February 23, 202612 min read

How to Get Funding Help for Startups: Beyond VC Rounds to Public Markets

By Abhishek Bhanushali

Startup Funding

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

If you've raised private equity rounds, managed debt covenants, or navigated term sheet negotiations, you already understand funding strategies. But the moment you begin IPO preparation, you discover where traditional funding approaches break.

The issue isn't capital availability. Indian enterprises in the ₹80–800 Cr revenue range rarely struggle to access growth capital. The breakdown occurs when historical funding structures must translate into SEBI-compliant disclosure frameworks. Every convertible note becomes a related-party transaction requiring explanation. Every debt covenant constitutes a material contract and requires evidence of board ratification. Every previous valuation round becomes a benchmark against which your IPO pricing will be scrutinized.

Most promoters discover these complexities after engaging merchant bankers. By then, the funding strategy, built over years of private capital rounds, will need to be reconstructed to meet institutional standards. This reconstruction adds 4–6 months to IPO timelines, assuming no regulatory queries.

The chaos isn't about what capital you raised. It's about whether that capital structure can withstand public market scrutiny without a material restatement.

S45 is an AI-native investment bank built to bridge the operational gap between private capital governance and public market execution. The firm pairs experienced sector bankers with proprietary AI systems that audit, reconstruct, and evidence-link funding histories before SEBI review begins.

This isn't advisory. It's institutional execution, the kind that treats your historical funding strategy as discoverable evidence, not promotional narrative.

When S45's IPO readiness analysis examines your capital structure, the focus centres on three requirements:

The funding strategy that worked brilliantly in private markets often creates disclosure complexity in public markets. Identifying these complexities before they become regulatory objections separates smooth IPO executions from delayed ones.

Indian mid-market enterprises typically pursue funding strategies optimized for growth velocity, not institutional transparency. This creates predictable friction during IPO preparation:

Many promoters begin with friends-and-family capital, director loans, or unsecured advances. These arrangements work effectively in private operations but require formal documentation and arm's-length validation for public market disclosure. The absence of proper agreements creates "unexplained funding" issues that SEBI queries extensively.

Your seed round valued the company using a discounted cash flow model. Your Series A was priced at comparable trading multiples. Your pre-IPO round used revenue multiples. Each methodology makes sense on its own, but together they suggest valuation inconsistencies that institutional investors question. The funding plan must demonstrate valuation progression logic, not just valuation growth.

You raised capital for "working capital requirements and general corporate purposes." This phrasing works in term sheets but fails in SEBI disclosures, which require specific deployment evidence: what percentage of the inventory expansion was funded, what percentage of debt was reduced, and what percentage of capital expenditure was funded. If deployment evidence is missing, reconstruction from historical financials is necessary.

Multiple funding rounds often create layered shareholding, holding companies, trusts, and nominee structures. While legally valid, these structures complicate disclosure requirements and sometimes trigger consolidation questions. Simplification before DRHP filing accelerates regulatory approval.

The fundamental tension: funding strategies optimized for operational flexibility create documentation gaps that public markets interpret as governance weakness.

Enterprises preparing for Main Board or SME Exchange listings must demonstrate capital discipline well before IPO filing. Regulators and institutional investors assess not just capital raised, but the intent, structure, and governance behind it.

Many promoters view debt negatively, something to minimize or eliminate before IPO. This misunderstands institutional capital structure.

Well-structured debt demonstrates operational maturity. Banking relationships evidenced through term loans, working capital facilities, and letter-of-credit arrangements show that institutional lenders have conducted their own due diligence and found your business creditworthy. This third-party validation strengthens IPO positioning.

The key distinction: debt raised for strategic purposes (capacity expansion, acquisition financing, inventory build-up) strengthens your IPO narrative. Debt raised to cover operating losses or fund promoter withdrawals creates disclosure complications.

Institutional capital market execution includes debt structure assessment as part of IPO readiness. If your current debt profile creates covenant restrictions that limit post-listing flexibility, these issues must be addressed before DRHP drafting begins. Waiting until regulatory review to discover that your primary lender requires mandatory prepayment upon listing adds weeks to the approval timeline.

Private equity and venture capital funding can strengthen IPO positioning when structured correctly.

Institutional investors bring more than capital. They bring governance frameworks, quarterly reporting discipline, and board-level accountability that public markets expect. An enterprise that has successfully managed institutional investor relationships demonstrates readiness for the higher scrutiny that public listing entails.

However, equity funding also creates disclosure obligations. Every investor agreement, every shareholders' resolution, every board approval becomes part of your DRHP documentation. If these agreements include unusual provisions, ratchets, liquidation preferences, or drag-along rights that extend beyond the listing date, they require detailed explanation and, in some cases, renegotiation.

The funding strategy here: raise institutional equity early enough that governance frameworks become embedded operational practice, not rushed compliance exercises. Enterprises that bring institutional investors onboard 18–24 months before IPO filing benefit from governance maturity that SEBI reviewers recognise.

The most credible funding strategy for IPO candidates: demonstrable ability to generate and redeploy operating cash flow.

Enterprises that fund most of their growth with retained earnings signal operational efficiency and market positioning strength. This doesn't mean avoiding external capital; it means demonstrating that external capital accelerates growth that would occur anyway, rather than substituting for profitability.

AI-driven DRHP drafting processes automatically flag cash flow patterns indicating overreliance on external funding. If your growth has been funded primarily through successive equity raises with minimal cash generation, institutional investors may question the sustainability of your business model. The IPO itself may succeed, but post-listing performance becomes harder to sustain.

The discipline: build your funding plan around operating cash flow first, then layer external capital strategically for specific growth initiatives that exceed internal funding capacity.

Traditional IPO preparation treats the funding strategy as a historical narrative to be explained. S45’s AI-native approach treats it as institutional evidence to be validated.

In manual reviews, merchant bankers rely on documents provided by the company, term sheets, shareholder agreements, and board resolutions. Gaps lead to follow-ups, assumptions, or disclosure language noting missing records, all of which increase regulatory query risk.

S45’s proprietary systems analyse funding structures in different ways. The AI cross-checks funding rounds against regulatory filings, public disclosures, and financial statements. It flags inconsistencies in capital deployment, identifies related-party transactions, and highlights missing arm’s-length documentation.

This is not about replacing banker judgment. It ensures that judgment operates on verified, complete evidence rather than promoter representations.

The result is workflow compression. What typically takes 4–6 weeks through manual review can be completed in 7–10 days, enabling earlier gap identification and cleaner DRHP submissions.

Many mid-market enterprises pursuing SME Exchange listings assume that lighter disclosure requirements mean a simpler funding preparation strategy. This misunderstands the regulatory framework.

SME Exchange regulations require the same funding disclosure rigour as Main Board listings, complete shareholding history, detailed fund deployment disclosure, and related-party transaction documentation. The difference lies in issue size and investor eligibility, not documentation standards.

Where SME listings create unique funding challenges:

Unlike Main Board listings with market-making support, SME Exchange stocks often trade at low volumes. Promoters who fail to structure post-listing liquidity mechanisms make their shares illiquid, undermining the purpose of a public listing. Professional liquidity and pricing design services address this specifically for SME candidates, structuring market-maker arrangements and investor relations programmes before listing.

SME listings attract a range of investor profiles, often less institutionally sophisticated than Main Board participants. Your funding strategy disclosure must explain capital structure in clearer, more accessible language. Technical funding arrangements that institutional investors understand immediately require additional explanation for SME investors.

SME-listed companies face more restricted access to follow-on public offerings and institutional placements. Your pre-listing funding strategy must account for this by ensuring sufficient capital for 18–24 months of operations without assuming easy post-listing fundraising.

These complexities don't make SME Exchange listings harder; they make them different. Enterprises that understand these differences structure their funding strategies accordingly.

Every IPO-ready enterprise reaches a moment when the board must confront an uncomfortable question: Do we have an institutional capital structure or a promoter-friendly one?

The distinction matters because SEBI disclosure requirements force transparency around this question.

Institutional capital structure means:

Promoter-friendly capital structure means:

Neither structure is "wrong" for private operations. But only institutional capital structures survive public-market scrutiny without requiring a material restatement.

The promoter who discovers this difference during DRHP preparation faces difficult choices: delay the IPO while restructuring governance, or proceed with disclosure language that raises regulatory queries and investor concerns.

Best practice: surface these questions during initial IPO readiness assessment, before commitment to listing timelines. This allows measured restructuring rather than rushed compliance.

Most enterprises pursuing IPOs find that their historical funding requires adjustments before public market readiness. The question isn't whether restructuring is necessary; it's whether you identify the need early or discover it during regulatory review.

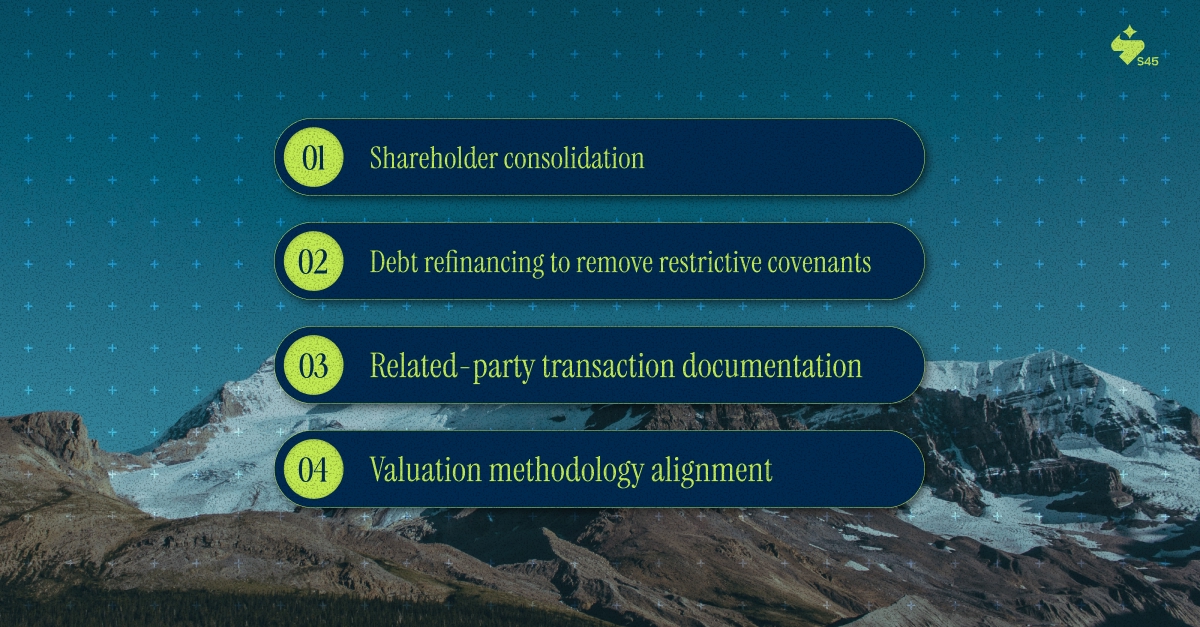

S45's IPO Readiness Scan specifically assesses whether your current funding structure can proceed directly to DRHP filing or requires preparatory work. The analysis flags several common restructuring requirements:

The timeline consideration: addressing these issues before engaging merchant bankers reduces both IPO preparation costs and timeline. Discovering them during DRHP drafting creates urgency that increases costs and extends timelines.

Many promoters approach IPOs with a focus solely on the capital raised through the public issue. This overlooks the more significant strategic question: how does public listing change your access to all forms of capital?

Post-listing, your funding options expand significantly:

However, these post-listing funding options require adherence to continuous disclosure obligations, minimum shareholding requirements, and pricing regulations that don't exist in private markets.

The pre-IPO funding strategy implication: structure your capital needs assuming post-listing funding will be available, but subject to constraints different from those of private capital. Enterprises that list with minimal working capital and plan to raise follow-on capital immediately often encounter timing mismatches that create operational stress.

Professional capital market execution includes post-listing funding planning, ensuring that your immediate capital raise through IPO provides sufficient runway while you establish post-listing funding relationships and demonstrate performance that supports follow-on capital raises.

The shift from private funding flexibility to public market accountability is the most consequential transition in an enterprise’s lifecycle. Most promoters encounter it as unexpected friction, missing documentation, unclear explanations, and late-stage restructuring that delays IPO timelines and weakens pricing outcomes.

S45 exists to eliminate this chaos before it begins.

Its IPO Readiness Scan evaluates funding strategy, capital structure, and disclosure readiness before listing timelines are locked. AI-driven DRHP drafting converts this analysis into evidence-linked disclosures that withstand regulatory scrutiny, while capital market execution ensures the funding structure supports both listing success and post-listing performance.

This is not funding advice. It is institutional funding execution, treating capital structure as the foundation of public-market credibility, not a compliance task.

Before committing board time, reputation, and capital to an IPO, assess whether your funding strategy can withstand institutional scrutiny. Clarity costs nothing. Chaos costs everything.

Assess your funding strategy’s IPO readiness with S45’s IPO Readiness Scan, institutional preparation for Main Board and SME Exchange candidates.

Discover more insights on similar topics