April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

If you have raised PE capital and signed an LPA without fully understanding the catch-up clause, you are not alone. Most founders do not discover what it costs them until exit is on the table.

The catch-up provision governs how profits flow once investors have received their preferred return — and it determines far more than a percentage. It shapes how your PE investor behaves at the board table, how urgently they push for a listing, and how much patience they extend on pricing.

For Indian enterprises evaluating PE entry, pre-IPO capital, or a Main Board listing, this is not fine print. Firms like S45, an AI-native investment bank built for Indian capital markets, consistently see this knowledge gap surface at the worst possible moment: when liquidity is at its tightest.

This guide covers catch up in private equity with institutional precision. No approximations.

Before getting into the mechanics, it helps to understand where the catch-up clause sits in the broader structure of a PE fund. The concept is deceptively simple on the surface, but its implications ripple through every stage of a fund's lifecycle, from capital deployment to exit.

Catch-up in private equity refers to a contractual provision in a fund's Limited Partnership Agreement (LPA) that allows the General Partner (GP) to receive a disproportionately large share of profits, typically 100%, for a defined period after the Limited Partners (LPs) have received their preferred return (also called the hurdle rate).

The logic is straightforward: because LPs receive 100% of distributions up to the preferred return threshold, the GP is effectively excluded from profit-sharing during that phase. The catch-up clause corrects that imbalance, allowing the GP to catch up to its agreed carried interest share before the standard profit split resumes.

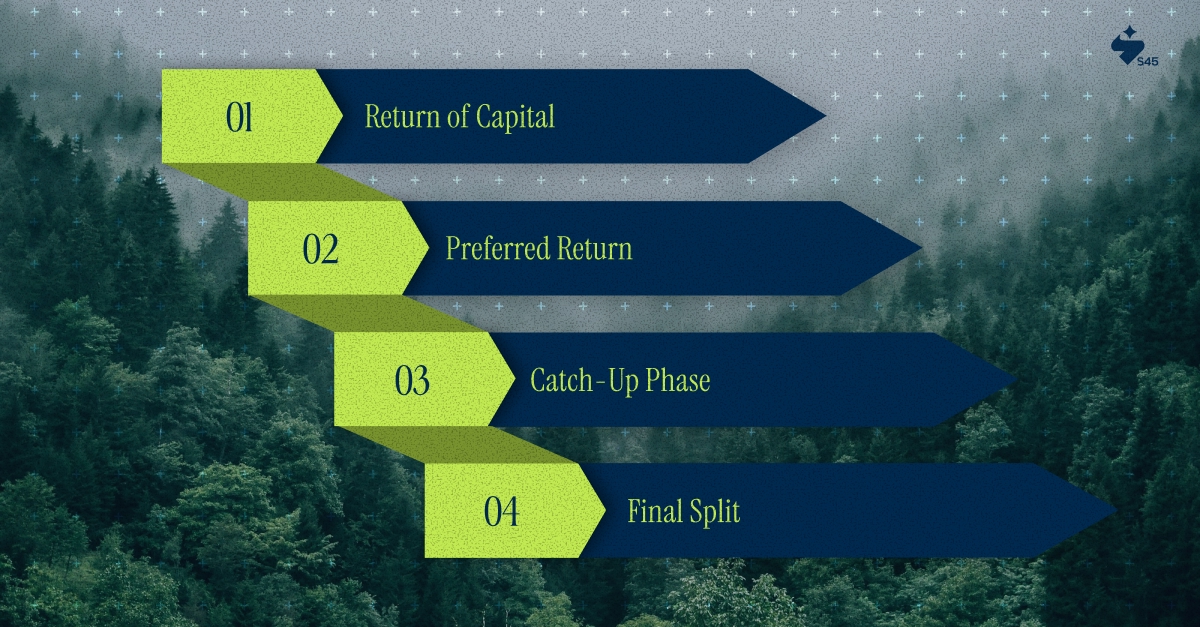

To understand catch-up in private equity, you need to understand the full distribution waterfall. Most PE funds follow a four-stage sequence:

The catch-up clause private equity structures fall into the third tier. It is not triggered until the LP has been made whole. It ends when the GP has received its proportionate share of total profits.

This is where most guides go vague. The actual mechanics of catch-up in private equity require precise calculation, because the GP is not simply taking 20% of profits above the hurdle. It is taking enough to represent 20% of all profits, including those already paid to the LP as preferred return.

Assume the following fund structure:

Step 1: Return of Capital

LPs receive back Rs. 100 crore in full before any profit-sharing begins.

Step 2: Preferred Return

LPs receive 8% annually on their Rs. 100 crore commitment. Over a 5-year fund, that accumulates to Rs. 40 crore (simplified). LPs receive this in full before the GP sees any carried interest.

Step 3: Catch-Up Phase

The GP now receives 100% of additional distributions. The GP needs to receive enough to make its share equal to 20% of all profits distributed to date. If LPs received Rs. 40 crore in preferred return, the catch-up amount is Rs. 10 crore (because Rs. 10 crore is 20% of the Rs. 50 crore total). The GP receives this Rs. 10 crore before the final profit split begins.

Step 4: Final Split

Any remaining profits are split 80% to LPs and 20% to the GP.

Not all catch-up clauses run at 100%. Some funds negotiate a 50% catch-up, meaning the GP receives half of the profits during the catch-up phase, and LPs receive the other half. This slows the GP's catch-up velocity and is generally more favorable for LPs.

The negotiation over the catch-up rate is a legitimate point of commercial tension. GPs prefer a faster catch-up at 100%, while LPs seek a slower build-up to protect themselves in scenarios where fund performance barely clears the hurdle. For Indian promoters reviewing PE term sheets, this clause deserves legal and financial scrutiny, not rubber-stamp approval.

The catch-up private equity provision does not operate in a vacuum. Its impact depends entirely on which distribution waterfall model the fund uses. There are two standard models, and they produce materially different outcomes for both GPs and LPs.

Under a European waterfall, the catch-up provision does not activate on any individual deal. The GP receives no carried interest until the entire fund, across all portfolio companies, has returned LP capital and the preferred return on that aggregate capital.

This structure is LP-friendly. It is the standard for large buyout funds and infrastructure vehicles globally. The GP must wait longer for economics, but there is no risk of carry being paid on early winners while later investments are still underwater.

Under an American waterfall, the catch-up clause activates on a per-deal basis. The GP can begin receiving carried interest on individual exits once that specific investment clears its hurdle, even if the fund as a whole has not returned LP capital.

This structure is GP-friendly. It accelerates GP economics and is more common among emerging fund managers who need earlier cash flow. For LPs, it creates clawback exposure: if later deals underperform, LPs must recover excess carry already paid to the GP.

Under SEBI's Alternative Investment Fund (AIF) Regulations, Indian PE funds structured as Category II AIFs are subject to specific distribution and carried interest frameworks. Understanding which waterfall model governs your PE investor's fund, and therefore how the catch-up private equity provision will behave, is essential due diligence for any Indian promoter or CFO accepting growth or pre-IPO capital.

A complete understanding of catch-up in private equity is incomplete without addressing the clawback provision that operates in the opposite direction, protecting LPs from overpayment scenarios.

A clawback clause gives LPs the right to recover carried interest already paid to the GP if the overall fund performance ultimately does not justify those payments. In practice, if a GP received catch-up distributions based on strong early exits but the fund as a whole underperforms, the clawback requires the GP to return excess carry, typically net of taxes.

The catch-up provision benefits GPs. The clawback protects LPs. A well-structured fund has both.

A GP nearing the end of its fund life with significant catch-up still uncollected may push for faster exits, aggressive monetization timelines, or secondary sales that do not align with the promoter's preferred liquidity path. Conversely, a fund with strong early performance and catch-up already cleared may demonstrate more patience on exit timing.

The catch-up mechanics of your investor's fund are not just their internal housekeeping. They are a behavioral driver that affects your business.

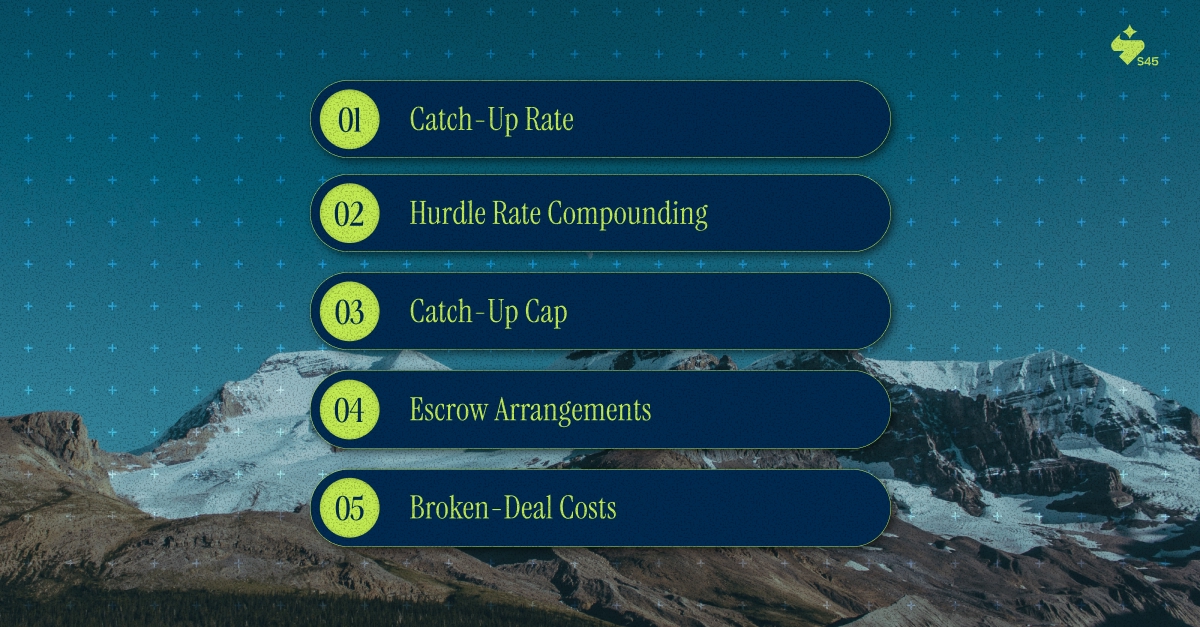

The catch-up clause private equity structures offer several legitimate points of negotiation. Institutional LPs, pension funds, family offices, and sovereign wealth funds routinely scrutinize these terms before commitment. Indian promoters and CFOs would do well to understand what these investors look for.

For an Indian CFO or board member reviewing a PE term sheet, each of these variables warrants explicit legal and financial analysis. Vague drafting in this section of the LPA is not an oversight; it is a risk that materializes at exit.

India's PE ecosystem has matured significantly over the past decade. Category II AIFs and Category I have raised substantial capital across growth equity, buyout, and pre-IPO funds. As this market grows, the documentation discipline expected of Indian fund managers has converged with global standards, but there remain gaps in how these terms are explained to portfolio company promoters and boards.

Many Indian companies raise PE capital in the 18-to-36-month window before a planned IPO. If the PE fund's catch-up provision is structured on a deal-by-deal basis, the GP may have a strong economic incentive to exit at IPO rather than hold through post-listing price appreciation. This directly affects how the fund participates in or resists lock-in structures post-listing.

For companies targeting SME Exchange listings, the liquidity window is narrower and secondary market depth is lower. PE investors with catch-up provisions pending may apply pressure on pricing or listing timelines that do not align with the promoter's preferred approach.

SEBI's regulatory framework for AIFs requires specific disclosures around distribution waterfall mechanics, but the depth of explanation provided to portfolio companies and co-investors varies significantly across fund managers.

Understanding catch-up in private equity is not a luxury for Indian promoters who have raised institutional capital. It is a prerequisite for managing investors intelligently as you approach a liquidity event. At S45, capital markets execution work for Indian enterprises consistently surfaces this gap, promoters who understood their businesses deeply but had not mapped the economics of their investors' fund structures before entering a liquidity process.

Even among experienced operators and CFOs, several misconceptions about catch-up in private equity persist. Clearing these up before you are in a live transaction is significantly easier than after.

This is the most persistent misconception. The catch-up is structured to give the GP 20% of total profits, including profits allocated entirely to LPs during the preferred return phase. The math looks the same at full distribution, but during the transition period, the GP receives a disproportionate share. In performance-sensitive environments, the difference is material.

It matters for a different reason. A fund that barely clears its hurdle enters a catch-up phase, in which the GP receives most of the marginal profits before any further LP upside. This is precisely the scenario where LPs argue the catch-up is most unfair, the fund produced modest returns, and the marginal economics favor the GP more than the headline 80/20 split suggests.

Fund economics shape the behavior of investors at portfolio companies in real and measurable ways. A promoter who dismisses this is managing an information asymmetry that will surface eventually, typically at a board meeting about timing, pricing, or exit structure.

Catch-up in private equity is a structural mechanism with precise mechanics and significant economic consequences. Where it becomes difficult is in the drafting — in the specific language around catch-up rates, hurdle compounding, escrow requirements, and clawback triggers that together determine real outcomes at exit.

For Indian promoters, CFOs, and boards navigating institutional capital, this literacy is table stakes. A well-structured PE relationship with clearly understood waterfall mechanics produces better alignment. A poorly understood one produces avoidable friction at exactly the wrong moment.

Before you commit months and reputation to a public markets process, get clarity on your capital structure first. Connect with S45 for a founder-level discussion on listing viability and capital market readiness.

Discover more insights on similar topics