April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You've built a real business. Revenue is compounding. Your early investors are patient, but not indefinitely so. The IPO is 18 to 36 months away, and somewhere in your cap table, there's a VC fund that's nine years into a ten-year mandate, quietly signaling it needs liquidity.

This is not a hypothetical. It's the reality for a significant number of Indian promoters and CFOs right now.

The venture capital secondary market sits at the intersection of private capital management, IPO preparation, and cap table governance. Most founders encounter it reactively, when an investor wants out before the listing. The operationally prepared ones understand it before the conversation starts.

The venture capital secondary market refers to transactions in which existing investors sell their stakes in private companies or venture funds to new buyers, rather than waiting for a primary liquidity event such as an IPO or acquisition.

This is a secondary sale of existing shares, not an issuance of new ones. No new capital enters the company. The transaction occurs between the selling investor and the incoming buyer.

Understanding how the venture capital secondary market works, who participates, what it costs, and how it affects your path to public markets is not optional for any Indian promoter or CFO serious about listing with institutional credibility.

Firms like S45 work with founders at exactly this inflexion point, where private liquidity decisions begin shaping the quality of the eventual IPO.

LP-Led Secondaries

A limited partner (LP) in a venture fund wants to exit its fund commitment before the fund's natural end. It sells its stake to a secondary buyer who steps into the LP's position and assumes rights to future distributions.

LP-led deals accounted for over half of secondary volume in 2024, particularly in older-vintage funds where returns had stalled. For Indian founders, this matters because it can change who sits on the other side of your cap table without any action on your part.

GP-Led Secondaries and Direct Secondaries

Here, the general partner (GP) of a fund creates a continuation vehicle to hold a specific high-performing asset longer, or an investor sells a direct stake in a portfolio company to another buyer.

The market for venture-backed tender offers has been gaining steam, and direct secondaries are increasingly structured either as stake transfers between VCs or as company-authorized tender programs for employees and investors.

Startups are staying private for a decade or more, while the venture capital model historically assumed 5 to 7 year holding periods. When that timeline extends, secondary markets emerge as the structural solution.

The private secondary market hit an all-time high of $152 billion in transaction volume in 2024, up nearly 39% from 2023.

India is not insulated from this trend. India's VC funding rebounded to approximately $13–14 billion in 2024, representing roughly a 1.4x increase from the 2023 trough, with investor confidence returning around sustainable unit economics and profitability. As funding volumes recover and companies mature, secondary activity will follow.

Suggested Read: 7 Top Venture Capital Firms in India in 2025

The venture capital secondary market is not an abstract institutional mechanism. For a promoter running a ₹200–800 Cr revenue business with two or three VC shareholders on the cap table, it has direct, practical implications.

When a secondary transaction occurs in your company, several things happen simultaneously:

SEBI's FVCI Amendment Regulations, effective January 2025, introduced significant changes to the registration and governance framework for foreign investors acquiring stakes in Indian unlisted companies, including tighter due diligence obligations through Designated Depository Participants.

None of this is unmanageable. But it requires your IPO preparation workflow to account for secondary transaction history, changes in investor classification, and disclosure traceability from day one.

Secondary transactions in the venture capital secondary market rarely occur at the last primary round valuation. Depending on market conditions, vintage pressure, and the company's trajectory, transactions can occur at discounts or, increasingly, at premiums.

For Indian founders, this creates a specific risk: if a secondary transaction happens at a discount to your last round, it resets the implied valuation narrative. When your investment banker begins pricing the IPO, that secondary trade becomes a data point that SEBI reviewers and institutional investors will reference.

This is why the sequence of secondary transactions, their timing relative to IPO filing, and the defensibility of any valuation differential must be prepared for with the same rigor as your financial disclosures.

A growing category of secondary activity involves employee equity, particularly for pre-IPO companies with mature ESOP pools.

When early employees or departing employees want to liquidate vested or unvested options, company-authorised tender offers have emerged as the primary mechanism. These are not informal transactions. They require board authorization, fair valuation, FEMA compliance for foreign employees or investors, and coordination with existing investors on right of first refusal (ROFR) provisions.

The right of first refusal is a provision that gives a company the right to approve or block future sales of equity shares and is typically invoked when an investor seeks to pursue a secondary sale.

For companies in IPO preparation, managing these employee liquidity requests poorly, without documentation, fair process, or consistent treatment, creates disclosure risk and potential SEBI queries on shareholder equity practices.

Must read: How to Apply for Venture Capital: A Comprehensive Guide

Understanding the process matters for founders who will need to approve, coordinate, or disclose these transactions.

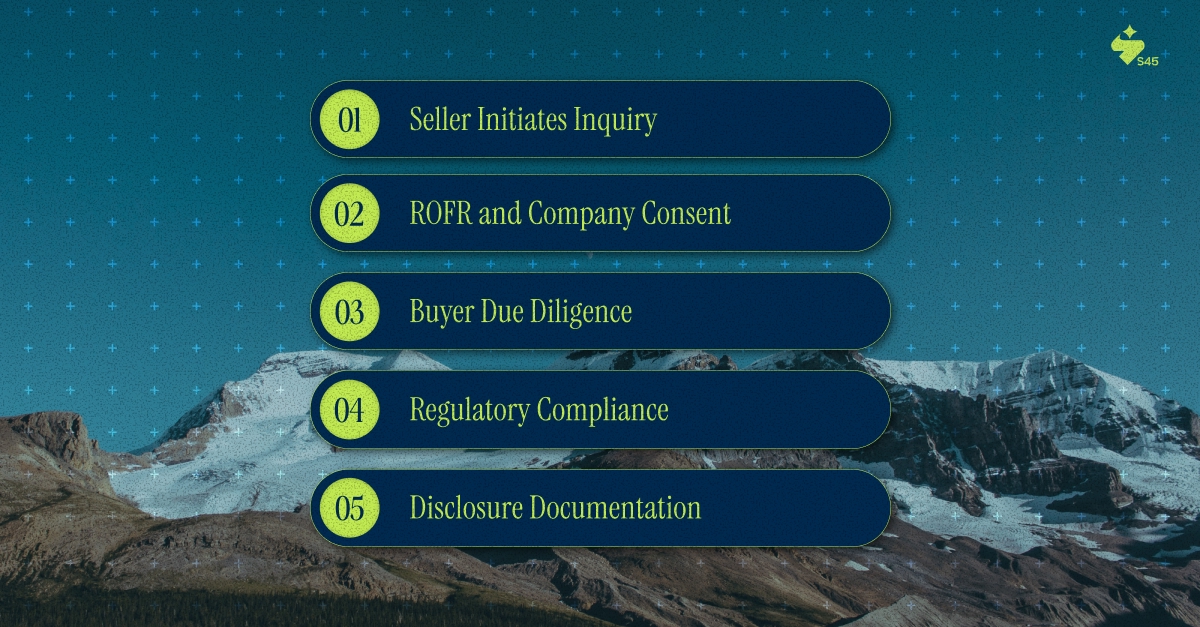

1. Seller Initiates Inquiry

The existing VC investor expresses intent to explore secondary sale, either independently or through a secondary broker. At this stage, most companies learn about a secondary transaction when it is already in progress.

2. ROFR and Company Consent

Most shareholder agreements contain ROFR clauses requiring the company and/or other investors to be offered the stake first. This is your operational control point. Responding without legal and financial clarity at this stage is a common error.

3. Buyer Due Diligence

The incoming secondary buyer will conduct diligence on the company, including reviewing financials, governance documents, and cap table structure. This is not a light process. Secondary buyers at an institutional scale run the same diligence rigor as primary investors.

4. Regulatory Compliance

Depending on buyer classification (domestic, FPI, FVCI), applicable FEMA rules, pricing guidelines, and reporting requirements apply. For foreign buyers, the amended FVCI framework governs registration and ongoing compliance.

5. Disclosure Documentation

Any secondary transaction that occurs between 18 and 24 months before the IPO filing will be disclosed in the DRHP. The pricing, buyer identity, and rationale for any valuation differential from the last primary round must be defensible under SEBI scrutiny.

This is where the venture capital secondary market becomes directly relevant to the IPO execution framework that serious Indian enterprises need to understand.

SEBI reviewers do not assess IPO pricing in isolation. They examine the full history of capital raises, secondary transactions, and any changes in company valuation. A secondary trade at a steep discount two years before your IPO filing requires explanation, not concealment.

The institutional discipline required is straightforward: every transaction in your capital history must be traceable, evidence-linked, and defensible. Not because regulators demand a story, but because the absence of evidence invites questions that delay listings.

Realizing private value at the right time, price, and structure is increasingly complex, and as GPs face growing pressure to deliver DPI, secondaries have become a core portfolio management tool.

For Indian promoters, this means your cap table at the time of DRHP filing will likely include investors who entered through secondary routes, not just original primary rounds. Each of these investors has different lock-in obligations, classification requirements under SEBI ICDR, and disclosure obligations.

Cleaning this up after the mandate is signed is expensive and time-consuming. Building it into IPO readiness planning from the outset is the institutional approach.

Firms like S45 approach this as an execution problem rather than a documentation formality. The IPO Readiness Scan conducted before mandate signing specifically maps secondary transaction history, investor classification, and cap table governance risks that will surface during DRHP drafting.

Under SEBI ICDR, promoter shareholders are subject to a minimum three-year lock-in on a portion of their holdings post-listing. Non-promoter pre-IPO shareholders face a one-year lock-in.

When secondary transactions occur shortly before an IPO, the incoming buyer is classified as a promoter or non-promoter. And the timing of their acquisition directly affects the lock-in structure and the free-float calculation that institutional investors will scrutinise during pricing.

Getting this wrong is not a minor error. It triggers SEBI queries, delays listing timelines, and can require cap table restructuring during the most operationally intense period of the IPO process.

Several patterns repeat across Indian high-growth companies approaching public markets.

Treating secondary activity as a private matter

Secondary transactions in your company are not confidential events that disappear before listing. They become part of your shareholder history and DRHP disclosures. Every rupee traded, at every valuation, with every investor, is institutional evidence.

Allowing secondary transactions without investment banker coordination

A VC secondary trade that occurs without reference to your planned IPO timeline, pricing strategy, or cap table governance framework can create contradictions that take months to resolve with SEBI.

Confusing secondary discounts with company distress

A secondary transaction at a discount does not necessarily signal weak fundamentals. But without a clear, evidence-linked explanation for the valuation differential, institutional investors and SEBI reviewers will draw their own conclusions.

Not building secondary transaction history into DRHP preparation

Many companies begin drafting a DRHP without a complete, documented history of secondary transactions. When this surfaces mid-process, it becomes a workflow crisis.

In India's VC landscape, secondary sales played an even bigger role than IPOs in driving exits in 2023–24, as late-stage funds and sovereign investors bought stakes from early backers without the startups going public.

This is not a temporary anomaly. As Indian companies stay private longer, as VC fund vintages age, and as institutional LP pressure for liquidity increases, the venture capital secondary market will become a standard feature of the pre-IPO capital stack for most high-growth Indian enterprises.

India's startup ecosystem is demonstrating greater maturity, particularly through IPOs and M&A, offering enhanced exit opportunities for investors.

The implication is clear. Indian founders and CFOs who understand the mechanics of secondary transactions, their regulatory implications under SEBI, and their interaction with IPO pricing and cap table governance are structurally better prepared for public markets than those who encounter them unprepared.

The venture capital secondary market is neither a threat to founders nor a distress mechanism for failing companies. It is a structural feature of mature private capital ecosystems, and India's private markets are now mature enough that avoiding the subject is no longer an option.

For Indian promoters running high-growth enterprises with revenue between ₹80 Cr and ₹800 Cr, backed by institutional VC shareholders and IPO ambitions, the operational questions are specific. Who on your cap table is approaching fund maturity? Have recent secondary transactions been documented, priced defensibly, and structured with SEBI disclosure requirements in mind? Does your IPO preparation workflow account for the full shareholder history, including secondary entries?

Execution discipline on these questions is not a legal formality. It is the foundation of institutional-quality IPO preparation.

If you are at this stage, and the questions above do not yet have clean answers, the time to build that clarity is before the mandate, not during DRHP drafting.

Connect with S45 for a capital markets conversation before the questions become complications.

Discover more insights on similar topics