumes 4-6 months because firms draft manually and treat SEBI observations as surprises rather than predictable regulatory patterns.

AI-driven institutional approaches are compressing this timeline to 30-45 days by automating evidence linkage, disclosure generation, and compliance mapping while maintaining banker judgment for materiality decisions. This reduces the window where PE exit timelines and promoter control concerns create friction.

Strategic sales to corporate buyers within the same sector command premium multiples because buyers pay for strategic advantages: market share consolidation, distribution network access, or intellectual property integration, not just financial returns.

Strategic sales reached $2.4 billion in H1 2024, a 3.5-fold increase from H1 2023. Tata Consumer's acquisition of Capital Foods ($460 million) demonstrates how strategic buyers deploy capital for sector consolidation.

Strategic buyers conduct operational due diligence that goes beyond financial audits:

Evidence architecture quality determines negotiation leverage. Buyers discount valuations heavily when operational risks emerge during diligence that weren't disclosed upfront.

Strategic sales create institutional tension. Buyers want management continuity and operational integration. PE investors want a full exit and maximum valuation. Promoters worry about legacy preservation and loss of control.

These conflicts require disciplined transaction structuring, not emotional negotiation. Earnout clauses, management retention agreements, and non-compete terms must balance competing interests while maintaining deal certainty.

Secondary sales are now the most popular exit mode. When one PE fund's investment horizon ends but the company isn't ready for public markets, another PE fund with a longer investment horizon and a fresh value-creation thesis steps in.

Secondary buyouts offer execution speed. No public market readiness required, simplified due diligence processes, and simpler regulatory approvals compared to IPO exits. But valuations rarely match IPO levels because buying PE funds underwrite their own return expectations, not public market enthusiasm.

Well-structured secondary sales preserve promoter rights, clarify expectations for new value creation, and set realistic timelines for the next exit. Poor execution leaves promoters managing conflicting investor demands while trying to run the business.

For PE investors in already-listed companies, open-market sales through block trades accounted for approximately 55% of all private equity exits in H1 2024.

Block trades allow PE investors to sell large stakes (typically above 1% of the company's equity) to institutional buyers in a single off-exchange transaction. The operational attraction is immediate: no DRHP drafting, no SEBI approvals for the exit itself, and no lock-in negotiations.

But open market exits depend entirely on market depth and buyer appetite. During market corrections, liquidity evaporates. PE investors must either accept discounted valuations or wait, which may not align with fund maturity timelines.

Recapitalization allows PE investors to extract partial returns while maintaining equity exposure. The company restructures its capital, typically by raising debt or issuing special dividends, returning capital to investors without triggering a full exit event.

This route gained prominence when exit markets froze during 2022-2023. PE funds facing pressure from limited partners used recaps to show cash distributions while keeping stakes in high-potential portfolio companies.

From a promoter perspective, recaps create breathing room. PE investors receive liquidity relief, immediate exit pressure is reduced, and the partnership continues to create value. But recaps increase debt levels on the balance sheet, which constrains future financing flexibility and can complicate eventual full exits by making the company appear overleveraged to potential buyers.

Exit Route | Preparation Intensity | Typical Timeline | Valuation Potential | Liquidity Depth | Key Risk |

IPO Exit (Main Board / SME) | Very High – 3 years audited financials, SEBI compliance, DRHP drafting | 12–18 months (30–45 days for AI-driven DRHP drafting) | Highest (public market multiples) | Strong (Main Board), Moderate (SME) | Regulatory delays, market volatility |

Strategic Sale | High – operational diligence, contract documentation, IP clarity | 6–12 months | Premium if a strategic fit exists | Full liquidity at closing | Buyer renegotiation during diligence |

Secondary Buyout | Moderate – financial diligence, growth thesis validation | 3–6 months | Moderate (PE-return driven) | Full liquidity at closing | Valuation compression vs IPO |

Open Market Sale (Block Trade) | Low – company already listed | Weeks to months (market dependent) | Market-driven | High if market depth exists | Liquidity evaporates in downturns |

Partial Exit / Recapitalization | Moderate – capital restructuring, lender alignment | 3–9 months | Limited (partial liquidity only) | Partial | Increased debt burden, future exit constraints |

The institutional difference between successful and failed private equity exits lies in when evidence gathering begins, not how sophisticated the exit strategy sounds on paper.

Most PE-backed companies treat an exit strategy as a future decision. The institutional reality: exit readiness begins at investment entry, not when funds need liquidity. PE investors underwrite specific exit routes based on company characteristics.

IPO exits require three years of audited financials with clean audit opinions, properly disclosed related-party transactions, and operational metrics that support coherent institutional growth stories. Strategic sales need documented customer contracts with renewal rates, formalized supplier relationships with backup sourcing options, and intellectual property properly assigned to the company rather than held personally by promoters.

Forensic readiness assessments, like S45's IPO Readiness Scan, map what evidence exists today to support the exit thesis and identify what workflows must execute to close evidence gaps before exit windows open.

Most PE-backed companies discover evidence gaps during exit execution, when it's too late to fix them without 12-18 month delays. Institutional preparation means evidence architecture built continuously, not scrambled during exit negotiations.

The institutional opportunity in private equity exits isn’t replacing bankers with algorithms. It uses AI to compress repetitive evidence workflows, allowing human expertise to focus on decisions that determine exit outcomes.

Private equity exits have two execution layers:

AI-driven DRHP systems process financials, filings, board minutes, and contracts to produce evidence-linked disclosures. They map risk factors to operations, connect growth claims to contracts, and flag gaps where assertions lack support. This compresses DRHP drafting from 4–6 months to 30–45 days in institutional setups.

Speed creates optionality. When exit windows open suddenly, execution-ready companies move. Others remain stuck in manual bottlenecks.

AI alone fails without banker judgment. Algorithms cannot rank material risks or navigate regulatory nuance. Institutional execution pairs AI speed with experienced sector bankers, delivering precision that standalone advisory models cannot.

Exit execution depends not only on workflow discipline but also on managing the psychological tension among PE timelines, board expectations, and promoter legacy.

The real negotiation happens in boardrooms.

Exit disputes in India take an average of 4.7 years to resolve, with nearly 15% of PE exits (2018–2022) involving legal conflict. These disputes rarely stem from valuation mechanics. They arise from control retention, exit timing, and the prevalence of institutional priorities.

Institutional execution addresses founder concerns structurally, not emotionally:

Founders who convert control concerns into transaction design and separate them from resistance to institutional change achieve cleaner exits. Psychology matters, but only when translated into structure, not delay.

Listing venue selection fundamentally changes exit liquidity dynamics, yet most PE-backed companies make this decision based on eligibility criteria rather than exit execution implications.

Private equity exits in India are increasingly bifurcated by listing venue. Larger companies with annual revenue of ₹500+ crore typically target Main Board listings. Mid-market companies in the ₹80-300 crore revenue range are increasingly considering SME Exchange as a faster path to public markets.

Main Board listings offer institutional depth. Mutual funds, foreign institutional investors, and domestic institutions provide a natural buyer base for large PE exit volumes. Trading liquidity remains robust even during market corrections, allowing PE investors to exit substantial stakes without causing stock prices to crash.

SME Exchange listings offer speed and a lower compliance burden throughout the listing process. Eligibility criteria are less stringent. DRHP preparation timelines compress. Regulatory scrutiny, while still rigorous, focuses less on absolute scale and more on disclosure quality.

But SME listings face post-listing liquidity constraints. Trading volumes remain thin compared to Main Board stocks. Block buyers who can absorb large PE stakes are scarce. PE exit timing is critical because aggressive selling in low-liquidity stocks can trigger price crashes that prompt shareholder litigation and regulatory scrutiny.

Institutional firms model optimal exit schedules before DRHP filing. How much PE stake should be sold in the IPO? How much should be retained for post-listing sale once trading liquidity stabilizes? Which anchor investors can be approached who'll provide exit liquidity post-listing rather than just participating in the IPO?

These decisions require pricing analysis that balances maximizing PE exit value with retail investor protection concerns that SEBI will scrutinize. Poor liquidity design creates "dead listings" in which post-IPO trading volumes collapse, and PE investors cannot exit meaningful stakes without incurring significant valuation haircuts.

Strategic sales and secondary buyouts are accelerating, while block trades provide immediate liquidity for listed stakes. Yet aggregate numbers hide execution quality. The gap between premium exits and distressed secondary sales at 30–40% discounts is rarely market timing. It is a preparation discipline.

Exit readiness does not begin when liquidity is needed. It is evidence architecture built from entry, SEBI compliance treated as craftsmanship, and early recognition that each exit route demands different preparation timelines. It also requires managing founder psychology through transaction design, not emotional negotiation.

Companies that build evidence continuously, treat regulation as an execution parameter, and prepare before windows open achieve better valuations, cleaner transitions, and faster exits. In Indian capital markets, the difference between having exit rights and executing a premium exit is where legacy, valuation, and control are won or lost.

S45 helps PE-backed companies assess exit readiness early, identify evidence gaps, and remove execution bottlenecks. Through AI-native investment banking and sector expertise, S45 compresses exit preparation cycles without compromising regulatory precision.

Discover more insights on similar topics