April 9, 202612 min read

Revenue-Based Financing in India: When and How to Use It?

By Abhishek Bhanushali

Debt & Equity Financing

Startups drive innovation and growth, but securing funding can be a major challenge. Traditional methods like bank loans or venture capital often come with rigid terms, high-interest rates, or equity loss. For many young companies, these barriers can hinder access to necessary capital.

Enter Revenue-Based Financing (RBF), an alternative that provides flexibility and control. Unlike traditional funding, RBF allows startups to secure capital based on future revenue projections, without giving up equity or adhering to rigid repayment schedules. It’s quickly becoming a popular choice for startups seeking non-dilutive, performance-based financing.

Revenue-Based Financing (RBF) is a modern funding option that allows businesses to secure capital based on their future revenue. Instead of relying on traditional debt or equity financing, RBF offers an alternative that aligns with the company’s performance. Essentially, a business receives capital upfront and agrees to repay the funding through a percentage of its monthly revenue until a specified multiple of the original funding amount is paid back.

Feature | Traditional Debt Financing | Equity Financing | Revenue-Based Financing (RBF) |

Repayment Structure | Fixed monthly payments, regardless of revenue | No repayment, equity holders get returns based on business performance | Percentage of revenue, varying with business performance |

Ownership Impact | No loss of ownership, but may require collateral | Equity is sold, giving up ownership | No loss of ownership; non-dilutive |

Flexibility | Rigid, fixed payments | Flexible, but control is relinquished | Flexible payments based on revenue |

Access to Capital | Slow approval process | Often lengthy due to investor negotiations | Quick approval and access to funds |

Eligibility Requirements | Requires a strong credit history and collateral | Requires high growth potential and willingness to give up control | Requires predictable revenue streams, not based on credit or collateral |

Risk to Business | Fixed payments regardless of performance | Loss of control and decision-making power | Lower financial strain due to variable repayments |

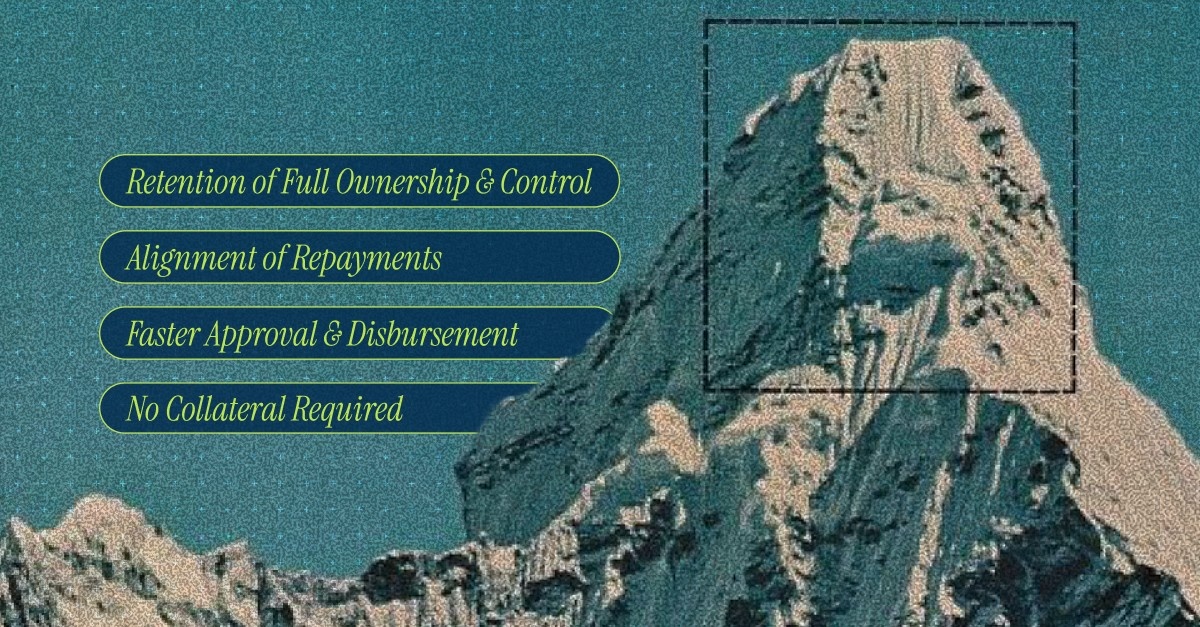

Revenue-Based Financing (RBF) stands out for its startup-friendly structure, offering funding without forcing founders to give up ownership or face rigid repayment terms. Here’s a closer look at its key features:

Revenue-Based Financing (RBF) is a unique and flexible approach to funding that links repayments to a business’s revenue performance. This method offers startups a way to secure capital without the constraints of traditional debt or equity financing.

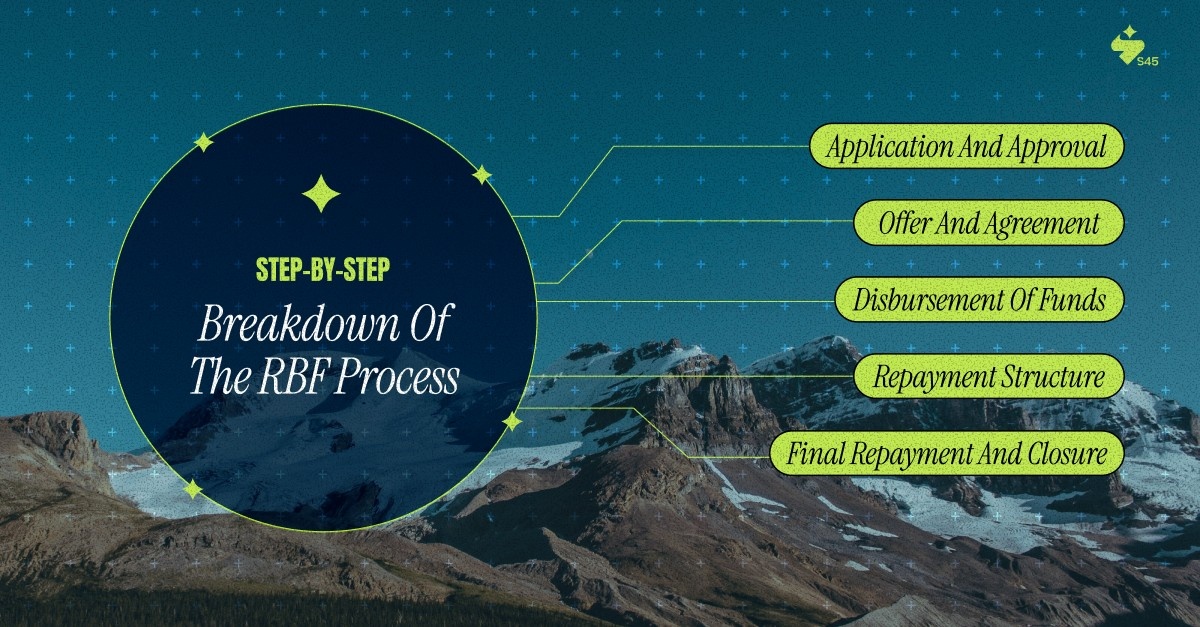

Let’s explore the step-by-step process of how RBF works, the repayment structure, and key elements like repayment caps and duration.

Understanding the RBF process is crucial for any startup considering this form of financing. Here's a breakdown of each step, from application to repayment, to give you a clear idea of how it works in practice.

To make the RBF repayment structure easier to understand, let's go through a real-life example. This will help you visualize how repayments fluctuate with monthly revenue and how the loan term varies based on performance.

Monthly Revenue:

Repayment for the month = $50,000 * 5% = $2,500

Duration of Repayment:

Early Repayment Scenario:

Understanding the concept of repayment caps and duration is essential to grasping the full benefits of RBF. These elements give startups both flexibility and assurance, knowing that the total amount to be repaid is capped and the repayment duration is based on their ability to pay.

Repayment Cap:

Duration:

RBF’s flexibility makes it especially appealing for businesses with seasonal or fluctuating revenue, as it reduces the financial burden during slower periods while allowing for quicker repayment when the business is doing well.

Revenue-Based Financing (RBF) offers several benefits that make it an attractive funding option for startups. Below are the key advantages that can help businesses grow without sacrificing ownership or facing rigid financial constraints.

While Revenue-Based Financing (RBF) offers numerous advantages, there are also some potential drawbacks that startups should carefully consider before opting for this type of funding. Here are a few challenges associated with RBF:

Revenue-Based Financing (RBF) is gaining momentum as an effective funding model for startups. Here are some leading platforms offering RBF solutions, both globally and in India.

S45 Club helps MSMEs in India access growth capital and strategic guidance.

Klub provides businesses with adaptable, founder-friendly funding solutions.

Velocity specializes in quick funding solutions for e-commerce businesses.

Recur Club supports companies with recurring revenue models to scale efficiently.

Clearco leverages data to provide capital to high-growth digital businesses.

Also Read: Business Advisory Council: Key Functions and Benefits

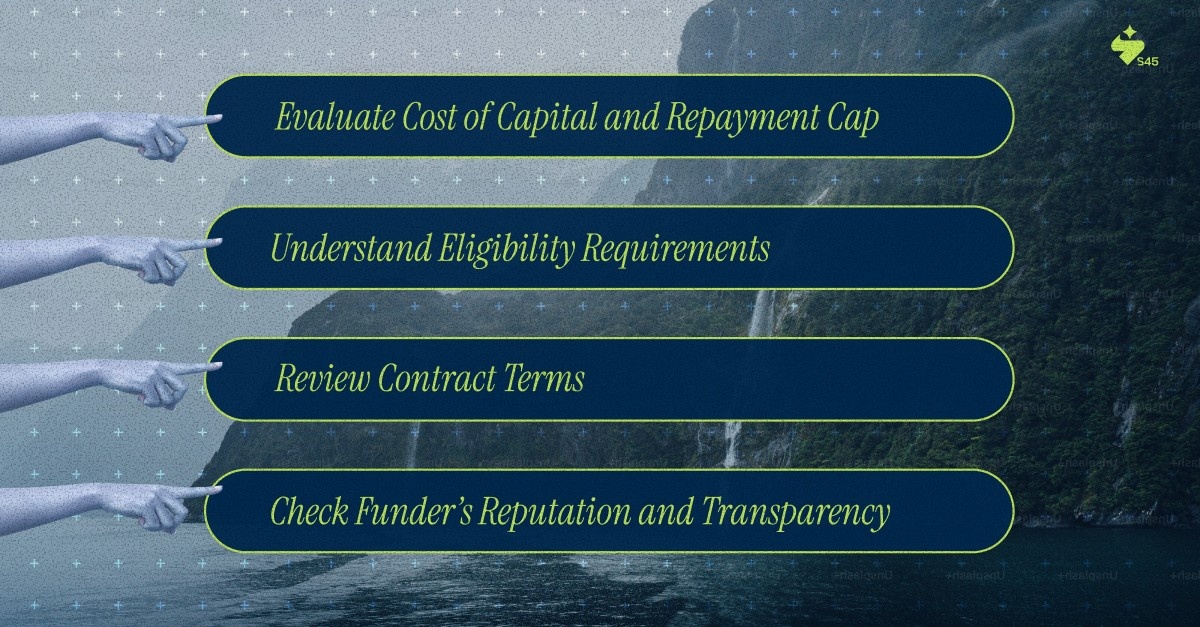

Revenue-Based Financing (RBF) can be an excellent option for startups, but it’s important to carefully evaluate several key factors before committing. Here are the most important considerations to keep in mind:

Before diving into RBF, it’s essential to understand the financial implications. The cost of capital and the repayment cap can significantly impact your overall financial health, so it’s important to assess these aspects carefully.

Each RBF provider has different criteria for eligibility, so it’s important to understand what is required to qualify. Meeting these requirements will help you decide if RBF is a viable option for your business.

The contract terms can vary widely between providers, so it’s critical to review the specific conditions that will affect your repayments. Understanding these terms upfront will prevent any surprises down the road.

Choosing the right provider is key to a smooth RBF experience. Make sure to thoroughly research the provider’s reputation and ensure they operate with transparency.

By considering these factors, you’ll be in a stronger position to make an informed decision and choose the right Revenue-Based Financing option for your business.

As a startup, finding the right support to scale efficiently can be challenging. That's where S45 Club comes in. They provide not only Revenue-Based Financing (RBF) but also the strategic capital and expert guidance that can accelerate your business growth. Watch this video to see how S45 Club can empower your startup:

Watch the video: S45 Club OverviewIn this video, you’ll discover how S45 Club helps startups leverage capital for sustainable growth.

S45 Club's Role in Your Startup’s SuccessS45 Club helps startups access the right capital and guidance to scale efficiently, combining financial support with expert strategic advice.

For more information on how S45 Club can fuel your startup's growth and provide strategic support, visit S45 Club.

Revenue-Based Financing (RBF) offers startups a flexible, non-dilutive funding option that aligns with their revenue performance, allowing businesses to grow without giving up ownership or taking on heavy debt. While RBF provides key benefits such as flexible repayments, quick access to capital, and retention of full control, it's important to carefully evaluate the cost of capital, eligibility requirements, and contract terms before moving forward.

At S45 Club, we go beyond funding, offering strategic capital, expert guidance, and personalized growth support to help your startup scale sustainably and confidently.

Ready to unlock your growth potential? Book your consultation with S45 Club today and discover how revenue-based finance can power your next stage of success.

Discover more insights on similar topics