April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Key Takeaways

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

You’ve built a ₹50 crore business with strong margins and diversified customers, yet scaling to ₹200 crore without dilution feels risky and unclear.

The problem isn’t access to capital, it’s choosing debt that won’t trigger SEBI red flags or complicate IPO disclosures.

This guide explains 15+ institutional debt options that align with IPO timelines, helping you raise capital without weakening your public-market readiness.

Debt financing means borrowing capital that you repay over a fixed period with interest. Unlike equity, it does not dilute ownership or board control. You retain decision-making authority while using external capital to fund growth, working capital, or asset expansion.

The lender earns predictable returns through interest and scheduled repayments. You retain strategic control.

Indian promoters increasingly choose debt over equity for four practical reasons:

However, not all debt supports an IPO journey.

Some facilities include restrictive covenants, promoter guarantees, or cross-default clauses that create red flags during SEBI reviews. Others complicate disclosures under ICDR regulations or weaken your governance narrative.

That’s why timing and structure matter.

S45 helps founders design debt structures aligned with IPO milestones. We evaluate how each loan impacts disclosures, related-party reporting, and promoter obligations, ensuring your capital stack strengthens, not delays, your public listing.

Also Read: Debt vs Equity Financing: A Complete Guide for Indian MSME Founders

Now, let’s explore specific debt sources available and when to use each one.

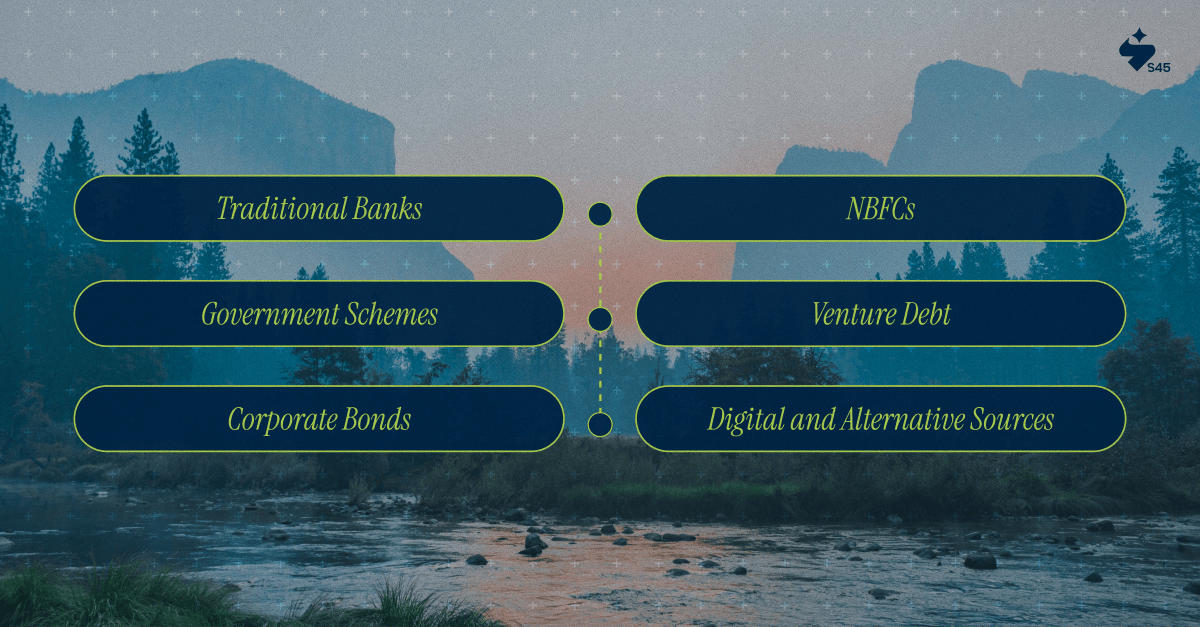

Indian entrepreneurs have access to multiple institutional debt channels. Each source offers distinct advantages in terms of interest rates, approval speed, and IPO compatibility. The key is matching the right source to your capital need and listing timeline.

Scheduled commercial banks offer the lowest rates, longest tenures, and strongest regulatory credibility. They also impose strict documentation requirements and credit evaluation processes.

S45 structures banking relationships 18-24 months pre-IPO to establish debt servicing history. Our DRHP drafting ensures every security interest and covenant appears correctly in disclosure schedules.

NBFCs approve faster than banks, taking 7-15 days versus 30-45 days. They handle smaller ticket sizes with more flexible documentation. But interest rates run 200-400 basis points higher.

Use NBFCs strategically for time-sensitive opportunities where bank approval timelines would cause you to miss growth windows. Disclose these higher-cost facilities transparently in your DRHP. Institutional investors will ask why you chose NBFCs over banks.

Government schemes and DFIs offer the most favorable terms. Lower interest, longer tenures, and softer collateral requirements. They also signal institutional credibility because government backing implies rigorous evaluation.

Government-backed debt strengthens your ESG narrative and policy alignment story. Include these prominently in your DRHP's sustainability sections.

Venture debt serves high-growth companies between funding rounds. It's subordinated debt carrying 14-18% interest plus warrants. Ticket sizes range from ₹5-50 crore with 2-4 year tenures.

Venture debt funds understand public market timelines. They often structure facilities to repay or convert before listing. But disclose warrant terms carefully. If warrants grant equity participation at below-market prices, explain the timing and rationale clearly.

Once you cross ₹500 crore revenue or achieve a strong credit rating, you access bond markets directly. This diversifies funding sources and often reduces borrowing costs.

Corporate bond history demonstrates capital market sophistication. If you've serviced NCDs for 18-24 months pre-IPO, institutional investors interpret this as rehearsal for public equity markets.

Digital platforms like Lendingkart or Capital Float offer 24-48 hour approvals for ₹1-50 lakh at 18-30% interest. They underwrite using GST returns, bank statements, and digital payment patterns.

Speed is the advantage. But high interest rates make these suitable only for short-term needs or quick payback opportunities.

Supply chain financing leverages buyer-supplier relationships. Platforms like TReDS let you discount invoices at 10-15% annually when large corporate buyers guarantee payment.

Use alternative sources tactically for timing mismatches. But build core debt relationships with scheduled banks or DFIs. Institutional investors view heavy reliance on digital lenders as a signal of limited bank access.

Also Read: Debt vs Equity Financing: Which Is Best for Your Business?

Debt timing isn't just about when you need capital. It's about sequencing facilities to build credible track records and avoid covenant conflicts during listing.

Below is how experienced founders sequence borrowing as they move toward a public listing.

This phase is for building visible, durable value.

Why this window matters

What to do

Outcome

This phase supports valuation acceleration, not structural expansion.

Why this window matters

What to use

Key safeguards

Outcome: Stronger growth narrative without long-term balance sheet risk

This is the execution and compliance phase.

Why restraint matters

What to do

Best practices

Every debt decision before an IPO should answer one question: Does this strengthen my listing story or complicate it?

Well-timed debt builds institutional confidence. Poorly timed debt creates avoidable friction. This is where a strategic partner can help you.

Most merchant bankers focus on the listing event. True IPO readiness starts 18–24 months earlier, when capital structure and financial discipline are set.

S45 works differently. We pair sector bankers with proprietary AI that tracks how every debt decision flows into your DRHP. Each facility is modeled for its 24-month impact on promoter contribution, leverage, and interest coverage.

For debt-financed growth specifically, S45 helps you answer three critical investor questions:

Ready to structure debt facilities for IPO success? S45's IPO Readiness Scan evaluates your current debt profile and creates a 12-24 month roadmap linking every borrowing decision to DRHP requirements. Connect with us to begin your journey with partners who've closed 30+ Main Board and SME Exchange listings.

Discover more insights on similar topics