April 7, 202611 min read

Catch-Up in Private Equity: Mechanics, Math & Meaning

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You have a company generating real revenue. Investors are willing to talk. The deal feels close. Then someone asks for the PPM, and the momentum stalls.

A PPM in private equity is a legally binding disclosure document. Under SEBI's AIF Regulations, 2012, every Alternative Investment Fund raising capital in India must file this document through a registered merchant banker, who must issue a due diligence certificate before it reaches any investor. This is the floor, not the ceiling.

Firms like S45, India's AI-native investment bank, exist because the gap between what a PPM should accomplish and what most companies produce is enormous. Fragmented advisors, recycled formats, and last-minute legal reviews produce documents that fail under investor scrutiny and invite SEBI comments, adding months to a transaction.

This guide covers what a PPM in private equity actually requires, how India's regulatory framework shapes it, and what execution precision looks like when it is done correctly.

A private placement memorandum is a legal disclosure document provided to prospective investors when a company or fund raises capital through a private securities offering. It is not a pitch deck. It is not a business plan. It is the document that governs the terms of the investment, discloses all material risks, and protects both parties if the deal sours.

In India, the PPM operates specifically within the AIF framework. SEBI's AIF Regulations categorize AIFs into three categories:

Each category has specific disclosure obligations, and the PPM must reflect them in full.

A PPM is specific to the AIF universe. It is distinct from a prospectus or DRHP, which governs public offerings under SEBI's ICDR Regulations. While an offer document for a listed entity requires full public disclosure, a PPM is a confidential document shared only with sophisticated, accredited investors. Its confidential nature does not relieve it of its legal obligation. It raises it.

A well-constructed PPM in private equity serves two simultaneous functions:

The tension between these two functions is where most PPMs fail. Firms either produce documents so laden with legal disclaimers that investors cannot extract a coherent investment thesis, or they produce marketing-heavy narratives that lack evidentiary rigor. Neither holds up.

The regulatory infrastructure around PPM private equity filings in India has tightened considerably. SEBI's April 2024 circular (SEBI/HO/AFD/SEC-1/P/CIR/2024/22) introduced a standardized reporting format for PPM Audit Reports applicable to all AIF categories. This was not a procedural update. It was a signal: SEBI is moving toward uniform compliance standards, and discretion in how you document your fund is narrowing.

Under Regulation 28 of the SEBI (AIF) Regulations, all AIFs must conduct an annual audit to ensure compliance with their PPM terms. Specifically:

When filing the draft PPM, the merchant banker must submit a due diligence certificate confirming the accuracy and sufficiency of all disclosures. A merchant banker who signs off on an incomplete or misleading PPM carries direct legal exposure.

This is where the execution model matters. S45's approach treats SEBI compliance not as a constraint to be cleared but as a structural framework built into the PPM from the first draft. Documents are designed to withstand audits, not scrambled to pass them.

There is no single prescribed format for a PPM, but every document used for private equity fund-raising in India must cover specific content areas. Gaps in any of these sections create liability exposure.

This section is where investor attention concentrates first. It must clearly articulate:

Every economic term must be defined and quantified. Vague terms like "competitive returns" or "market-rate fees" are not disclosures.

This is a factual description of the business model, operational history, competitive positioning, and the fund's investment thesis. The goal is not to convince investors to commit capital. The goal is to provide them with the information they need to make that decision independently.

Common failure point: founders allow marketing language to bleed into what should be evidentiary disclosure. Phrases like "market leader" or "best-in-class" without supporting data are claims, not disclosures, and unsubstantiated claims in a PPM create legal risk.

This is the most legally consequential section. Risk factors must be specific, material, and honest. A risk section listing only generic market risks is inadequate. It must include:

The principle is simple: if a reasonable investor would consider a fact important when deciding whether to invest, it belongs in the risk factors section.

Audited financials must be included along with a clear explanation of the methodology behind any forward-looking projections. Every number must show its math. Every projection must be linked to stated assumptions that can be tested against historical performance.

Broad categories like "working capital" or "growth initiatives" are insufficient. The use of proceeds section must specify allocation percentages, deployment timelines, and contingency provisions if proceeds fall short of the target.

Biographical disclosures for key management personnel must include professional history, relevant qualifications, any disciplinary history, and conflicts of interest. The governance section must describe the oversight structure, including board composition and any advisory relationships.

The single most common mistake Indian mid-market companies make when preparing a PPM for private equity is treating disclosure as a narrative exercise. Institutional investors evaluating a PPM are not reading for inspiration. They are reading for contradictions.

Every claim must be traceable to evidence. Every number must be verifiable. Every disclosure must be consistent with what appears in the financial statements, the management discussion, and the due diligence data room.

Firms that build this discipline into their PPM preparation process consistently face fewer investor queries, shorter due diligence cycles, and cleaner closes. Firms that do not spend months answering questions that a well-constructed document would have preempted.

The promise of AI in capital markets documentation is frequently overstated. Here is what operational AI actually does in the PPM drafting process, and what it does not do.

AI does not have the judgment to assess whether a disclosure is strategically positioned, whether a risk factor understates a real exposure, or whether the fund's investment thesis will survive scrutiny from a senior LP's investment committee.

S45 pairs proprietary AI systems with senior sector bankers for this reason. The AI compresses the workflow. The bankers ensure the output holds up. The combination brings mandate-to-document timelines from the traditional four-to-six-month range down to thirty to forty-five days without compromising disclosure quality or regulatory compliance. This is operational leverage, not automation theatre.

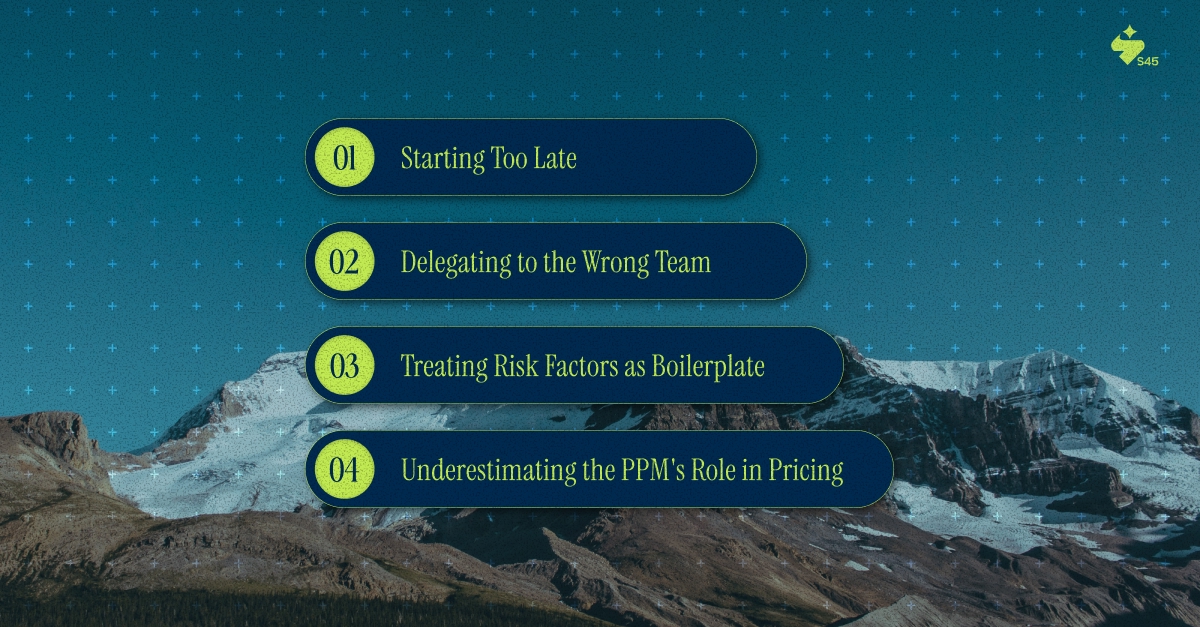

Having observed how Indian mid-market capital raises come together and fall apart, a few recurring failure patterns have been identified:

The PPM is not a document you prepare after a term sheet is signed. By that point, investors have already formed a view of the business, and material disclosures that surface during formal due diligence spark re-pricing conversations. Starting early gives you time to close documentation gaps before they become liabilities in negotiations.

Internal legal or finance teams rarely have the combination of regulatory knowledge, capital markets experience, and sector context needed to produce an institutional-grade document. The result is a document that is technically compliant but operationally weak: one that passes a first read but does not survive a serious due diligence process.

Copying risk factor language from a comparable company's PPM is dangerous. Risk factors must be specific to your business, your sector, and your fund structure. Boilerplate risk factors signal to sophisticated investors that the issuer has not thought carefully about what could go wrong, which raises questions about what else has not been thought through.

The way a company is disclosed in a PPM shapes how institutional investors model it. A document that presents a clear, evidence-linked picture of the business gives investors confidence to price the deal at the upper end of their range. A document with gaps and inconsistencies creates uncertainty, and investors price uncertainty with a discount.

In private equity, a PPM is a period during which capital is raised or lost before a single investor meeting. In India's regulatory environment, with SEBI tightening compliance standards and institutional investors raising their due diligence bar, the quality of your PPM is no longer a differentiator. It is a threshold requirement.

The companies that close private equity rounds efficiently are not the ones with the most compelling pitch decks. They are the ones whose documentation holds up: whose risk factors are specific, whose financials reconcile, and whose offering terms are unambiguous. That quality does not emerge from a last-minute drafting sprint. It comes from a structured, evidence-first preparation process built by people who understand what investors and regulators are actually looking for.

If you are evaluating a private equity raise and want to understand where your documentation stands before committing time and reputation to the process, connect with S45 for a capital structure consultation. The starting point is clarity, not a mandate.

Discover more insights on similar topics