April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Disclaimer: This content is for informational purposes only and should not be construed as financial advice. Please consult with qualified financial advisors before making investment decisions.

Growth-stage companies face a recurring challenge: how to fuel expansion without constantly diluting ownership.

Every equity round chips away at founder control. Every new investor brings fresh expectations and board dynamics. For many startups in India, this tradeoff becomes increasingly painful as they scale.

The alternative often overlooked is venture debt, a financing instrument that has gained significant momentum in India's startup ecosystem. India's venture debt market reached $1.23 billion in 2024 and continues to expand rapidly, reflecting growing confidence in debt-backed growth strategies.

Unlike traditional bank loans, which require collateral and demonstrate profitability, venture debt operates on a different basis. It fills the space between equity rounds, offering capital to companies that have already proven their model to institutional investors.

This guide provides a comprehensive overview of everything you need to know about venture debt funds in India. From understanding how the mechanism works to determining when it makes strategic sense, you'll gain clarity on whether this financing route aligns with your growth trajectory.

Venture debt is a loan extended to early-stage and growth-stage companies that have already raised institutional venture capital. Unlike traditional bank loans that require tangible collateral and profitability, venture debt is underwritten based on your equity backing, growth metrics, and cash runway.

The typical venture debt arrangement includes three components:

Most arrangements are structured as term loans with 24-36 month tenures. You make interest-only payments for an initial period (often 6-12 months), followed by principal plus interest repayments. The warrants give lenders the option to purchase equity at a predetermined price, usually set at your last funding round valuation.

What makes venture debt particularly useful is timing. It's designed to extend your runway between equity rounds by 12-18 months, giving you more time to hit milestones that justify higher valuations in your next raise. This reduces dilution pressure and keeps you from raising equity at unfavorable terms.

The venture debt landscape in India has matured significantly over the past decade. There are now over hundreds of startups annually and dozens of active debt funds, for 2024–25 in India.

Let’s look at the top ones:

India's leading venture debt fund with over 100 investments across 15+ sectors.

Key Highlights:

Founded in 2019, Stride has launched three funds, emphasizing support for startups beyond capital deployment through strategic guidance and network access.

India's leading venture debt fund dedicated to supporting innovative startups backed by top-tier VC sponsors.

Key Highlights:

Alteria works closely with portfolio companies to align covenant structures with business cycles and growth phases, making them particularly suited for companies with seasonal or lumpy revenue patterns.

One of the largest venture debt providers in India, claiming to be both the first and largest in the country.

Key Highlights:

InnoVen has been instrumental in normalizing venture debt as a legitimate financing option for Indian founders, bringing institutional credibility and deep capital reserves to the space.

Founded in 2015, Trifecta provides both equity and debt funding along with financial advisory services.

Key Highlights:

This hybrid model provides Trifecta with a strategic perspective on how debt and equity interact at various growth stages, making them valuable thought partners beyond just capital providers.

Several newer funds have entered the market to meet growing demand. Beyond the established names, a host of emerging funds are focusing on specific sectors or geographies. These include regional players and industry-specific funds catering to particular business models or stages.

As venture debt in India continues to expand, choosing the right fund requires a clear understanding of your capital needs, repayment capacity, and growth priorities. To make an informed decision, it’s valuable to seek expert guidance.

Reach out to platforms like S45 Club that act as a strategic advisor to founders, helping evaluate funding options, structure deals effectively, and connect with credible venture debt providers that align with long-term business goals.

Understanding the venture debt process helps you approach it strategically rather than reactively. The journey from consideration to deployment follows a fairly standard pattern across most funds.

Before approaching venture debt providers, evaluate whether you meet the baseline criteria.

The best time to secure venture debt is when your runway is longest and your valuation is fresh. Approaching debt providers when you're desperate for capital weakens your negotiating position significantly.

Once you've identified potential funds, initiate conversations strategically.

This phase typically progresses rapidly, usually within 1-2 weeks. If there's mutual interest, you'll receive a term sheet outlining the proposed structure.

The due diligence process mirrors equity fundraising but focuses more heavily on financial sustainability.

Pay close attention to covenants. These protect the lender but can constrain your operational flexibility if they are too restrictive. Negotiate for breathing room that aligns with your business realities.

Once terms are agreed upon, legal documentation begins.

Timeline: Typically 3-4 weeks, depending on corporate structure complexity

After documentation is complete and legal conditions are satisfied, funds are disbursed. Most arrangements allow for a single drawdown, though some permit multiple tranches tied to milestone achievement.

Post-closing, you'll have regular reporting obligations that keep your lender informed.

Most funds are founder-friendly and will work with you on reasonable adjustments, but unexpected changes can quickly erode goodwill.

Once you understand the mechanics of venture debt, the natural question becomes: Is it the right fit for your business compared to equity funding? Let’s explore how the two stack up side by side.

Choosing between venture debt and equity isn't a binary decision. Most high-growth startups use a mix of both at different stages. The key is knowing when each option makes the most sense based on your current runway, growth stage, and capital goals.

Factor | Equity | Venture Debt |

Cost | Permanent ownership dilution. | Interest payments plus a small equity kicker (warrants). |

Dilution | Typically, 10–25% per round. | Usually 0.5–1% through warrants. |

Repayment | No repayment obligation. | Regular interest and principal repayments. |

Cash Flow Required | No | Yes, must support repayment schedule |

If you raise $2 million in equity at a $20 million valuation, you may give up around 10% ownership.

With venture debt, the same $2 million might carry a 15% warrant coverage, translating to only about 0.5–1% dilution, depending on conversion terms. The tradeoff is regular interest payments, typically in the 12–18% range in India.

For companies with strong gross margins and stable revenue, the interest burden is manageable. As a general rule, monthly debt service should remain below 20% of monthly revenue.

You Can Use Equity When:

Equity works well in the discovery and early growth stages, where risk is high and returns are uncertain.

Use Venture Debt When:

Venture debt is most effective when your business fundamentals are strong, and the capital is being used to accelerate specific outcomes.

Aspect | Equity | Venture Debt |

Control | Investors often take board seats and voting rights. | Lenders typically have observer roles, not control. |

Cost of Capital | High in the long term due to ownership dilution. | Lower if debt is repaid from cash flows. |

Runway Impact | Extends cash without repayment. | Adds repayment obligations that require careful planning. |

Smart capital structuring doesn't rely on just one type of funding. Use equity to support long-term, uncertain, or high-risk initiatives. Utilize venture debt to extend your runway, bridge funding gaps between rounds, or support measurable, short-term growth drivers.

A blended capital approach allows you to maximize growth while preserving ownership and control. This is the foundation of capital-efficient scaling.

Knowing when to use venture debt is only half the equation. To actually secure it, startups must meet specific eligibility and financial benchmarks. Let’s break down what determines access and how lenders assess your readiness.

Before you explore venture debt as a funding option, it's essential to understand how lenders evaluate startups. Unlike equity investors who take long-term ownership risk, debt providers need repayment within a fixed period. That means they assess risk differently, and they’re selective about who qualifies.

This section covers three interconnected factors that influence both access to venture debt and the terms you receive:

Each of these factors influences how lenders perceive your business, enabling you to structure a deal that supports growth without compromising cash flow or founder control.

Venture debt is typically available to startups that already have momentum. It is not designed for early-stage companies still figuring out product-market fit. Most funds want to see institutional backing, revenue traction, and sound financial planning.

Meeting these criteria doesn’t guarantee funding, but it positions you to negotiate better terms and access a wider pool of lenders.

Once you're considered eligible, the next factor is pricing. Venture debt is more expensive than traditional loans, but less dilutive than equity. Interest rates reflect the startup’s risk profile and repayment capacity.

Venture debt often includes warrants, which are rights for the lender to purchase equity in your company at a predetermined price. While the debt itself is non-dilutive, warrants create a potential for future dilution.

Warrants are a key part of venture debt structuring and should be evaluated with the same scrutiny as valuation in an equity round.

A clear understanding of these levers allows you to approach venture debt strategically. Instead of just asking “Can I raise debt?”, you can evaluate: “Am I ready to raise on the right terms, and do those terms support long-term value creation?”

Understanding eligibility and cost gives you the ‘what’, but not the ‘how.’ It's essential to examine how startups utilize venture debt in real-world growth scenarios.

Startups turn to venture debt as a strategic tool to support growth, reduce dilution, and increase flexibility. The key is using it where the capital drives measurable outcomes, without waiting for a full equity round.

Below are the most common and effective ways startups deploy venture debt.

Use venture debt to accelerate traction or unlock valuation milestones.

Utilize debt to manage operations efficiently and maintain control during uncertain periods.

If the capital you raise has a clear, short-to-mid-term ROI or helps you unlock a stronger valuation later, venture debt may be the right fit. If you're using it to buy time, prove value, or avoid dilution, you're on the right track.

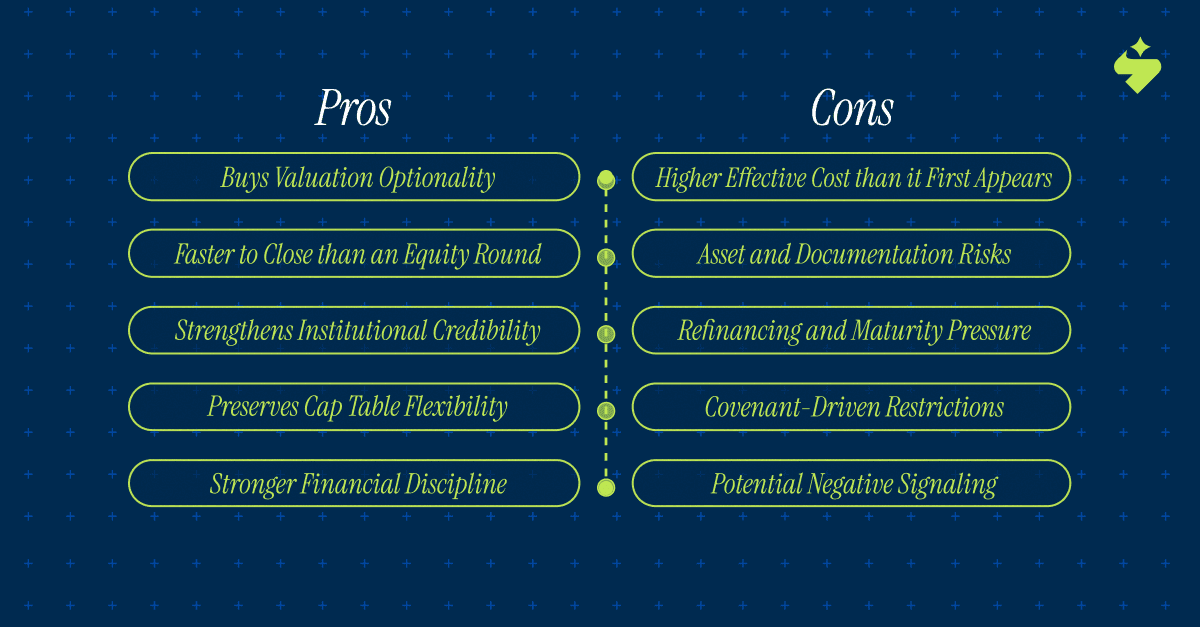

Venture debt creates opportunities but also introduces constraints. Evaluating both sides honestly helps you make informed decisions.

While understanding theory is essential, executing a sound venture debt strategy requires experience and connections. That’s where expert partners like S45 Club come in, guiding businesses through every stage of the capital journey.

Navigating the capital markets as a growth-stage SME requires more than just access to funding. It demands strategic thinking about capital structure, governance readiness, and market positioning.

S45 Club serves as a bridge between ambitious businesses and the institutional capital required to scale. For companies evaluating venture debt, S45 provides the strategic frameworks and market access that make the difference between capital that constrains and capital that accelerates.

Here's how S45 Club supports SMEs through their capital journey:

Beyond capital access, S45 Club brings expertise in preparing companies for the institutional scrutiny that comes with venture debt. This includes tightening financial operations, implementing strong reporting systems, and establishing the governance structures that debt providers expect.

Venture debt has progressed from a niche financing option to a mainstream capital strategy for growth-stage companies in India. The market's maturation reflects growing sophistication among both founders and lenders about when and how debt creates value without introducing undue risk.

The decision to pursue venture debt shouldn't be reactive, driven by cash crunches or complex equity markets. Used strategically between equity rounds, it extends runway, minimizes dilution, and gives you the time and resources to achieve milestones that justify premium valuations.

The best capital structures blend equity's flexibility with debt's efficiency, optimizing for both growth and founder outcomes. As you evaluate whether venture debt fits your situation, focus on fundamentals: adequate runway to service debt comfortably, capital funding initiatives with measurable ROI, and ability to meet eligibility criteria and secure reasonable terms.

S45 Club helps businesses navigate these decisions with clarity and confidence. If you’re ready to explore whether venture debt aligns with your funding roadmap, book a consultation call with S45 Club to discuss how a tailored capital strategy can accelerate your next stage of growth.

Discover more insights on similar topics