April 9, 202611 min read

What Is a PPM in Private Equity? Guide to Capital Raises Done Right

By Abhishek Bhanushali

Venture Capital

Key Takeaways

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Growth often reaches a point where internal cash flows, informal structures, and incremental financing are no longer enough. Founders and CFOs begin weighing tougher questions: how to fund the next phase without losing control, how to unlock liquidity without exiting, and how to prepare the business for institutional scrutiny.

This is where recapitalization in private equity comes into play. It is frequently presented as a clean solution, but its long-term implications are rarely examined upfront. According to KPMG, global private equity investment reached $537.1 billion in the first three quarters of 2025, signaling that more companies than ever are stepping into recapitalization structures.

What many discover later is that decisions made at this stage shape board control, disclosure standards, pricing outcomes, and even the viability of future IPO timelines. Recapitalization is not just a financing event. It is a structural reset whose effects surface years later.

This blog examines those second-order effects, outlining when recapitalization supports institutional outcomes, where founders misstep, and how to evaluate these decisions before committing.

Recapitalization in private equity refers to a transaction where a company restructures its capital base by changing the mix of equity and debt, typically alongside an investment from a private equity firm. The business continues to operate under the same legal entity, and founders usually retain an ownership stake.

In practical terms, a private equity recapitalization involves the following elements:

This structure is commonly used when a business has reached a particular scale and stability but is not ready, or does not intend, to pursue a full sale. It provides access to institutional capital while allowing founders to remain actively involved in the company.

Unlike a full exit, recapitalization does not involve a complete transfer of ownership. Founders typically roll over a portion of their equity into the new structure and continue to participate in future value creation alongside the private equity investor.

At its core, recapitalization is a capital rebalancing exercise. It determines how the business is funded, how financial risk is shared, and how long-term control is structured. These changes make recapitalization a meaningful step in a company’s progression toward institutional capital rather than a one-time transaction.

Companies pursue recapitalization when organic growth, internal capital, or informal structures no longer support the next phase of scale. When deliberately designed, recapitalization can address several constraints at once rather than introduce new ones.

Key benefits include:

Recapitalization delivers these benefits only when approached as a structural decision tied to long-term objectives. Poorly aligned structures tend to shift constraints rather than remove them.

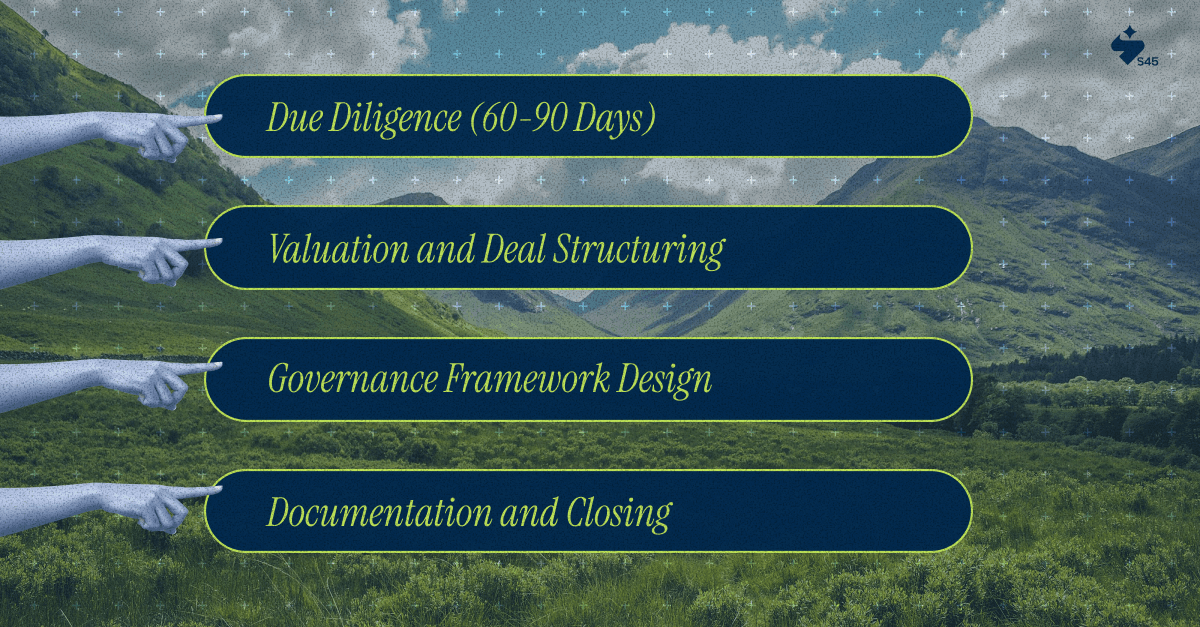

The mechanics follow a defined sequence, though execution timelines vary based on business scale and preparedness. The process typically unfolds across four distinct phases.

PE firms conduct exhaustive reviews after initial term sheet agreement:

For businesses, this often surfaces gaps in documentation and related-party transactions requiring cleanup.

Negotiations center on enterprise value, not just revenue multiples. PE firms build detailed models that incorporate growth trajectories, competitive positioning, and capital requirements.

Many Indian founders fixate on headline valuations while overlooking how debt, working capital adjustments, and transaction expenses affect the actual proceeds. The compelling valuation often differs materially from the initially quoted number.

A typical structure might look like:

Board composition and decision rights get formalized through detailed agreements. The PE firm typically secures a board majority, though founders retain operational control through management agreements.

Reserved matters require board approval:

Drag-along and tag-along rights, liquidation preferences, and anti-dilution provisions protect PE interests but constrain founder flexibility in future scenarios.

Documentation packages rival IPO preparation in scope. Share purchase agreements, shareholders' agreements, management contracts, and employment terms all require legal review and negotiation.

Indian businesses often underestimate the complexity of documentation, assuming a quicker closure than reality permits. Closing depends on the satisfaction of conditions, including regulatory approvals (if applicable), third-party consents, and financing arrangements.

Post-closing integration begins immediately, with PE firms typically driving 100-day plans focused on governance formalization, management strengthening, and operational improvements.

Also Read: Private Equity Law Key Regulations, Structures, and Risks

Not all recap structures are created equal. Each one directly affects your control, liquidity, and your ability to run the business post-deal. Understanding these trade-offs upfront helps you avoid surprises after the term sheet is signed.

In a majority recap, the PE firm acquires a 51–80% ownership stake. You secure meaningful liquidity, while the investor gains control through board seats and reserved decision rights.

What this typically means for founders:

This structure works well when you want to lock in wealth but still participate in the next phase of growth. A strong PE partner can bring operational discipline, senior talent, and credibility that help win larger customers and unlock better financing terms.

In a minority recap, the PE firm takes a 20–49% stake, while you retain majority ownership and day-to-day control.

Why founders choose this route:

This structure suits founders who value control over maximum liquidity, and whose businesses are performing well enough to attract minority capital at compelling valuations.

What to be realistic about: Minority deals are harder to source. PE firms must be comfortable backing you without control, and expectations still rise. You’ll commit to greater transparency, structured reporting, and alignment on long-term exit plans, just with less operational interference than a majority deal.

Equity recapitalization focuses on restructuring the equity stack, rather than providing liquidity or transferring control. It is often used ahead of larger PE rounds, strategic investments, or IPO preparation.

What this typically means for founders:

It works best when planned proactively. When treated as a corrective step, they often introduce dilution or disclosure complexity that resurfaces during institutional diligence.

A dividend recap introduces new debt into the business, using the proceeds to pay out a special dividend to shareholders.

This approach is more common in mature, cash-generative businesses with predictable earnings. For PE-backed companies, it’s often a way to generate early returns without selling equity.

Where founders need to be cautious:

Dividend recaps can make sense, but only when cash flows are resilient, and downside scenarios are well understood.

S45 works with founders to objectively evaluate these paths, helping you choose a structure that aligns with long-term goals while building the institutional readiness to keep multiple capital options open.

Also Read: Who Are Angel Investors? Relevance in 2025

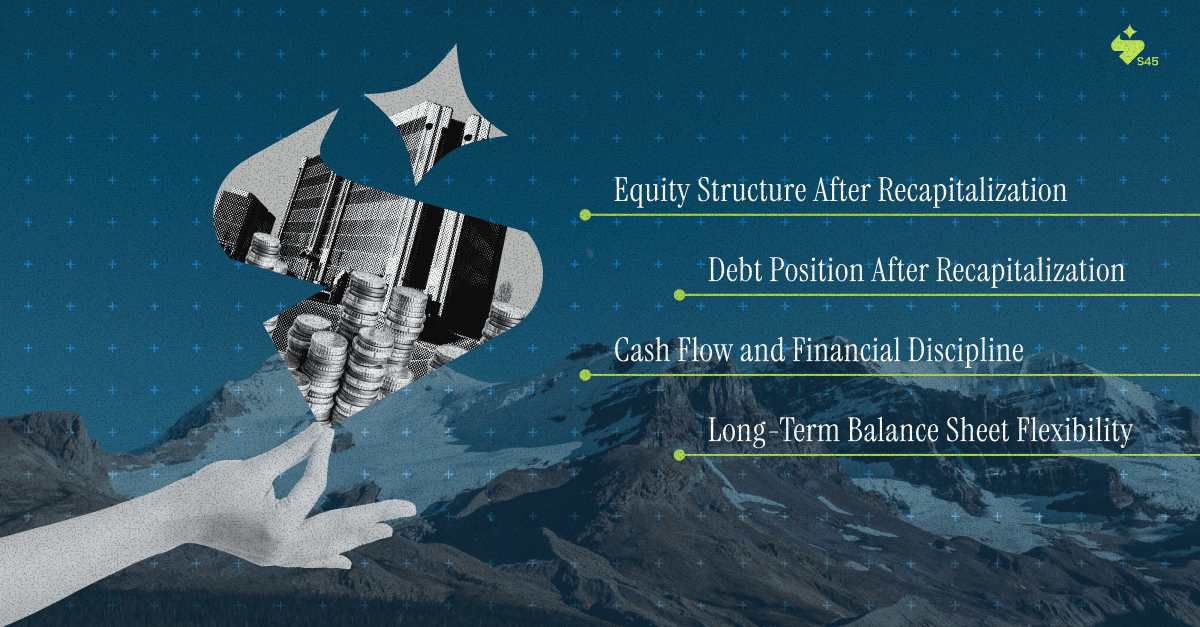

After a recapitalization, the most immediate changes appear in the company’s equity structure and debt profile. These shifts influence ownership economics, cash flow priorities, and long-term flexibility.

Recapitalization typically introduces a more layered equity structure. Instead of a single class of equity, the cap table may now include multiple instruments with distinct economic and governance rights.

Common changes include:

In many recapitalizations, debt becomes a more active component of the balance sheet. Even modest leverage changes how financial decisions are evaluated.

Typical outcomes include:

Post-recapitalization, cash flow management becomes more structured and predictable. Budgeting, forecasting, and working capital oversight tend to tighten as external stakeholders rely on consistent performance.

This shift often results in:

The combined effect of new equity layers and debt obligations shapes future capital decisions. Additional fundraising, secondary sales, or listing plans must account for existing rights and repayment structures.

Recapitalization functions as a structural reset rather than a temporary adjustment. The way equity and debt are configured at this stage influences every subsequent capital event.

Also Read: Decoding Private Equity Metrics for Founders

Most recapitalization missteps follow predictable patterns. If you are aware of them early, they are largely avoidable. The issues usually do not come from the deal itself, but from how founders prepare for what comes after.

It is easy to view recapitalization primarily as a way to take money off the table. In reality, you are entering a three-to-five-year operating partnership with defined performance expectations.

Once the transaction closes:

Founders who disengage after securing liquidity often struggle. Private equity partners expect continued leadership, not a gradual step-back.

After recapitalization, informal decision-making gives way to documented processes.

You should expect:

If you resist these changes, friction builds quickly. Founders who adopt governance discipline early tend to scale more smoothly, both during the PE partnership and beyond it.

Complexity may seem manageable during negotiations, but it creates downstream challenges.

Common issues include:

Simple structures tend to travel better across capital events. Common equity, clear debt terms, and a clean cap table make future transactions faster and less contentious.

Related-party arrangements, informal promoter loans, and undocumented practices rarely survive institutional scrutiny. Leaving these issues unresolved slows diligence and weakens the negotiating position.

A better approach is to:

This preparation shortens deal timelines and keeps multiple capital options open.

S45's IPO Readiness Scan identifies these gaps before they become deal impediments, assessing operational, compliance, and financial dimensions through institutional capital requirements.

Also Read: Understanding How GPs and LPs Drive Private Equity Growth

Private equity recapitalization can either support a future IPO or quietly complicate it. The outcome depends less on the investor involved and more on whether the structure withstands public market scrutiny.

Recapitalization supports your IPO when it brings clarity and stability into the business, not just capital.

When these conditions are in place, recapitalization can shorten the transition from private ownership to public markets.

Recapitalization works against you when short-term decisions create long-term complexity.

In these situations, you may still reach the IPO stage, but the process often involves more friction around valuation, timing, and investor confidence.

Also Read: Is Your Business Facing a Funding Gap? Here’s What Every SME Should Know

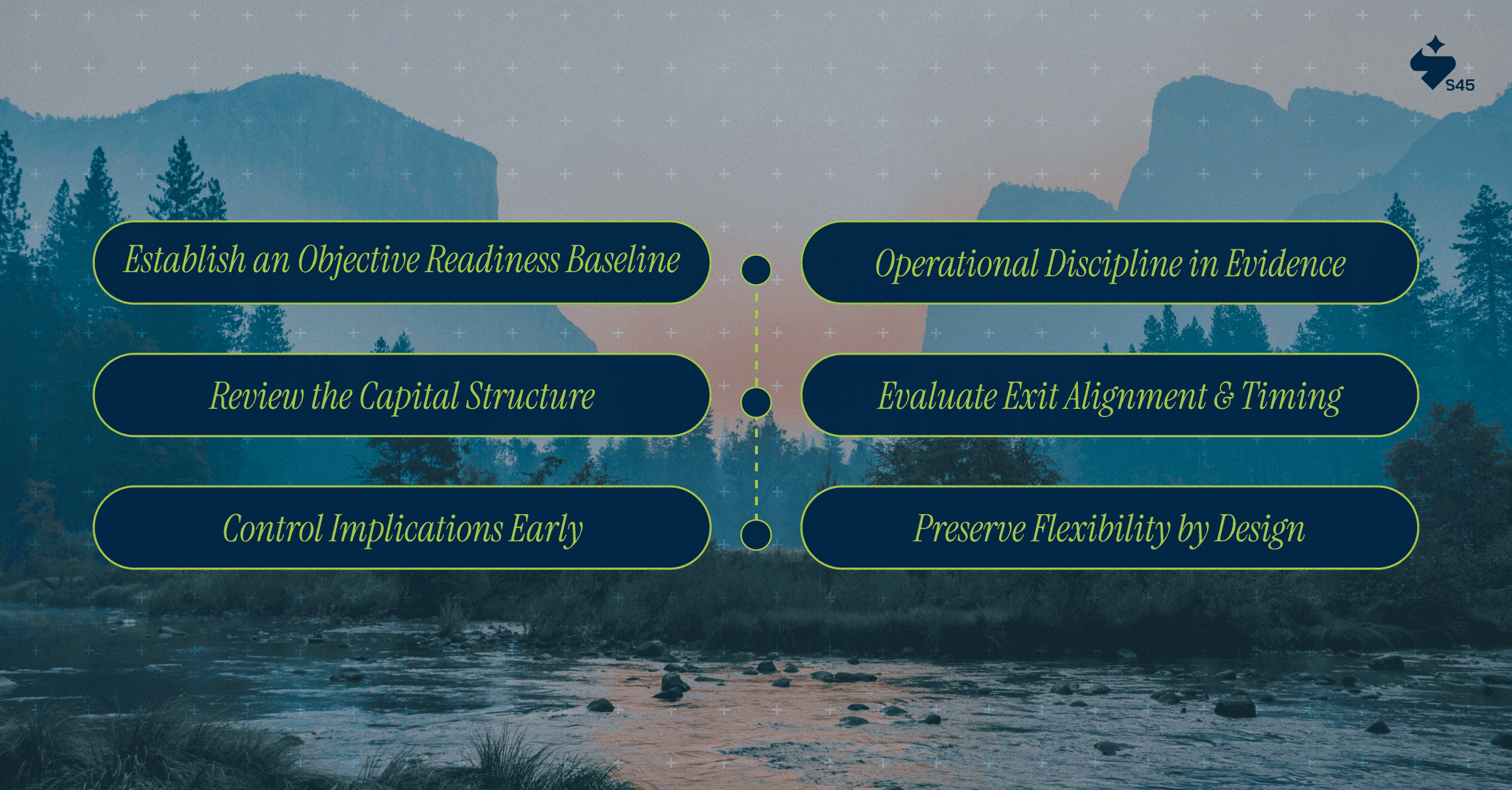

Before signing a term sheet, founders should evaluate recapitalization the same way public markets will later determine the company's valuation. These steps help surface risks early, when they can still be addressed.

Do not assume readiness is based solely on growth or profitability. Begin by assessing the business across three areas:

If gaps exist here, recapitalization will magnify them rather than resolve them.

Model the post-recapitalization structure as if the company were filing for an IPO:

If the structure raises questions in this exercise, it will raise questions later.

Recapitalization formalizes decision-making. Founders should evaluate:

Clarity here reduces friction and preserves operational focus after closing.

Public markets value consistency over intent. Ensure that:

Before committing, confirm alignment on:

Misalignment here often becomes visible only when options narrow.

Future options depend on structure, not intent. Prioritize:

The goal is to keep paths open without renegotiating core terms.

Recapitalization should increase clarity, not introduce new uncertainty. Following a structured evaluation before committing allows founders to move forward with confidence, knowing the decision supports long-term institutional outcomes.

Private equity recapitalization represents one path in your capital journey, not necessarily the optimal path for every business.

S45 works with founders at this inflection point. We help determine whether PE recapitalization serves your objectives or whether alternative paths like direct IPO preparation, strategic minority investors, or debt-based growth funding better match your situation.

Every recommendation links to specific regulatory requirements, market precedents, or data from comparable transactions. We show what institutional investors scrutinize, how similar businesses structure capital, and where your business stands relative to listing or PE readiness benchmarks.

If PE recapitalization aligns with objectives, we help prepare:

Our goal is to prepare your enterprise for whatever capital path serves your long-term vision, not to push transactions that serve advisor economics.

Recapitalization in private equity sits at the intersection of private ownership and institutional capital. How you approach this decision determines how smoothly your company transitions into its next phase, whether that is additional private capital, a strategic transaction, or a public listing. Recapitalization works best when it is treated as part of that broader trajectory, rather than as a standalone event.

This is the lens S45 brings to founders. S45 evaluates recapitalization decisions in the context of public-market expectations, ensuring capital structure, governance, and disclosures are built to endure, not just to close a deal.

If recapitalization in private equity is on your roadmap, the most constructive next step is to contact us and understand how your current structure measures up against institutional benchmarks.

Discover more insights on similar topics