April 10, 202611 min read

Angel vs. Seed Funding: What Every Indian Founder Must Know Before Raising Capital

By Abhishek Bhanushali

Startup Funding

Disclaimer: This content is for educational purposes only and should not be considered as financial advice. Every business situation is unique, and we recommend consulting with qualified financial advisors before making important business decisions.

Every equity term sheet shrinks your ownership. For growth-stage Indian founders, the "Series B/C crunch" often forces a choice between a painful down round or stalled growth, eroding the control you worked to build.

Non-dilutive funding provides a strategic alternative, allowing you to capitalize operations without sacrificing board seats or equity. It serves as a bridge to major milestones, like an IPO, without the permanent cost of dilution.

In this guide, we will break down the mechanics of non-dilutive capital structures available in India. We will move beyond basic definitions to examine the eligibility criteria, the hidden costs of debt instruments, and how to build a capital stack that prepares your company for the ultimate liquidity event.

Non-dilutive funding refers to any capital acquisition method that does not require the company’s owners to give up equity or ownership stakes. Unlike venture capital or angel investment, where you trade shares for cash, non-dilutive capital functions on a repayment model or grant basis.

It provides immediate liquidity for operations, expansion, or R&D while ensuring the founder's control and cap table remain intact.

Understanding the fundamental difference between selling a part of your company and renting capital is the first step in optimizing your capital structure.

Strategic capital allocation is the difference between a diluted cap table and a high-valuation exit. Talk to an S45 banker today to evaluate your non-dilutive options and build a data-driven roadmap.

Founders often conflate "non-dilutive" with "cheap." This is a mistake. While you save equity, you take on repayment pressure. Here is how the asset classes compare structurally:

Feature | Equity (VC/PE) | Traditional Bank Debt | Non-Dilutive (RBF/Venture Debt) |

Cost of Capital | Most Expensive (Future Upside) | Cheapest | Moderate |

Ownership Impact | High Dilution | Zero Dilution | Zero to Low (Warrants) |

Collateral | None | Hard Assets (Land/Machinery) | IP/Cash Flow/Revenue |

Repayment | Exit/IPO | Fixed Monthly EMIs | Revenue Share or Bullet |

Speed to Close | 3–6 Months | 2–4 Months | 2–6 Weeks |

Selecting the right instrument requires knowing exactly what options exist in the Indian market.

Also Read: Top 8 Government Grants for Startups in India 2025

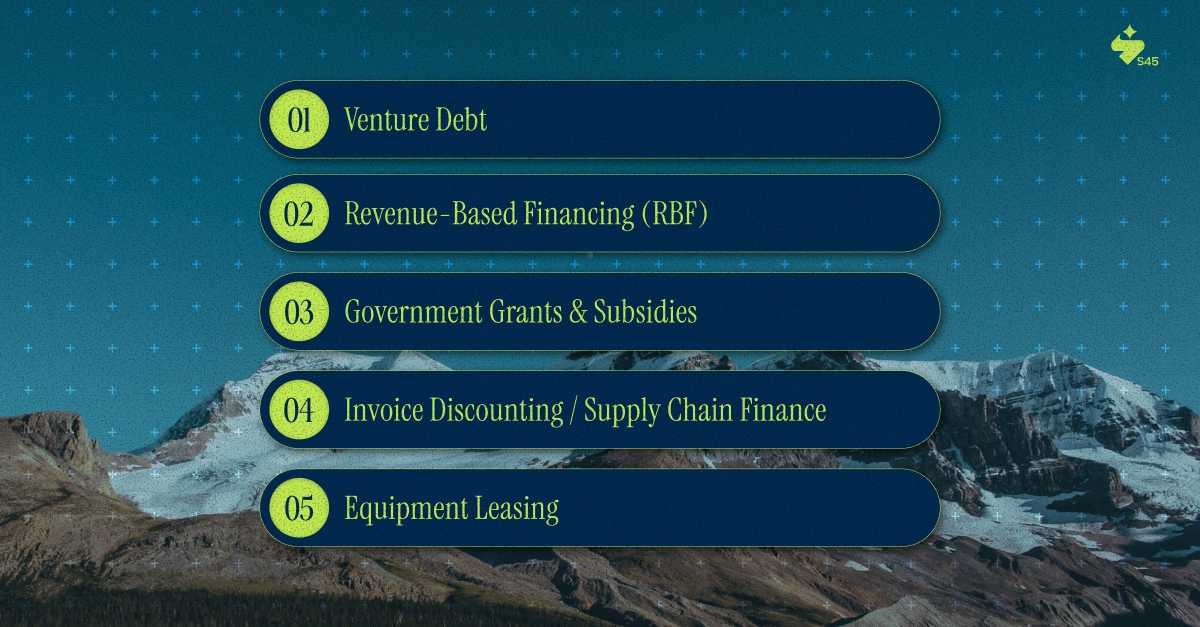

Non-dilutive funding is not a monolith. It encompasses diverse instruments, each with unique mechanics, ideal use cases, and risk profiles. Selecting the right one depends on your business model, the purpose of the capital, and your financial maturity.

This is term loan debt provided specifically to venture capital-backed startups. It typically includes warrants (options to buy equity at a fixed price), which makes it slightly "dilutive" in a technical sense, but it remains primarily a debt instrument used to extend the cash runway between equity rounds.

Lenders provide a lump sum in exchange for a fixed percentage of your company's future monthly revenue until a pre-determined total (the cap) is repaid. This model directly aligns repayment with your business performance.

Funds provided by government bodies (e.g., SIDBI, various state and central schemes) to support innovation, R&D, or businesses in priority sectors. These are often true "free money" with no repayment or equity required, though they come with strict compliance and usage requirements.

You sell unpaid invoices to a financier at a discount to get immediate cash. This bridges the working capital gap between delivery and payment.

Instead of buying the machinery up front, a lender buys it and leases it to you. This keeps cash on the balance sheet for operations rather than capex.

Knowing the types is useful, but knowing when to deploy them determines success.

Non-dilutive funding is not a default option; it is a strategic choice with a clear set of triggers. Deploying it at the wrong stage or for the wrong reason can burden your cash flow without delivering sufficient growth to justify the cost.

Once you decide to proceed, you must quantify the requirement precisely.

Also Read: Pre-IPO Investing in India: A Complete Guide for Smart Investors

Precision is critical. Raising too little leaves the goal unfunded; raising too much incurs unnecessary cost and repayment pressure. Your calculation must be directly tied to a specific, bounded use of funds.

Follow this three-step framework:

1. Calculate the Working Capital Gap: Look at your Cash Conversion Cycle.

2. Determine the "Bridge" Duration: If your goal is a Series B or an IPO in 15 months, and your current cash lasts 9 months, you need exactly 6 months of burn + a 20% buffer.

3. Assess Serviceability: Ensure your EBITDA or gross margins can cover the interest/revenue share without stalling growth. A debt-to-revenue ratio above 30-40% is usually the danger zone for high-growth firms.

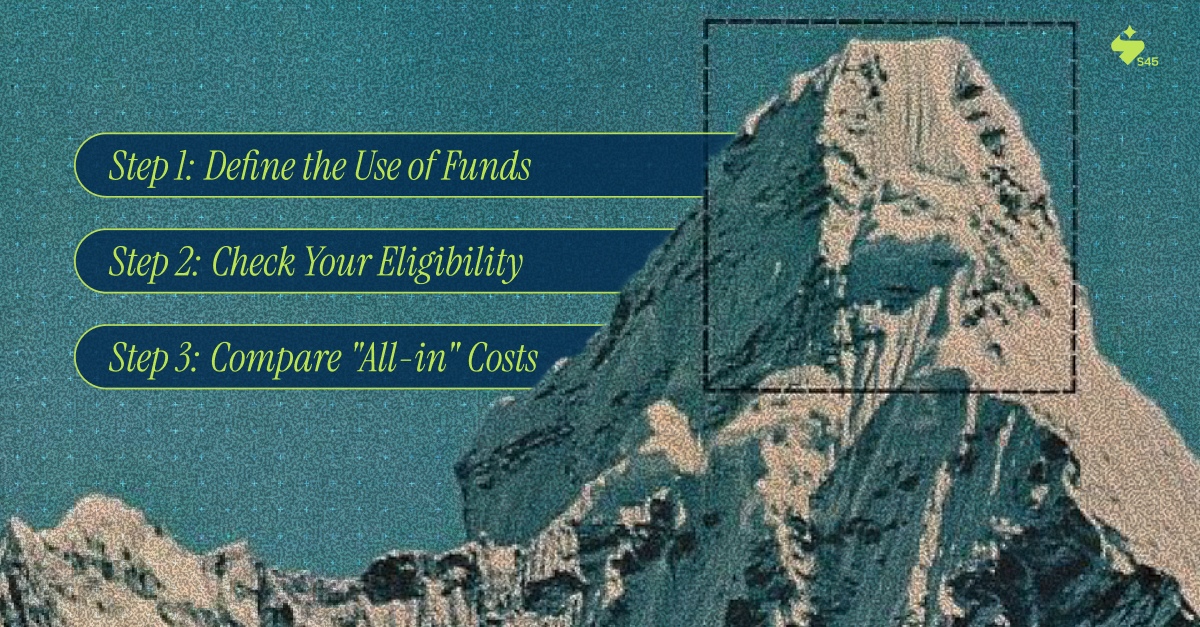

With the number in hand, follow a disciplined selection process.

With multiple instruments available, a structured evaluation process prevents you from chasing the wrong option. This workflow moves from internal assessment to external sourcing.

Follow this sequence to narrow your focus efficiently:

Let’s dive deeper into how the specific instruments function.

Also Read: A Complete Guide on Private Investment in Public Equity (PIPE)

Understanding the basic mechanics, requirements, and ideal use cases for each major instrument allows you to engage with providers from a position of knowledge. Here’s what you need to know:

Investors advance a lump sum. You repay a fixed percentage (e.g., 5-10%) of monthly revenue until a multiple (e.g., 1.2x) is paid back.

A term loan provided to VC-backed startups. It often includes a "principal moratorium" (you only pay interest for the first 6-12 months).

Capital provided by the government for innovation, usually disbursed in tranches based on milestones.

Understanding the mechanics is futile if you miscalculate the cost.

To make an informed decision, you must translate financing terms into standardized metrics that allow for comparison with both other debt and the cost of equity dilution.

1. Effective Annual Rate (EAR): This accounts for compounding periods. A 1% monthly rate is not 12% per year; it is higher due to compounding.

2. Internal Rate of Return (IRR): For RBF, calculate the IRR based on your projected revenue growth. If you pay back the loan in 6 months because you grew fast, your effective interest rate might be 30%+.

3. Debt Service Coverage Ratio (DSCR):

Calculations protect you from financial risk, but structural risks remain.

Don't get caught by 'flat rates' or warrant traps. Request a call with a S45 banker to learn about cost analysis that uncovers the true EAR and IRR of your funding offers.

Also Read: How to Apply for Venture Capital: A Comprehensive Guide

Mistakes in structuring or managing non-dilutive capital can negate its benefits and create severe financial strain. Awareness of these traps is your first line of defense.

To avoid these traps, integrate non-dilutive capital into a broader strategy.

Also Read: A Guide to Overcoming Common MSME Funding Issues For Growth

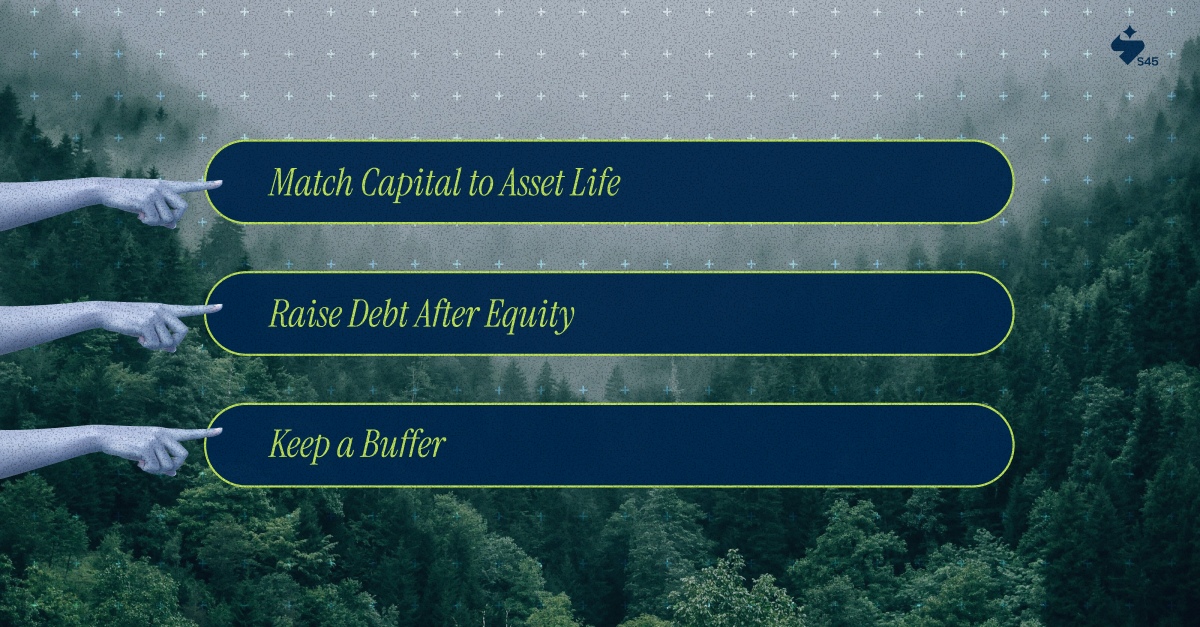

The goal is not to choose between equity and non-dilutive capital, but to blend them into a strategic "capital stack" that optimizes for cost, control, and flexibility across your company's lifecycle.

Impact: Use long-term equity for long-term assets (brand building, R&D). Use short-term debt for short-term assets (inventory, receivables). This matches your liability duration to your asset duration.

Impact: Raising debt immediately after an equity round gives you the best terms (lowest interest rates) because your balance sheet looks strongest.

Impact: Never borrow the absolute maximum offered. Borrowing 70% of the limit leaves room for error if a quarter misses projections.

Strategy is useless without execution. Here is how to prepare.

Lenders and grantors invest in clarity and low risk. Your preparation signals operational maturity and directly influences the terms you receive.

Securing non-dilutive funding is often the final bridge a company crosses before targeting the public markets. However, efficiently deploying that capital to meet the rigorous governance and profitability standards of an IPO requires more than just money; it requires a roadmap.

S45 prepares growth-stage Indian companies for this transition, ensuring that when you do graduate to the Main Board or SME exchange, you are fully compliant and accurately valued.

Why choose us:

We ensure that the capital you raised today translates into a successful listing tomorrow.

Non-dilutive funding is a strategic tool for preserving ownership while financing predictable growth. By choosing the right instrument and integrating it into your capital strategy, you build a stronger, more efficient balance sheet.

S45 bridges the gap between private ambition and public execution. Our AI-native platform provides instant IPO readiness scans, data-driven demand mapping, and 0% upfront fees. We manage the end-to-end process, from DRHP filing to post-listing IR, letting you focus on growth.

Ready to fuel your growth without surrendering equity? Begin with clarity. Talk to a banker today for a data-driven assessment of your non-dilutive options and their impact on your long-term capital strategy.

Discover more insights on similar topics