April 10, 202611 min read

Angel vs. Seed Funding: What Every Indian Founder Must Know Before Raising Capital

By Abhishek Bhanushali

Startup Funding

Key Takeaways

1. Settlement funding provides liquidity when legal cases take time. It helps plaintiffs manage essential expenses without waiting years for a settlement payout.

2. It’s non-recourse; repayment only happens if the case succeeds. This makes it a safer alternative for those who cannot access traditional loans, though it often comes at a high cost.

3. Costs and risks can be significant. High fees and compounding interest may reduce final settlements, so understanding the full terms is essential.

4. Alternatives exist and should be reviewed first. Personal loans, insurance coverage, or structured settlements can be more economical and transparent.

Legal disputes often take months, sometimes years, to resolve. During this time, plaintiffs can face significant financial strain, and medical bills, household expenses, or lost income can make waiting for a fair settlement difficult. Settlement funding offers a practical, though costly, solution to ease that burden.

Unlike a traditional loan, settlement funding provides a cash advance against a pending legal case.

The amount advanced depends on the strength of the claim and the estimated settlement value. If the case succeeds, the funder recovers its advance plus fees. If the plaintiff loses, there is usually no repayment required.

For many individuals, this funding acts as a financial lifeline during litigation. Yet, as with any form of financing, it demands careful understanding. This article explores what settlement funding is, how it works, its benefits, risks, and the questions to ask before considering it.

Settlement funding, sometimes called pre-settlement funding or lawsuit funding, is a financial arrangement that allows plaintiffs to receive a portion of their expected legal settlement before the case concludes.

These cases can take time, especially when negotiation or appeals are involved. Settlement funding helps plaintiffs cover immediate financial needs without accepting a low settlement offer out of pressure.

Settlement funding is not a loan in the traditional sense. There are no monthly payments, no credit checks, and no collateral. Instead, repayment happens only if the plaintiff wins or settles.

However, the cost can be high, funding fees and interest accumulate over time, often making this one of the most expensive financing options available.

S45 Insight: We often remind business leaders and individuals that not all funding is equal. Settlement funding can provide short-term relief but should never replace disciplined financial planning or a well-advised legal strategy.

Also Read: Categories of Alternative Investment Funds Explained

Settlement funding follows a transparent but multi-step process. The funder evaluates the case, estimates settlement potential, and advances part of that value.

Stage | Description |

1. Application | The plaintiff or lawyer submits case details to the funding company. |

2. Case Review | The funder reviews evidence, liability, and the likelihood of success. |

3. Legal Consultation | The plaintiff’s lawyer provides additional information to confirm case validity. |

4. Offer and Disbursement | If approved, the funder offers a cash advance (typically 10–20% of the expected settlement). |

5. Repayment | On successful settlement, repayment plus fees is deducted from the proceeds. If the case fails, no repayment applies. |

S45 Insight: Funding should act as a bridge, not a crutch. We encourage individuals and founders to calculate not just the amount needed today, but how it affects what remains tomorrow.

Also Read: How Revenue-Based Financing Works Explained

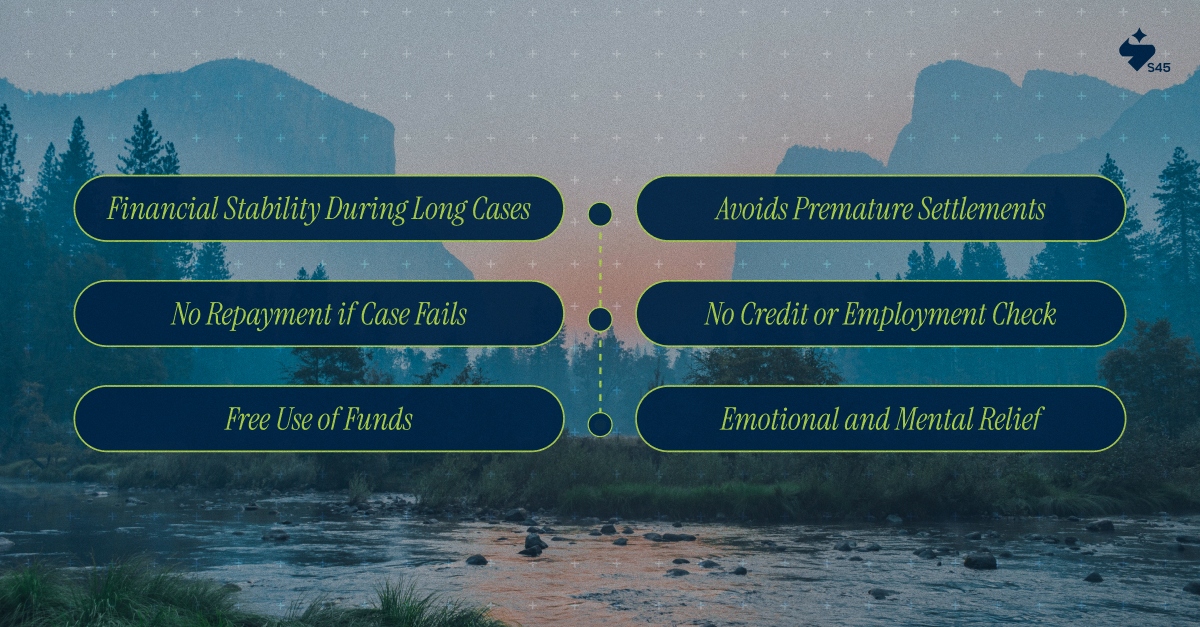

When used strategically, settlement funding can provide essential financial support. It enables plaintiffs to maintain stability while pursuing fair compensation.

Legal proceedings can take years. Settlement funding provides liquidity when income stops, but expenses continue, helping plaintiffs manage daily life confidently.

Financial stress often pushes plaintiffs to accept early, lower offers. Funding allows more time for negotiation, improving the chance of securing a fair and full settlement.

Because it’s non-recourse, repayment occurs only after a successful outcome. If the case is lost, the funder absorbs the loss, not the plaintiff.

Approval depends entirely on case strength. This helps individuals who may not qualify for traditional loans due to damaged credit or employment gaps.

Funds can be used at the plaintiff’s discretion. There are no spending restrictions, whether for medical care, legal costs, or personal needs.

With immediate financial pressure reduced, plaintiffs can focus on recovery and legal proceedings without distraction.

While settlement funding can provide financial relief, it comes at a high cost. Understanding the risks ensures you make a decision grounded in reality, not urgency.

Example: If a plaintiff receives ₹10 lakh and the case lasts two years, repayment could exceed ₹16–₹18 lakh, leaving little from the eventual settlement.

At S45 Club, we remind founders and individuals, every form of capital carries a cost. The goal isn’t to avoid risk entirely, but to understand it well enough to manage it wisely.

Also Read: Types of Private Equity Explained

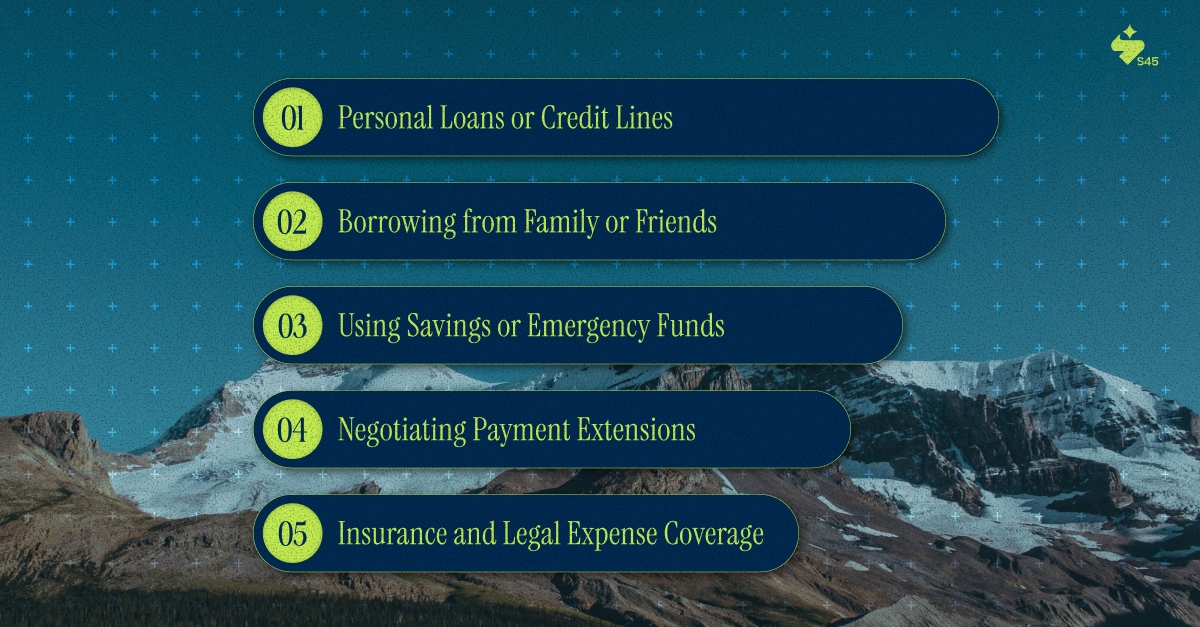

Before taking settlement funding, explore other financing routes. Many alternatives offer lower costs, clearer repayment terms, and better financial control.

Pros: Predictable terms, transparent cost.

Cons: Requires creditworthiness and personal liability.

Pros: Minimal cost, flexible repayment.

Cons: Can strain relationships if expectations are unclear.

Pros: No repayment risk.

Cons: Reduces financial cushion.

Pros: No borrowing cost.

Cons: May not cover all expenses.

Pros: Built-in benefit, no repayment.

Cons: Limited to specific conditions.

Option | Cost Level | Repayment Required? | Best For |

Settlement Funding | High | Only if the case succeeds | Urgent, high-need cases |

Personal Loan | Medium | Always | Strong credit profiles |

Family/Friends Loan | Low | Flexible | Short-term needs |

Savings | None | N/A | Liquidity holders |

Insurance | None | N/A | Covered claims |

The strongest financial decisions come from exploring every option, not choosing the fastest. At S45 Club, we help decision-makers weigh urgency against opportunity, and long-term outcomes over short-term ease.

Also Read: What Are Private Equity Firms? A Simple Guide for 2025

Use this checklist to evaluate if settlement funding truly fits your situation. Treat it like a decision framework, not just a financial option.

Settlement funding can be a lifeline in difficult times, but like any financial product, it requires understanding, discipline, and caution. It offers speed and liquidity, yet comes with cost and consequence. The best outcomes come when it is treated as a strategic choice, not a desperate measure.

For plaintiffs and founders alike, every funding decision should protect tomorrow’s stability, not just today’s comfort.

When managed with awareness, transparency, and proper legal guidance, settlement funding can provide breathing room during long legal battles without compromising long-term financial goals.

At S45 Club, we help Indian entrepreneurs, investors, and individuals make capital decisions that build stronger foundations for growth, whether it’s structured finance, legal funding, or equity partnerships. The principle remains the same: choose clarity over speed, sustainability over shortcuts.

Discover more insights on similar topics