April 1, 202610 min read

Third-Party Funding in Indian Arbitration: What You Need to Know

By Abhishek Bhanushali

Finance Advice

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a qualified advisor before making any credit or loan-related decisions.

For many SMEs, growth isn’t limited by potential; it’s limited by cash flow. Whether it’s buying inventory, upgrading machines, paying vendors, or managing seasonal dips, businesses often need additional financial support.

This is where credit funding steps in. Yet, many SME owners find themselves confused:

The real challenge isn’t borrowing money, it’s borrowing wisely.

Before diving deeper, here’s a soft reminder: many successful Indian SMEs rely on structured guidance and financial expertise to avoid taking on the wrong credit or mismatching repayment obligations with their cash cycles.

Let’s explore what credit funding means, how it works, and how SMEs can use it strategically.

Credit funding refers to the process of borrowing money from financial institutions, NBFCs, private lenders, or credit platforms to support business operations, manage cash flow, or finance expansion. Unlike equity, credit funding allows SMEs to access capital without giving up ownership, making it one of the most practical and commonly used financing tools for Indian businesses.

According to the IFC MSME Finance Gap Study, India’s MSME credit gap stands at ₹20-25 trillion, indicating that millions of businesses rely on external funding to survive and scale. These numbers highlight a simple truth: Credit isn’t optional for SMEs, it’s essential.

A well-structured credit strategy helps SMEs:

But choosing the wrong credit structure can quickly turn into repayment stress, cash-flow instability, and long-term financial strain. Understanding credit funding is the first step to using it wisely.

Now that we’ve seen the foundational role credit plays, let’s break down the specific reasons SMEs rely on credit funding to stay competitive.

SMEs operate in environments where revenue cycles, customer payments, and working-capital demands are constantly shifting. Even profitable businesses often face temporary liquidity shortages, making credit funding a crucial financial tool, not just for survival, but for sustainable growth.

Access to credit empowers SMEs to stabilize operations, take advantage of market opportunities, and protect themselves during downturns. Without timely credit support, SMEs may delay production, lose customers, or miss out on growth opportunities.

Understanding why SMEs rely on credit naturally leads to the next question: what kinds of credit options are available to support different business needs?

Understanding the right type of credit is just as important as securing it. Different stages of business, launch, expansion, seasonal swings, or recovery, require different funding formats. SMEs that choose the right credit product tend to manage cash flow more efficiently, reduce financing costs, and grow with fewer disruptions.

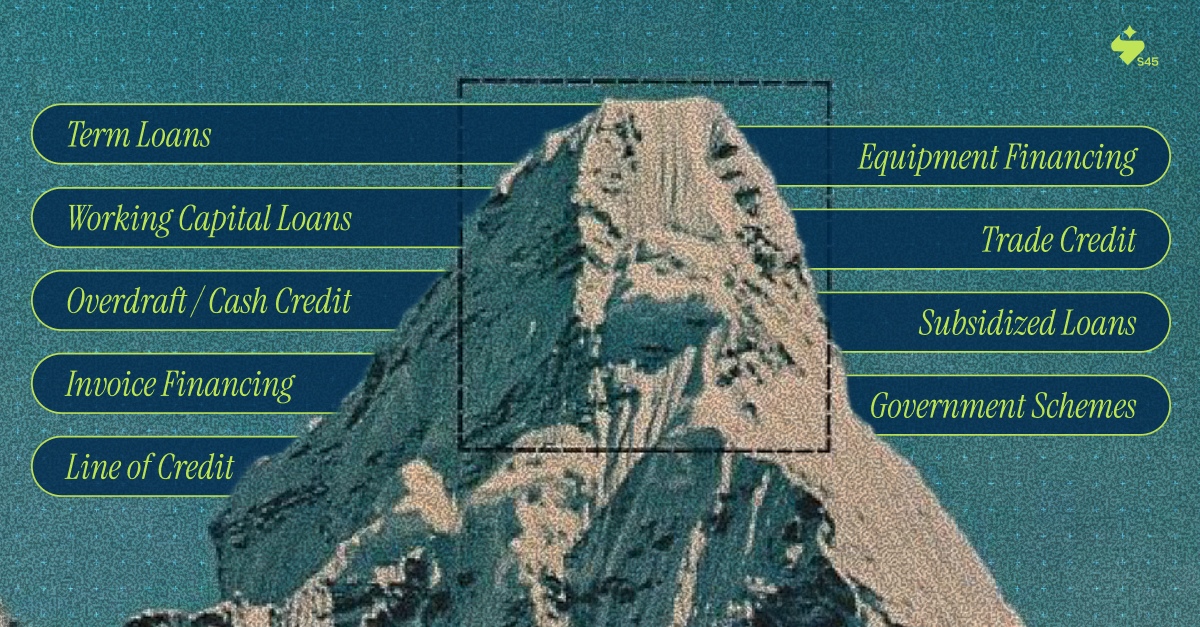

Here’s a clear breakdown of the most commonly used credit options and how they support SME growth.

A term loan is a traditional business loan where SMEs borrow a fixed amount and repay it over a set period with interest. These can be short-term, medium-term, or long-term, depending on the business need.

How it benefits SMEs:

Example: A manufacturing SME takes a 3-year term loan to upgrade machinery, improving production speed and reducing operational costs.

Working capital loans help SMEs manage daily operations such as payroll, inventory, vendor payments, and seasonal demand fluctuations.

How it benefits SMEs:

Example: A wholesale distributor uses a working capital loan to stock additional inventory before Diwali season, increasing sales and meeting customer demand.

Banks provide an overdraft or cash credit facility that allows SMEs to withdraw funds beyond their account balance, up to a pre-approved limit.

How it benefits SMEs:

Example: A textile exporter uses a cash credit facility to cover vendor payments while waiting for overseas buyers to clear invoices.

This form of credit allows SMEs to borrow against unpaid customer invoices, giving them immediate liquidity instead of waiting 30–90 days.

How it benefits SMEs:

Example: A B2B furniture manufacturer receives 80% of invoice value upfront through invoice discounting, helping them start new orders faster.

A revolving credit line gives SMEs ongoing access to funds up to a certain limit, similar to a credit card for business purposes.

How it benefits SMEs:

Example: A marketing agency taps into a ₹20-lakh credit line to hire temporary staff during a large campaign project.

Used specifically to purchase business equipment, where the asset itself becomes collateral. Common in manufacturing, logistics, construction, and healthcare.

How it benefits SMEs:

Example: A logistics company finances delivery vans through equipment financing, scaling operations without blocking working capital.

Trade credit is when suppliers allow businesses to purchase goods or raw materials on credit, usually with 30- to 90-day payment terms.

How it benefits SMEs:

Example: A small electronics retailer buys stock on 45-day credit terms, enabling continuous sales without cash-flow stress.

Government-backed programs like CGTMSE, MUDRA loans, and SIDBI schemes offer collateral-free loans and lower interest rates for SMEs.

How it benefits SMEs:

Example: A food processing unit secures an MUDRA loan to expand production capacity at a lower interest rate than private lenders.

Venture debt is a form of credit offered to high-growth SMEs or startups backed by investors. It complements equity without diluting ownership.

How it benefits SMEs:

Example: A fast-growing SaaS SME raises venture debt to invest in product upgrades while awaiting the next equity round.

Now that we’ve explored the major credit options, let’s break down how to choose the one that works best for your SME.

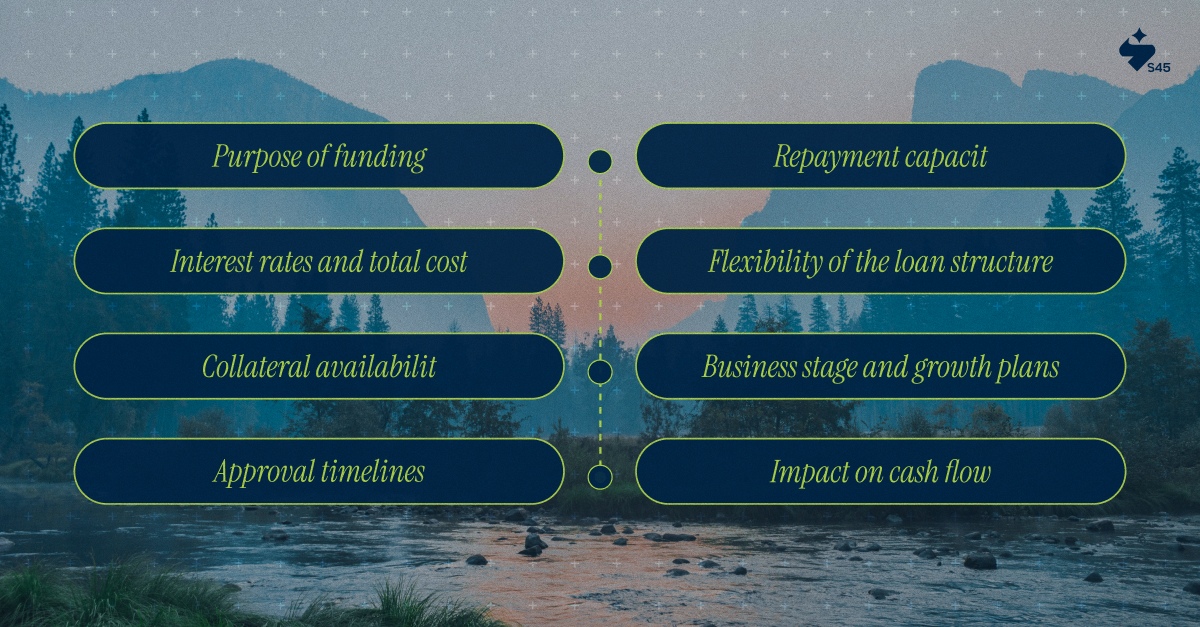

Choosing the right credit product is just as important as accessing credit itself. Each option influences cash flow, risk, and long-term business planning differently. A structured evaluation helps SMEs avoid mismatched loans, high interest costs, or unnecessary debt.

Key factors to consider:

At S45, SMEs are matched with seasoned mentors and financial specialists who offer far more than surface-level guidance. They help challenge assumptions, stress-test funding decisions, and provide practical clarity so every credit choice supports long-term stability and growth.

To make smarter borrowing decisions, SMEs must first know what lenders consider a good credit score.

A credit score reflects how trustworthy a business or individual is when it comes to repaying loans. For SMEs, lenders often assess both the business credit profile and the founder’s personal credit score before approving funding.

In India, credit scores are typically calculated by agencies like CIBIL, Experian, CRIF High Mark, and Equifax, usually ranging from 300 to 900.

A higher score signals lower risk, faster approval, and better interest rates. Most banks and NBFCs consider anything above 700 to be strong, but the ideal range can vary depending on the type of credit you are applying for.

Also Read: Understanding Micro Venture Capital for Startups

A good credit score opens doors to better funding, so here are actionable steps SMEs can take to build and maintain a strong profile.

A healthy credit score doesn’t just boost loan approval chances; it reduces borrowing costs, strengthens lender confidence, and gives SMEs more room to negotiate terms. Improving your credit score is a gradual process, but even small, consistent changes can make a significant impact on your financial profile.

While business credit cards can be incredibly useful for managing day-to-day expenses, they can also become a source of financial stress if not handled carefully. Recognizing the warning signs early helps SMEs avoid unnecessary debt, higher interest costs, and long-term credit damage.

Suggested read: India's SME Growth: Challenges and Opportunities

To avoid these costly mistakes and navigate credit decisions with more clarity, SMEs often need a trusted partner who can bring objectivity, structure, and expertise to the process.

The S45 Club supports India’s leading SMEs by strengthening their access to capital, improving financial discipline, and aligning funding decisions with long-term growth goals. We help you handle complex credit queries with clear, actionable guidance tailored to your business model and financial realities. Whether you operate in manufacturing, trading, or any other sector, our approach ensures your credit choices strengthen, not strain your business.

Here's how we assist with your credit funding decisions:

S45 works alongside you to simplify credit funding, reduce risk, and help your business grow with confidence. Connect with S45 today to make smarter, data-backed credit decisions.

Credit funding is more than just securing money; it’s about making informed choices that strengthen cash flow, reduce financial stress, and fuel long-term business growth. When SMEs understand their credit options, maintain strong financial discipline, and avoid common borrowing mistakes, they unlock far greater stability and resilience in a competitive market.

With the right guidance, credit stops being a challenge and becomes a powerful tool for expansion, sustainability, and smart financial planning.

Ready to make stronger credit decisions? S45 is built for ambitious Indian SMEs that want to scale with confidence. From evaluating loan structures to selecting the most cost-efficient credit options, our mentors and financial experts guide you through every step.

Become a part of Club S45 today, and let’s build lasting value, side by side.

Discover more insights on similar topics