April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making crucial business decisions.

Your CFO has run the numbers. The board is asking about dilution. You have sat through three pitch decks promising "strategic value" alongside capital. And somewhere in the back of your mind, you are calculating how much of your enterprise you will still own by the time the PE firm exits.

This is not a moment of excitement. This is a moment of reckoning.

For Indian promoters running ₹80–800 Cr revenue enterprises, the choice usually boils down to a fundamental audit of private equity advantages and disadvantages.

The question is: How do I access growth capital without losing control, credibility, or speed?

The answer PE firms offer: Give us 25–40% equity, relinquish board control, align with our 5–7-year exit timeline, and accept operational restructuring that may conflict with legacy priorities.

The question you should be asking: Can I access public markets directly, retain control, and compress execution timelines using institutional-grade infrastructure?

That is the chaos gap. And it is solvable.

Most Indian enterprises do not fail because they lack growth potential. They fail to access optimal capital structures because they lack institutional clarity on execution pathways.

The conversation about the advantages and disadvantages of private equity is dominated by investor-side narratives. Returns, diversification, and portfolio construction are all valid for LPs deploying capital. But for Indian promoters, the calculus is different.

When you accept PE funding, you are not just raising capital. You are:

According to Bain & Company's India Private Equity Report 2025, PE-VC investments in India reached $43 billion in 2024, rebounding 9% year-over-year. Buyouts accounted for 51% of total PE deal value. This is not a market discovering new growth companies. This is a market extracting value from mature enterprises that could have accessed public markets directly.

The chaos gap exists because:

This is where S45 enters, not as another advisor, but as an AI-native investment bank that owns IPO outcomes from readiness → DRHP → listing → liquidity design.

S45 pairs seasoned sector bankers with proprietary AI systems to compress IPO timelines from 4–6 months to 30–45 days (mandate to DRHP). This is not faster execution through shortcuts. This is institutional clarity replacing chaos.

Private equity firms raise capital from institutional investors (LPs), deploy it into mature businesses, implement operational changes to increase valuation, and exit within 5–7 years through secondary sales, strategic buyouts, or IPOs.

For Indian enterprises, PE typically means:

India's PE market is projected to grow at a 18.22% CAGR, reaching $232.7 billion by 2030, driven by sectoral rotation into healthcare, renewables, and deep tech. But this growth reflects LP appetite for returns, not enterprise suitability for PE structures.

The question is not whether PE is large. The question is whether it is right for your enterprise.

While Private Equity (PE) is often a middleman for companies ready to go public, its value proposition is built on four distinct pillars. For an Indian promoter, these benefits must be weighed not only as capital but also as a strategic trade-off.

PE provides growth capital without the transparency requirements of public listings. For enterprises with complex ownership structures, legacy issues, or regulatory gaps, this privacy can feel liberating.

But privacy is not the same as preparedness. If your enterprise cannot withstand SEBI ICDR scrutiny, the issue is not market readiness; it is institutional discipline. And PE funding does not solve that. It delays the reckoning.

PE firms bring sector knowledge, portfolio company playbooks, and operational leverage. They can introduce performance metrics, governance frameworks, and talent pipelines that Indian mid-market companies often lack.

This is valuable if your enterprise has structural capability gaps. It is extractive if your enterprise simply lacks execution infrastructure to access public markets.

Unlike bank debt with fixed repayment schedules, PE capital does not require monthly servicing. This frees up cash flow for reinvestment.

But "patient" is relative. PE funds operate on 7–10 year cycles. Your exit timeline is not patient; it is predetermined. And when market conditions do not align with fund timelines, you exit anyway, often at suboptimal valuations.

A Tier-1 PE firm on your cap table signals institutional validation. This can unlock follow-on funding, commercial partnerships, and talent acquisition.

But this only matters if you plan multiple funding rounds. If your goal is public market access, PE is a detour, not a validation step.

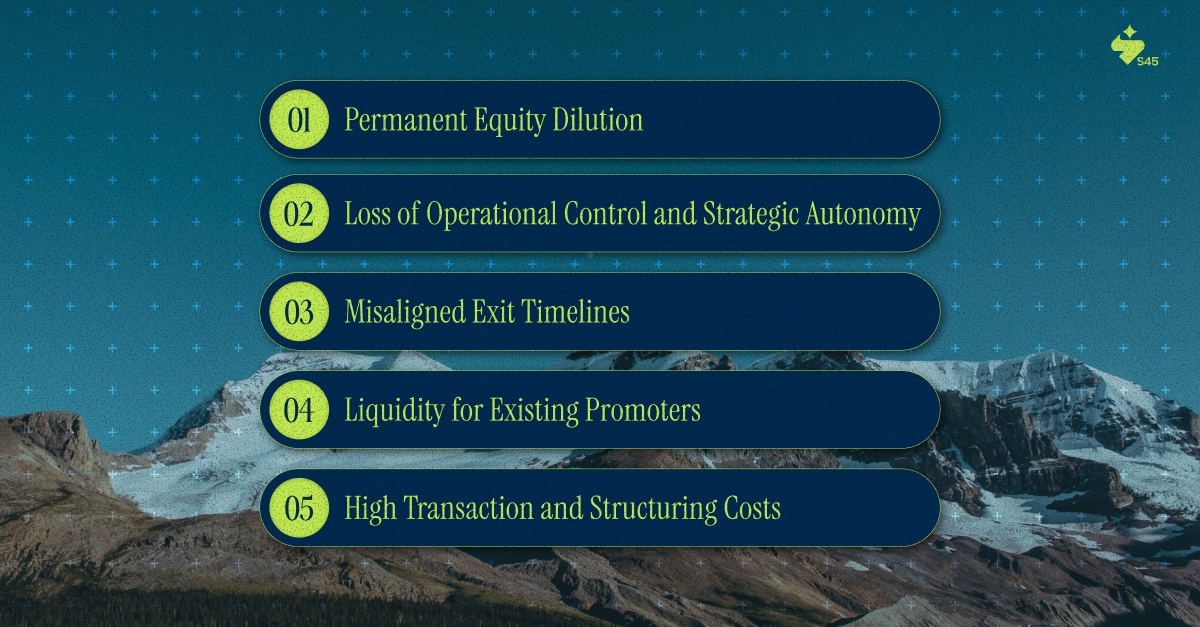

The advantages of private equity are marketed aggressively; the structural costs are usually discovered in year three. For a ₹200–800 Cr enterprise, these "disadvantages" often manifest as a loss of the very agility that built the business.

Unlike debt, equity never returns. When you sell 30% to a PE firm, you have permanently reduced your ownership. And if subsequent funding rounds occur (which PE firms often push), dilution compounds.

For legacy-driven Indian promoters, this is not just a financial issue. It is emotional. You built the enterprise. PE firms rent influence for 5–7 years and exit with multiples. You stay, with less control and less upside.

PE firms do not invest passively. They demand board seats, veto rights on key decisions, and quarterly performance reviews tied to pre-agreed metrics.

This may improve governance. It may also conflict with founder instincts, legacy priorities, and long-term vision. And when conflicts arise, the PE firm's fiduciary duty is to its LPs, not to your enterprise's legacy.

PE funds have finite lives. Whether your enterprise is ready or not, they exit within 5–7 years. If public markets are volatile, they push secondary sales. If your sector is out of favor, they restructure and exit anyway.

Your timeline is not considered. Their IRR targets are.

When a PE firm acquires a stake, your shares become less liquid. You cannot easily sell. You cannot easily dilute them. You are locked into their exit timeline, with limited optionality.

PE deals involve extensive due diligence, legal structuring, and advisory fees. These costs are often borne by the enterprise, reducing net capital received.

And if the deal does not close (which happens frequently), you have spent months and fees with nothing to show.

Numbers clarify what narratives obscure.

According to Bain's research, exit activity in India surged to $33 billion in 2024, up 16% year over year. Public market exits comprised 59% of total exit value, driven by IPO activity and block trades.

This is critical: PE firms are using IPOs to exit. They are not using IPOs to build.

When a PE-backed company lists, the PE firm is selling, not holding. The public market absorbs their exit, often at valuations inflated by pre-IPO rounds. Retail investors buy the narrative. PE firms collect multiples.

Meanwhile, enterprises that could have listed directly paid in equity dilution, time, and control.

Private equity investments in India reached $15 billion in 2024, up 46.2% from 2023. Healthcare, pharma, consumer, and technology-led deal activity. But these are mature sectors with proven business models, exactly the sectors that could access public markets through institutional IPO execution.

The data does not suggest PE is the only path. It suggests PE is the marketed path. For most Indian enterprises, it is the more expensive path.

The advantages and disadvantages of private equity matter less when you understand that IPO readiness is an execution problem, not a capital problem.

Most Indian enterprises delay IPO not because they are unready, but because they lack institutional infrastructure to compress workflows, evidence disclosures, and regulatory drafting.

S45's IPO Readiness Scan identifies these gaps. Not conceptually. Operationally.

AI-driven DRHP drafting compresses regulatory documentation from 4–6 months to 30–45 days. Every disclosure is evidence-linked. Every claim is traceable. Every section references source documents that SEBI can verify instantly.

This is not automation for speed. This is institutional clarity replacing manual chaos.

Capital market execution, whether Main Board or SME Exchange, becomes a workflow, not a negotiation. Pricing is transparent. Liquidity design is explicit. Exit timelines align with market conditions, not fund cycles.

And you retain control. Full board autonomy. No dilution beyond what public markets price transparently. No misaligned exit pressures.

This is not anti-PE. This is pro-clarity.

If your enterprise has structural capability gaps, fragmented operations, governance deficits, or talent shortages, PE may be the right answer. But if your enterprise simply lacks IPO execution infrastructure, PE is an expensive detour.

Private equity advantages and disadvantages become irrelevant if your enterprise cannot demonstrate SEBI ICDR and LODR compliance with institutional precision.

PE firms tolerate regulatory gaps because they plan to fix them before exit. But fixing compliance post-funding is more expensive, time-consuming, and more disruptive than building compliance-native operations from day one.

SEBI does not negotiate. DRHP comments are not suggestions. Every disclosure gap extends your timeline. Every evidence failure triggers re-submission cycles.

S45 treats SEBI compliance as craftsmanship. Not as friction. Not as a checklist completion. As the structural foundation of institutional credibility.

When DRHP drafting is AI-driven and evidence-linked, SEBI comments reduce by 60–80%. Review cycles compress. Approval timelines become predictable.

This is not regulatory arbitrage. This is regulatory precision.

And it fundamentally changes the capital structure decision. When IPO execution is no longer uncertain, PE becomes optional rather than inevitable.

Not every enterprise should avoid private equity. But every enterprise should understand when PE is the optimal capital structure, and when it is default advice masquerading as strategy.

PE makes sense when:

PE does not make sense when:

For most Indian enterprises in the ₹80–800 Cr revenue range, PE is the latter. And the alternative is not bank debt. The alternative is institutional IPO execution.

The private equity advantages-and-disadvantages framework is incomplete without acknowledging the third path: institutional IPO execution that eliminates the chaos gap.

PE firms market optionality. But optionality for whom? For LPs seeking portfolio diversification and IRR targets. Not for promoters seeking capital markets access without permanent dilution.

Indian enterprises deserve better than a binary choice between expensive equity dilution and restrictive debt. They deserve execution clarity.

S45 provides that clarity. Not through advisory recommendations. Through outcome ownership.

From IPO readiness scans that identify operational gaps, to AI-driven DRHP drafting that compresses regulatory timelines, to capital market execution that treats SEBI compliance as craftsmanship, S45 replaces chaos with institutional precision.

Don't solve an execution problem with an equity solution. Consult an S45 partner to bridge your chaos gap and verify your direct path to the public markets.

Discover more insights on similar topics