April 1, 202612 min read

Traditional vs Alternative Investments: What You Need to Know Before Going Public

By Aman Singh

Investopedia

Key Takeaways:

At a certain scale, capital market execution becomes less forgiving. Every trade, disclosure, allocation, and settlement decision starts to affect timelines, pricing, and regulatory outcomes in very real ways.

This is where the trade life cycle matters.

In investment banking, the trade life cycle is the operational backbone of execution. It defines how intent becomes data, how that data moves across teams, and how consistently outcomes hold up under regulatory and market scrutiny.

When handoffs are manual, ownership is fragmented, or information lives in silos, risks tend to surface late and compound quietly. For companies preparing for the public markets, these gaps often translate into delays, rework, and pricing uncertainty.

This blog breaks down the trade life cycle through an execution lens and explains why institutional discipline across every stage matters.

The trade life cycle is often described as a series of steps. In reality, it is the system that determines control, accountability, and timing across every capital market transaction.

At its core, the trade life cycle exists to answer three critical questions:

When this system works, execution feels predictable. When it does not, delays, rework, and regulatory exposure begin to compound.

This matters far more at scale and especially in public markets. As transaction volumes grow and disclosures become stricter, even small gaps between teams, systems, or versions of data can trigger pricing confusion, SEBI observations, or missed market windows. What worked in a private setup begins to break once institutional scrutiny enters the picture.

There is also a fundamental difference between executing a trade and owning execution end-to-end:

Most failures in investment banking are not caused by a single mistake. They come from broken links between stages of the trade life cycle.

Seen this way, the trade life cycle is less about process and more about precision. It is the foundation that determines whether capital market execution stays disciplined or unravels under institutional scrutiny.

Capital market outcomes are decided by execution systems, not intent. S45 helps growth-stage companies assess readiness, surface execution gaps, and move from mandate to DRHP with institutional discipline.

The trade life cycle is best understood as a single flow, not a checklist. Each stage feeds the next, and small breakdowns early on tend to surface later as bigger execution or compliance issues.

This is where intent becomes data. A trade is agreed, terms are set, and details are entered into systems.

What matters here:

Errors at this stage rarely disappear. They usually resurface downstream as rework.

This is the first real checkpoint. The trade details are validated between counterparties to confirm everyone sees the same version of the truth.

What happens here:

If confirmation is slow or unclear, execution timelines start slipping quietly.

This is where money, securities, and counterparty obligations actually move.

Key focus areas:

Any disruption here directly impacts credibility and, in public markets, regulatory confidence.

This is where compliance and audit risk live. Trades are recorded, reported, reconciled, and disclosed.

This stage covers:

Most regulatory observations originate here, often because earlier stages were not clean.

In modern capital markets, these stages are tightly linked. Data captured early drives disclosures later. Confirmation affects settlement. Settlement quality affects reporting. Treating them as separate functions creates blind spots. Institutional execution depends on managing the entire life cycle as one continuous workflow, not isolated tasks.

Also read: Investment Banking in India: Roles, Growth Opportunities & How to Get Started

Most failures in capital market execution do not come from poor intent or lack of expertise. They come from how work moves between stages of the trade life cycle. The breakdowns are operational, but their impact compounds as execution progresses.

The same data is often entered separately by bankers, legal teams, auditors, and registrars. Small inconsistencies creep in early and travel downstream. By the time numbers are reconciled, pricing discussions and disclosures are already exposed to uncertainty.

Email threads, spreadsheets, and static documents create parallel versions of the same information. Teams may believe they are aligned, but subtle mismatches remain. These gaps slow decisions and raise questions during regulatory review.

When confirmations rely on back-and-forth coordination rather than structured workflows, issues surface late. Errors that should have been resolved early reappear during filing or bookbuilding, when timelines are tight and corrections are costly.

Spreadsheets remain the default tool for reconciling trades, allocations, and disclosures. At scale, they are fragile. Errors discovered late force rework across multiple documents and stakeholders, often pushing timelines out.

When compliance checks happen after drafting is underway, gaps in disclosures, controls, or governance emerge too late. Fixing them at that stage can stall filings and disrupt execution momentum.

These breakdowns are well known inside capital markets. The harder question is why they persist, even with experienced teams and established institutions.

These breakdowns persist not because teams are careless, but because the underlying execution model has not changed.

Most investment banks still rely on:

Execution responsibility is fragmented. Each party owns a piece, but no one owns the full life cycle. As long as this structure remains, errors will surface late, timelines will stretch, and outcomes will depend on firefighting rather than precision.

This is a structural limitation, not an individual failure. Experience alone cannot compensate for systems that were never designed for today’s regulatory intensity, transaction volumes, or speed expectations.

In private markets, these gaps are inconvenient. In public markets, they become execution risk with visible consequences.

When these execution gaps carry into an IPO, the consequences become visible and expensive.

DRHP timelines stretch as inconsistencies force repeated reviews and redrafting. Pricing discussions lose clarity when disclosures, forecasts, and comparables do not align cleanly. Allocation conversations weaken as institutional investors sense uncertainty in numbers or controls.

Missed market windows are rarely caused by a single delay. They happen when small execution issues accumulate until timing slips beyond control. Even when a listing proceeds, weak pre-listing discipline can show up as volatility in the aftermarket, affecting credibility and confidence.

At this stage, the issue is no longer operational efficiency. It is outcome risk. In public markets, execution quality directly influences valuation, demand, and long-term perception.

This is why the trade life cycle cannot be treated as a checklist. It must be owned as a continuous execution system, built to hold up under institutional scrutiny.

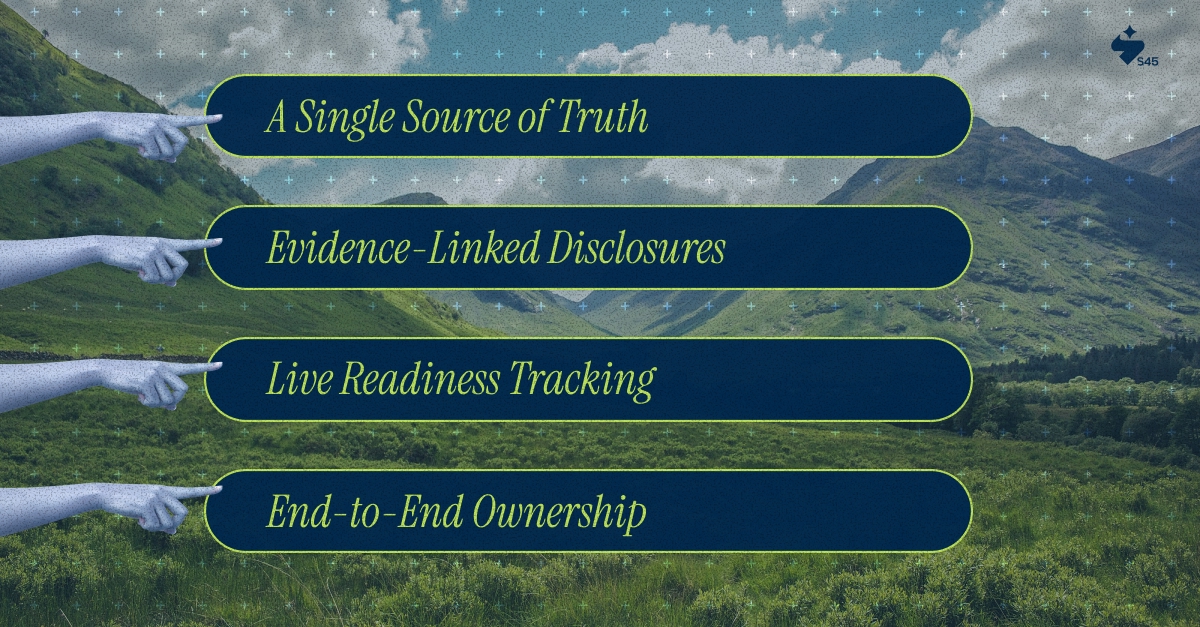

Institutional execution does not treat the trade life cycle as a series of handoffs. It treats it as one continuous system with shared data, clear ownership, and built-in controls.

Institutional systems start with a unified data layer. Financials, disclosures, and transaction data live in one place, not across emails and spreadsheets. When data changes, every dependent output updates automatically, removing reconciliation work and silent inconsistencies.

Every number, claim, or projection is tied back to a verifiable source, whether an audited statement, contract, or operational record. Compliance shifts from reactive checking to proactive design, making regulatory review faster and more predictable.

Readiness is not assumed. It is measured continuously. Gaps in governance, controls, or disclosures are surfaced early, with owners and timelines clearly assigned. This turns execution from a guessing game into a managed process.

Responsibility does not reset at each stage. The same system carries accountability from initiation through settlement, reporting, and beyond. This continuity allows speed without shortcuts and reduces execution risk at scale.

The result is a trade life cycle built for scrutiny. Precision replaces rework, and timing becomes a strength rather than a liability.

At a public-market scale, outcomes are shaped less by intent and more by execution discipline. The trade life cycle is where that discipline is tested. When ownership is fragmented or data moves slowly, risk accumulates quietly and surfaces late, often when timelines, pricing, and regulatory confidence matter most.

This is why modern capital market execution demands systems, not workarounds. Institutional clarity comes from owning the lifecycle end to end, linking data to evidence, and moving with speed that does not compromise control.

S45 was built to close this execution gap.

As India’s first AI-native investment bank, S45 combines sector-experienced bankers with a unified execution platform that runs from IPO readiness through listing and post-market stability.

If you are preparing for the public markets and want a clearer, faster, and more disciplined path to listing, start with an IPO Readiness Scan or speak with a banker to assess where execution risk truly sits.

Discover more insights on similar topics