April 10, 202611 min read

Angel vs. Seed Funding: What Every Indian Founder Must Know Before Raising Capital

By Abhishek Bhanushali

Startup Funding

Key Takeaways

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Here is the paradox every MSME founder knows too well. Your biggest customer wants 5,000 units next quarter. You have the capacity, the team, and the expertise. What you do not have is the working capital to buy raw materials upfront. By the time your current invoices clear, the opportunity window closes.

This is not about poor planning. It is about the fundamental architecture of cash flow in manufacturing. Raw materials need payment today. Production takes weeks. Invoices are clear in 45 to 90 days. The math never quite adds up without strategic capital.

Short-term funding exists to solve exactly this problem. But most founders approach it wrong. They see it as crisis management when it should be a growth strategy. They focus on interest rates when they should focus on opportunity capture.

This blog walks you through the strategic framework for using short-term funding to scale sustainably, the India-specific advantages available to MSMEs, and how to build funding relationships that compound over time rather than create short-term stress.

Short-term funding is capital borrowed for a limited period—usually 3 to 18 months—to meet immediate business needs. In simple terms, it helps MSMEs manage cash flow gaps without waiting for revenue cycles.

For example, if you get a 20% discount by paying suppliers upfront on a ₹10 lakh order, you save ₹2 lakh. Even if the short-term loan costs ₹20,000 in interest, you still gain ₹1.8 lakh. That's the real purpose—using quick capital to unlock opportunities, not just to borrow money.

The shift from viewing short-term funding as emergency debt to seeing it as strategic growth capital changes how you approach every business opportunity. Now, let us explore the specific funding instruments available to Indian MSMEs and how each serves different operational needs.

Indian MSMEs have more funding options today than ever before. The challenge is not availability but understanding which instrument serves your specific need. Here is what actually matters in practice.

You have delivered products worth ₹15 lakh. Your invoice payment is due in 60 days. But you need cash now for the next production cycle. Invoice discounting lets you access up to 80% of the invoice value immediately.

Best for:

MSMEs with established customers who have payment cycles of 30 to 90 days. Works particularly well when you have multiple invoices from creditworthy buyers.

These are short-term loans designed specifically for operational expenses. Raw materials, salaries, utility bills, and inventory purchases. Unlike term loans tied to specific assets, working capital loans give you flexibility in deployment.

India Specific Advantage:

MUDRA loans under the Tarun category offer up to ₹10 lakh without collateral. For established MSMEs, the CGTMSE scheme provides guarantee cover up to 85%, making banks more comfortable with unsecured lending.

This is where smart founders gain a competitive advantage. Supply chain financing works through your existing supplier relationships. A financing partner pays your suppliers directly, and you repay the partner once your customer pays you.

Strategic value:

Strengthens supplier relationships through timely payments while preserving your cash flow. Particularly powerful for MSMEs working with larger buyers who demand extended payment terms.

You receive a large order but lack the funds to fulfil it. Purchase order financing provides capital specifically to complete that order. The financing is secured by the order itself, making it accessible even for MSMEs with limited credit history.

Reality check:

This works best when you have a confirmed purchase order from a creditworthy buyer. The financing partner assesses buyer credit, not just yours.

Think of this as a credit card for your business, but with better terms. You get approved for a credit limit, say ₹25 lakh. You only draw what you need, when you need it. You pay interest only on the amount you actually use.

Founder benefit:

Maximum flexibility. Handle unexpected costs, bridge short gaps, or seize sudden opportunities without going through approval processes each time.

These benefits compound when you approach funding strategically rather than reactively. But strategy means nothing without understanding the costs and considerations. Smart founders weigh both opportunity and risk before deploying capital. Let us examine what you need to evaluate before taking short-term funding.

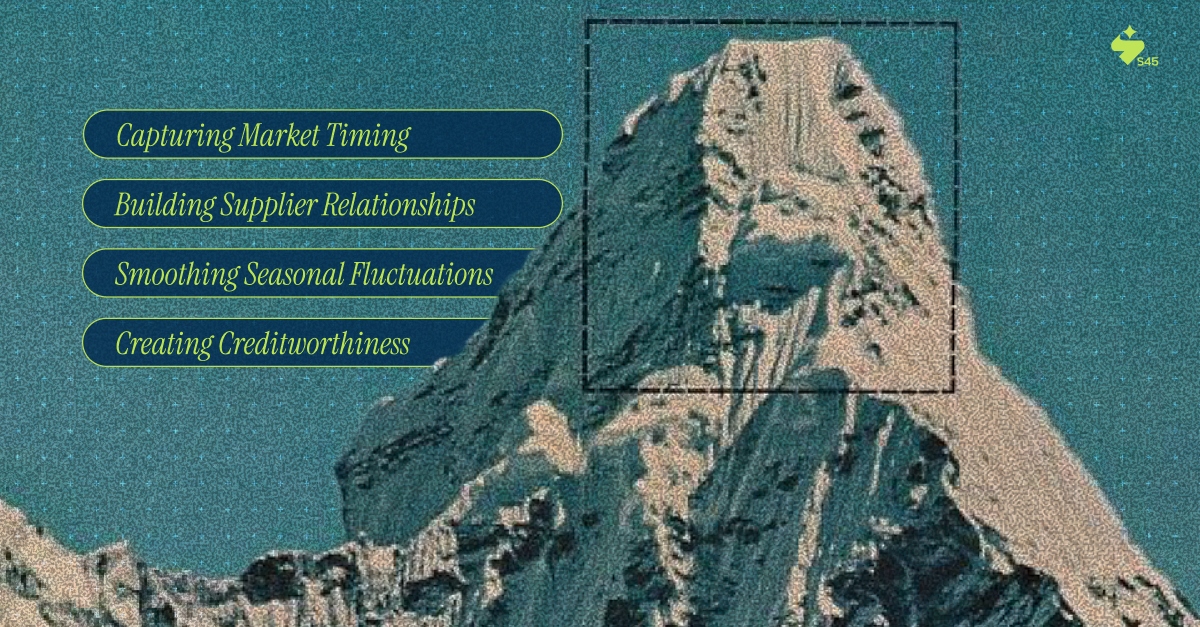

Most founders focus on obvious benefits like speed and accessibility. Those matters, but they miss the deeper strategic value. Here is what actually changes when you master short-term funding.

Markets reward speed. A competitor delays because they are waiting for cash flow. You move immediately because you have funding access. Six months later, you own that customer relationship.

In manufacturing, timing often matters more than cost. Raw material prices fluctuate. Buying when prices dip saves more than you pay in interest. Missing the window costs you margin for months.

Pay your suppliers early, consistently. Watch what happens. Better prices. Priority in supply shortages. Flexibility when you need it. These advantages compound over the years.

Short-term funding that costs you 2% can enable early payment discounts of 3%. The arbitrage is obvious, but the relationship value is priceless.

Many manufacturing sectors have seasonal demand. Textiles peak during festivals. Toys surge before holidays. Agricultural equipment moves before planting season.

Strategic short-term funding lets you build inventory ahead of demand without draining reserves. You capture full-season revenue instead of partial sales limited by cash constraints.

Here is what nobody tells you. Successfully managing short-term debt builds your credit profile faster than operating cash-positive. Each timely repayment strengthens your funding access for the next cycle.

Banks and fintech platforms track repayment behaviour. Good history opens doors to better terms, higher limits, and more sophisticated funding instruments.

Along with these, Indian MSMEs have something most global small businesses do not: a robust ecosystem of government-backed schemes designed specifically to reduce funding costs and barriers.

Indian MSMEs operate in possibly the most supportive policy environment globally for small business funding. Most founders barely scratch the surface of available advantages. Here is what actually matters.

These schemes work best when combined with proper documentation and registration. But you need to consider several factors along with that.

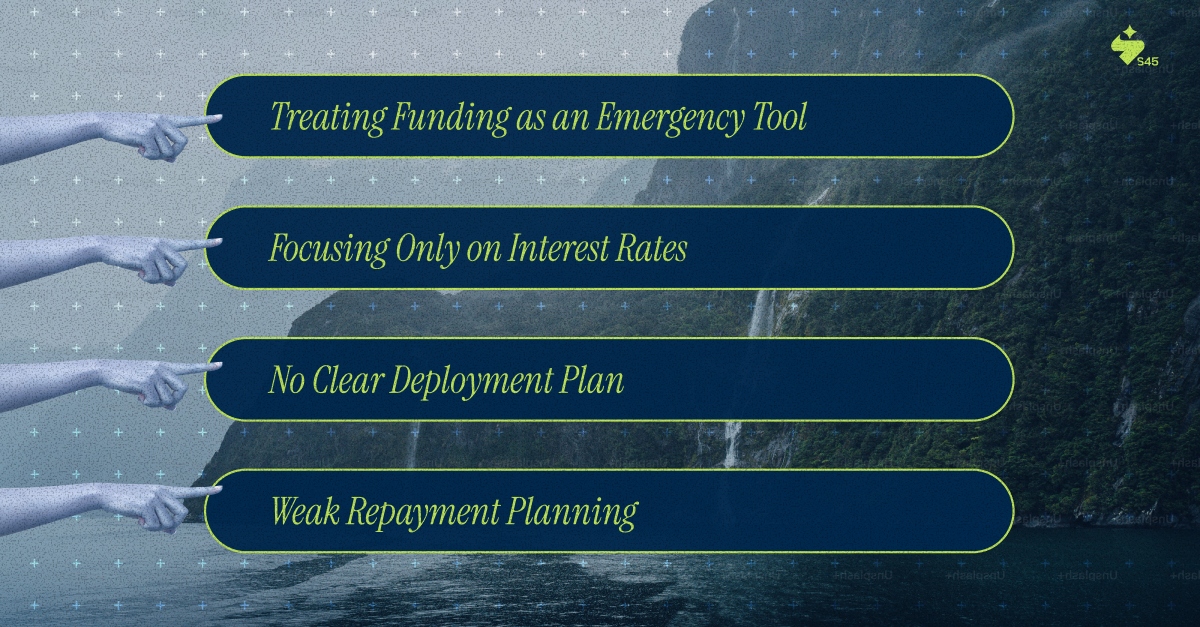

Short-term funding is powerful, but not an automatic growth lever. Used poorly, it adds stress. Used strategically, it accelerates growth. Here’s what really matters:

Strategic partners like S45 help founders model total cost scenarios before committing. Often, a slightly higher base rate with transparent terms beats a lower rate loaded with hidden charges. But even with the best intentions, founders make predictable mistakes when accessing short-term funding.

Mistakes cost time, money, and can damage credit for years. Knowing what goes wrong helps you use capital strategically from day one.

Most funding providers focus solely on capital deployment. At S45, we recognise that smart capital use matters more than capital access. Strategic benefits emerge when you match the right funding type to the right business opportunity.

The problem most MSME founders face: You can access one-time funding when desperate, but you cannot build systematic capital access that supports consistent growth. Each funding cycle feels like starting from scratch. Terms do not improve. Relationships do not deepen. Funding remains transactional rather than strategic.

How S45 solves this:

We walk beside founders to build funding architectures that improve with each cycle. Our approach combines three elements:

Founders who partner with S45 move from reactive funding scrambles to proactive capital deployment. Most importantly, they scale sustainably without the funding stress that breaks many growing businesses.

Whether you are looking to capture your next major opportunity, optimize working capital cycles, or build funding relationships that improve with time, we walk beside you through the journey. Start Your Partnership Journey with S45.

Discover more insights on similar topics