April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

You’ve spent months refining your pitch deck, endured tough due diligence, and finally received the term sheet; capital is on the way. But here’s the question most MSME founders never ask: Is your venture capital fund compliant with SEBI regulations?

It may sound bureaucratic, even unnecessary, but in 2025, this question can define your startup’s future. SEBI now requires all legacy Venture Capital Funds (VCFs) to shift to the Alternative Investment Fund (AIF) framework, yet nearly 130 of 179 registered VCFs remain non-compliant or inactive.

Understanding SEBI’s rules helps ensure your investor can legally deploy funds, prevent compliance delays, and align with credible partners. This blog explains the key SEBI requirements every founder must know to protect funding and future growth.

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

SEBI’s latest changes mark India’s shift from a scattered regulatory framework to a unified, transparent system that protects both investors and entrepreneurs.

SEBI introduced the Venture Capital Funds (VCF) Regulations, 1996, as India’s first official rulebook for venture capital.

Over time, these rules became outdated. As private equity, hedge, and angel funds emerged under separate rules, confusion and loopholes appeared in the system.

SEBI replaced the old framework on May 21, 2012, with the Alternative Investment Funds (AIF) Regulations.

For founders, this means your investor is now part of a regulated and structured ecosystem, offering greater security and accountability.

At S45, we view capital as more than money; it’s a foundation for long-term growth. We help founders connect with compliant, stable investors who value transparency and play by the rules, ensuring funding remains reliable through every growth stage. Now, let’s find out what SEBI identifies as Category I AIFs.

Understanding the Category I AIF structure is crucial for founders. It reveals what your investor can and cannot do, how their fund operates, and the timelines that govern your relationship.

Category I AIFs must have a corpus of at least ₹20 crore, with each investor contributing a minimum of ₹1 crore. The fund can have up to 1,000 investors.

But with the two-thirds rule, you need to be more conscious.

SEBI mandates that at least two-thirds of the fund’s corpus be invested in unlisted equity shares or equity-linked instruments. This ensures the fund is genuinely focused on venture capital, not just low-risk investments.

Therefore, you need partners like S45 who can commit to the long haul, not investors who are counting down to their exit. Next, let’s find out the impact of the migration on your business.

By now, you might be wondering: why should I care about my VC's regulatory status? Here's the reality: non-compliant funds face escalating consequences:

When your investor is distracted by existential compliance issues, your business pays the price in lost strategic guidance, delayed capital deployment, and weakened networks.

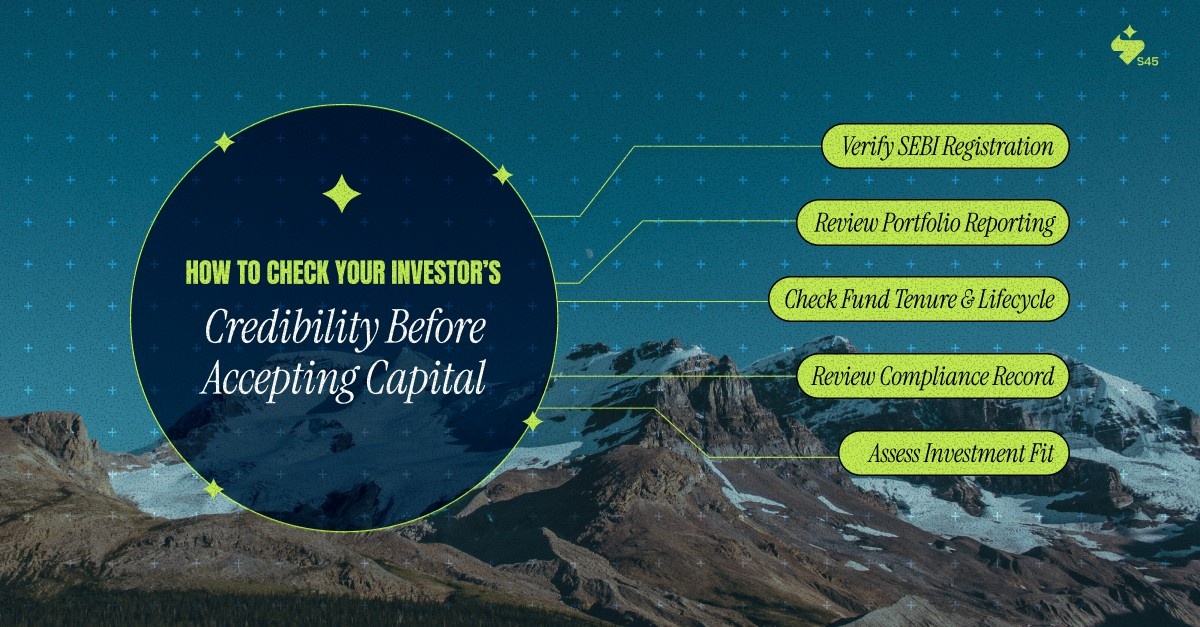

You wouldn’t hire an executive without checking their background. The same rule applies to investors. Before taking their money, verify their compliance, track record, and alignment with your goals.

Go to the SEBI website and open the “Intermediaries” section.

Request the fund’s latest quarterly investment reports submitted to SEBI.

A well-diversified fund with consistent reporting usually indicates sound governance.

Ask for the Private Placement Memorandum (PPM) or Limited Partnership Agreement (LPA) to understand:

If the fund is in its final years, the investor may focus more on exits than new follow-ons. Know where your deal fits in their timeline.

Search for SEBI enforcement actions or penalty orders against the fund or sponsor. This information is public under the “Enforcement Actions” section of SEBI’s site. A clean record shows discipline, while frequent disputes can indicate governance or operational problems.

Review the fund's investment mandate.

When structure, compliance, and strategy align, you’re not just taking capital, you’re choosing a stable long-term partner.

Not every clause in your term sheet is up for discussion. Some terms come directly from SEBI’s AIF rules and can’t be changed. Knowing which ones are fixed helps you save time and focus on points that truly impact your deal.

These are SEBI-mandated and apply to all Category I AIFs:

Everything else can be discussed. These include:

Push where you have leverage, and verify any claim that “SEBI doesn’t allow this.” That statement often hides a commercial preference, not a rule. Strategic partners like S45 often can help you here so that you can avoid wasting time and focus on terms that shape your long-term control and alignment.

Now, let’s explore the scenario where your VC fails to migrate by the March 2025 deadline. Here's what happens.

Non-migrated VCFs with active schemes face enhanced reporting and surveillance. Expired schemes operating beyond their liquidation period face penalties, including potential loss of registration. SEBI can mandate asset distribution and investor repayments.

As a portfolio company, you have limited formal rights to force your investor's compliance. However, you can:

By understanding these risks and preparing early, you can protect your company from potential fallout. But what if you can have a partner who would do that for you?

At S45, we don't just facilitate capital connections; we architect sustainable growth pathways for MSME founders. Our approach combines:

If you're an Indian entrepreneur building an MSME designed to last, then the regulatory landscape might be complex, but the path forward doesn't have to be. Connect with S45 to explore how we support founders navigating growth capital, operational scaling, and legacy building.

Discover more insights on similar topics