April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making crucial business decisions.

The email arrives at 11 PM. Your PE fund's compliance team needs updated ESG metrics for the quarterly LP report. Different format than last quarter. The data they're requesting isn't available in your systems because no one mapped LP sustainability requirements to the operational infrastructure at the time of the investment close.

Meanwhile, your CFO is three weeks into DRHP preparation. The merchant banker flagged 47 sustainability disclosure gaps that SEBI will question. Water consumption data exists, but isn't certified. Board diversity metrics look adequate until compared against SEBI's BRSR Core benchmarks.

This is where most Indian enterprises discover that ESG integration isn't a sustainability initiative. It's the capital markets infrastructure that either exists before exit conversations begin or incurs months of remediation when institutional investors start diligence.

Private equity and ESG integration have moved beyond compliance checkbox exercises into institutional readiness infrastructure. Sustainability disclosure gaps delay listings, trigger SEBI comment cycles, and signal governance weakness to institutional investors who determine IPO outcomes.

Most PE firms identify ESG integration gaps during exit preparation, not during portfolio monitoring. The pattern repeats across mid-market deals: LP commitments at fund formation reference international frameworks (TCFD, SASB, GRI), portfolio companies operate under Indian regulatory structures (Companies Act CSR provisions, Environmental Protection Act compliance, state pollution board requirements), and nobody maps these systems together until merchant bankers start DRHP drafting.

When exit conversations begin, founders discover that their sustainability documentation doesn't align with institutional investor requirements or public market disclosure standards. This isn't a failure of intent. It's a workflow problem disguised as a sustainability challenge.

The typical failure pattern: ESG due diligence occurs separately from operational assessment. Portfolio companies implement generic sustainability programmes disconnected from material business risks. Ad hoc reporting to LPs uses metrics that don't align with India-specific requirements.

Exit preparation reveals sustainability data that isn't traceable, evidenced, or listing-ready. AI-native investment banks like S45 address this by treating ESG gap analysis as an integrated IPO readiness assessment, identifying sustainability deficiencies that could trigger SEBI comments before timelines are delayed. The approach maps LP ESG commitments to regulatory disclosure requirements systematically, not reactively.

Result without this infrastructure: delays, expensive remediation, diluted narratives.

The workflow failures in traditional ESG integration stem from a deeper issue: most firms still treat sustainability as a qualitative narrative rather than quantifiable operational data. This creates a disconnect between what LP reports promise and what SEBI DRHP disclosures can substantiate.

The institutional shift in private equity ESG investing centres on one principle: materiality determines measurement.

Sustainable private equity firms no longer treat ESG as a universal checklist applied uniformly across portfolios. Instead, they identify sustainability factors that directly impact financial performance, operational resilience, and regulatory exposure within specific sectors and geographies.

For Indian enterprises, this means:

Research on Indian ESG investment performance shows varying impacts across pillars: governance and environmental factors show measurable correlations with financial outcomes, whilst social metrics require sector-specific interpretation.

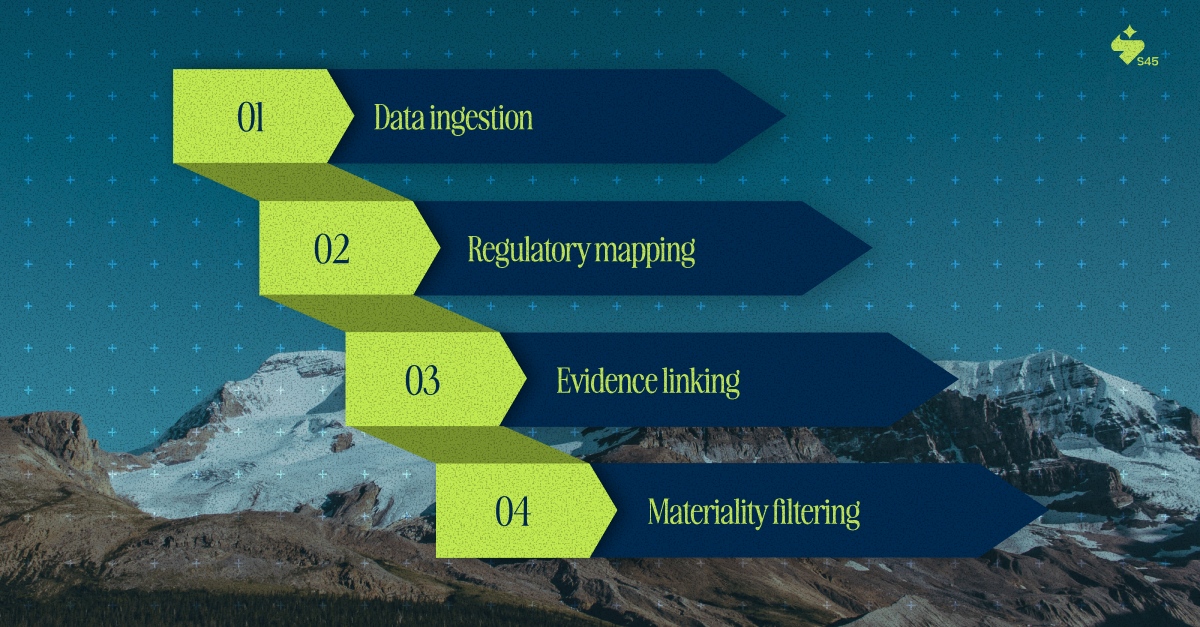

AI-native investment banks mapping sustainability disclosures to regulatory requirements don't generate generic ESG statements. They map company-specific sustainability performance against SEBI expectations, investor concerns, and sector benchmarks, and link each claim to documentary evidence.

The execution model treats materiality assessment as the foundation, not an afterthought.

Understanding materiality matters because India's regulatory requirements have evolved faster than most PE firms anticipated. The shift from voluntary sustainability reporting to mandatory, assured ESG disclosure fundamentally changes how enterprises must approach public market preparation.

India's regulatory evolution on sustainability disclosure has moved faster than most enterprises recognise. SEBI's BRSR Core framework, introduced with mandatory implementation timelines phased from FY 2023-24 onwards, represents a fundamental shift in how listed entities approach ESG accountability.

The framework mandates:

For enterprises preparing for an IPO, this creates a specific challenge: sustainability reporting infrastructure must be operational before listing, not built afterwards.

PE-backed companies face additional complexity. Their ESG frameworks must satisfy both SEBI's disclosure requirements and LP reporting commitments, often structured around global standards that don't perfectly align with India-specific regulations.

Advanced capital markets execution treats this alignment as drafting precision, not compliance burden. Institutional-grade DRHP preparation maintains updated mappings between SEBI BRSR metrics, international ESG frameworks, and sector-specific materiality factors.

When preparing sustainability disclosures, the approach ensures claims are evidenced (every ESG metric links to source documentation), compliant (disclosures meet BRSR Core requirements without over-disclosure), and material (focus remains on sustainability factors that impact business performance).

This isn't sustainability reporting. This is institutional-quality disclosure that treats SEBI requirements as minimum standards, not ceiling objectives.

The regulatory framework sets the floor. Limited partner expectations set the ceiling. Between these two benchmarks, PE-backed enterprises must navigate sustainability requirements that compound rather than align.

This isn't ethical investing divorced from returns. LPs have observed that ESG-integrated portfolios demonstrate superior risk-adjusted performance. The mechanism is straightforward: systematic sustainability assessment identifies operational inefficiencies, governance weaknesses, and reputational exposures that traditional due diligence misses.

For Indian enterprises seeking PE capital, this translates into specific implications:

The structural implication for capital markets preparation: ESG integration cannot be an exit-stage consideration. It must be embedded in operational infrastructure from PE entry onwards.

The gap between LP expectations and operational capacity creates the core challenge. Most mid-market Indian enterprises lack dedicated sustainability teams. ESG data exists in a fragmented across departments, geographies, and filing systems. Traditional approaches to consolidating this information rely on consultant-led manual processes that consume months.

The sustainability data challenge in private equity stems from volume, variability, and verification requirements. Portfolio companies operate across diverse geographies and sectors. LPs demand standardised metrics. SEBI requires India-specific disclosures. International frameworks impose additional reporting layers.

Manual ESG data management struggles to keep up with this complexity. AI addresses this through systematic data structuring:

This operational leverage compresses timelines. Traditional ESG disclosure preparation for IPO documents requires 2-3 months. AI-native platforms reduce this to weeks through eliminating manual correlation work.

The critical distinction: AI accelerates evidence organisation and regulatory mapping. It doesn't replace the judgment required to determine ESG materiality, assess sustainability risks, or craft disclosure narratives that institutional investors find credible.

Technology solves the data consolidation problem. Strategy determines which data matters. The distinction separates institutional ESG integration from compliance theatre.

The sophistication gap in private equity and sustainability integration appears most clearly in how firms define "ESG strategy." Immature approaches treat sustainability as carbon accounting plus diversity statistics, measuring emissions and gender ratios without operational changes or value creation. Institutionally rigorous ESG private equity firms structure sustainability around three principles:

Not all ESG factors matter equally across sectors. Water intensity drives value in beverage manufacturing; it's irrelevant in software services. Effective ESG strategies identify the 5-7 sustainability factors that genuinely influence operational performance, regulatory risk, and stakeholder relations, then build measurement systems around those factors exclusively.

Sustainability metrics should emerge from operational systems, not parallel reporting infrastructure. Best-practice portfolio companies embed ESG metrics into existing management dashboards, operational reviews, and performance incentives.

Institutional investors distinguish between disclosed ESG commitments and evidenced ESG performance. SEBI's BRSR Core framework, with mandatory independent assurance, acknowledges that sustainability reporting without verification can enable greenwashing. PE firms applying similar rigour to portfolio ESG monitoring create verifiable value creation narratives that translate directly into exit premiums.

Strategic principles matter, but execution occurs within specific regulatory environments. For PE-backed Indian enterprises, the sustainability compliance landscape operates across multiple layers.

India’s sustainability regulatory framework has accelerated faster than many expected. Beyond SEBI’s BRSR mandates for listed companies, enterprises must navigate Companies Act CSR provisions (2% of average net profits), Environmental Protection Act enforcement through state pollution boards, state-level labour laws, and RBI’s green finance frameworks.

For PE-backed enterprises preparing for public markets, this creates a clear challenge. Sustainability frameworks designed for global PE funds do not map cleanly to India-specific regulatory structures. International ESG questionnaires rarely align with SEBI BRSR Core’s quantified requirements on employee welfare, community impact, and responsible business conduct.

Institutional capital markets execution, therefore, requires India-focused ESG knowledge bases that reflect actual regulatory requirements and investor expectations, not generic frameworks adapted post-facto. Execution platforms like S45 maintain sector-specific mappings between SEBI requirements and operational sustainability metrics, ensuring DRHP disclosures reflect Indian regulatory reality rather than international templates.

Regulatory complexity and LP requirements create the context. Operational decisions determine outcomes. For enterprises that have raised institutional capital with public-market exits in view, three execution principles are critical.

If your enterprise has raised institutional capital and a listing represents your likely exit path, three operational imperatives matter:

Sustainability gaps identified during IPO readiness cost exponentially more to remediate than ESG frameworks built during PE ownership. Water permits, waste management licenses, labour compliance audits, and board independence structures all require months to establish properly. Waiting until pre-IPO preparation guarantees timeline delays or disclosure compromises.

Your ESG reporting should serve three audiences simultaneously: PE fund LPs (quarterly updates), SEBI (BRSR disclosures), and IPO investors (DRHP sustainability sections). Unified sustainability infrastructure, embedded in operational systems rather than maintained separately, enables efficient reporting across all stakeholder requirements.

Every ESG claim in offering documents is subject to institutional investor scrutiny. Qualitative sustainability statements without quantified improvement metrics signal weak governance. Metrics without documentary evidence indicate potential misrepresentation. The institutional standard: measurable improvement in material ESG factors, evidenced through operational data, verified through independent assessment, disclosed transparently.

Capital markets execution demands more than ESG awareness. It requires institutional clarity, sequencing, and defensible disclosures that withstand regulatory and investor scrutiny. In practice, this translates into a few defining execution characteristics:

Private equity and ESG integration have evolved from an optional sustainability initiative into a mandatory capital markets infrastructure. For Indian enterprises navigating the path from PE ownership to public listing, sustainability disclosure gaps identified during exit preparation cost months of remediation and signal governance weaknesses to institutional investors who determine listing success.

The operational reality: ESG frameworks must satisfy the combined scrutiny of LP reporting cycles, SEBI BRSR mandates, and institutional investor diligence. Evidence-linked sustainability performance, mapped systematically to regulatory requirements, compresses these risks into manageable execution timelines. Firms that treat ESG integration as exit infrastructure control their listing timelines. Those who don't spend months explaining gaps to SEBI.

Before committing to IPO timelines, assess whether your sustainability infrastructure can withstand institutional scrutiny. S45's IPO Readiness Scan identifies ESG gaps that could delay listings without compromising outcomes.

Discover more insights on similar topics